December 2022 / MARKET OUTLOOK

The Need for Agility

A time to be selectively contrarian

KEY INSIGHTS

- Central bank efforts to tame inflation have reached a critical point. In 2023, investors will be looking for the peak in interest rates.

- U.S. earnings growth estimates may be too optimistic. But we see relative valuation advantages in some equity sectors and in non-U.S. markets.

- The worst bond bear market on record pushed yields to some of the most attractive levels since the global financial crisis. Investors appear to have noticed.

- The threat of global economic decoupling has been exaggerated, but big structural changes are in progress. We see opportunities amid the disruptions.

Heading into 2023, capital markets appear to have priced in a significant global economic slowdown. The key question is whether this deceleration will end in a “soft landing”—with slower but still positive growth—or in a full‑fledged recession that drags down earnings.

Much depends on the U.S. Federal Reserve (Fed) and the world’s other major central banks as they continue efforts to bring inflation under control by hiking interest rates and draining liquidity from the markets.

“History is not on our side,” says Sébastien Page, head of Global Multi‑Asset and chief investment officer (CIO). “Fed hiking cycles don’t generally end well, especially when inflation is running high.”

But investors shouldn’t assume a deep downturn is inevitable, Page adds.

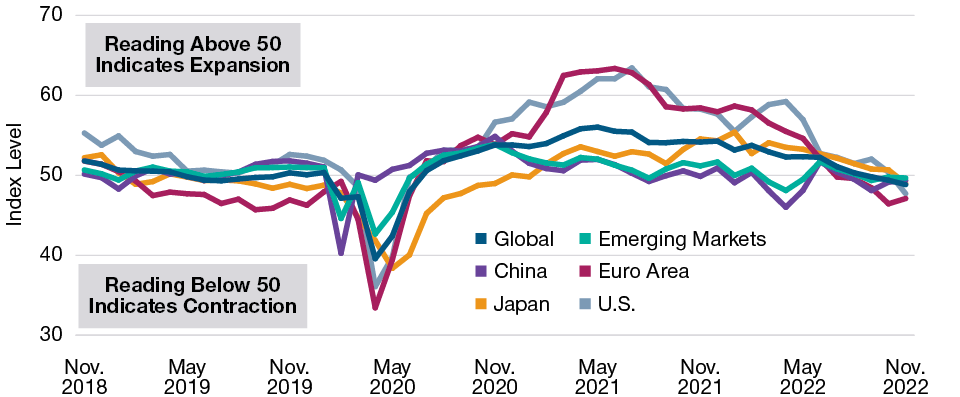

Although some leading indicators have weakened (Figure 1), U.S. employment was still growing in late 2022. Corporate and household balance sheets appeared strong. And the economic wounds inflicted by the COVID pandemic continued to heal, notes Justin Thomson, head of International Equity and CIO.

Geopolitical risks will remain potential triggers for downside volatility in 2023. Structural factors, such as bank capital requirements that constrain market liquidity, could magnify price movements, both up and down.

With most central banks seeking tighter financial conditions, investors can’t count on them to intervene if markets fall, warns Andrew McCormick, head of Global Fixed Income and CIO.

“We’ve come out of a period where central banks had strong motivation to suppress volatility,” McCormick says. “Now, policy is aimed at tightening financial conditions. So there is no buyer of last resort when markets come unhinged.”

But excessive pessimism and volatility can create value for agile investors, the CIOs note. An attractive point to raise tactical exposure to equities and other risk assets may appear in 2023, Page predicts. However, as of late 2022, it had not yet arrived, in his view.

Until it does, Page favors a “selectively contrarian” approach of tilting toward specific sectors within asset classes— such as small‑cap stocks relative to large‑caps and high yield relative to investment‑grade (IG) bonds.

In difficult markets, security selection will be critical, Page says. “Active management skill is just incredibly important in this environment.”

Leading Indicators of Economic Growth Are Fading

(Fig. 1) Purchasing Managers’ Index Levels for Manufacturing

As of November 2022.

Sources: Institute for Supply Management/Haver Analytics, J.P. Morgan/IHS Markit, Bloomberg Financial L.P. (see Additional Disclosures). Data analysis by T. Rowe Price.

Explore our four themes:

An Economic Balancing Act

Aggressive rate hikes are slowing economic growth. But a deep downturn across the globe is not inevitable.

Leaning Against the Wind

In the face of challenging headwinds, a careful contrarian approach could offer potential for investors.

The Return of Yield

Yields are appealing in select markets and buying opportunities exist, but investors will need to be mindful about volatility.

Deglobalisation in a Connected World

We are seeing a shift in the global economy that could shape the investment landscape for years to come.

Read our full 2023 Global Market Outlook (PDF)

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.