June 2021 / INVESTMENT INSIGHTS

What Makes an “Impact” Investment Manager?

Understanding the required foundation to build, manage, and measure an impact portfolio

Key Insights

- Impact investing aligns the interests of stakeholders, including shareholders, fiduciaries, and listed corporates, to pursue positive social or environmental outcomes.

- It involves directing capital toward desired impact outcomes and integrates impact‑oriented company engagement, proxy voting, and a commitment to actively influence via the ownership and engagement feedback loop.

- Impact measurement is a separate and more complex discipline than performance measurement, but we believe that businesses addressing social and environmental needs, with a defined and sustainable business model, put themselves in an advantaged position to meet required impact and return thresholds.

Impact investing brings a nonfinancial dimension to the investment process—a values‑based approach that seeks positive environmental and/or social impact as part of distinct performance targets. While originally the domain of private investors, we believe the potential to capture and create impact in public equity markets has broadened tremendously over the past decade.

This is largely a function of a growing urgency and demand for solutions to the pressing needs of society. The willingness of investors to supply capital to those businesses recognizing these needs has in effect created the potential to invest for impact in public markets, with greater scale and liquidity and on a truly global basis. Within public equity markets, understanding impact fundamentals and how companies are contributing to positive outcomes is crucial for shaping a credible portfolio. Understanding traditional fundamentals, including valuation and the persistence and durability of a business, is also key to ensuring that a portfolio performs financially, while contributing to change an investor wants to evidence.

Here, Hari Balkrishna discusses the essential elements that underpin the materiality of impact within an investment strategy.

Q. Can public equity investing really make an impact on key environmental and social concerns, especially when compared with private investing?

I think public markets are essential to achieving the collective goals of society. In its purest form, supplying new capital to an entity that could not otherwise access capital to generate its intended positive impact is the origin of impact investing. While impact investing has deep roots in private capital and philanthropy, solving for today’s elevated and global environmental and social pressure points demands a complementary approach. In public equity markets, this means understanding, addressing, and aligning the interests of stakeholders—including shareholders, fiduciaries, and listed corporates—to capture, accelerate, and pursue positive outcomes.

While we understand and have engaged in the private versus public capital argument, we disagree that impact investing is purely a private-equity market domain. This is in line with the Global Impact Investing Network’s definition of impact investing, albeit within high standards of intentionality, materiality, measurement, and additionality, which are clearly stated as requirements to be an impact investor.

Supplying new equity or debt capital to businesses to accelerate their impact profile is one fundamental opportunity that should present itself within public equity markets, while additionality has clear roots in engagement with corporates to further the positive impact of a business.

Given the magnitude of the world’s environmental and social challenges, we believe that private markets alone will not suffice to build the required solutions to the very real and very complex friction points that exist for our planet and our global community. To match the magnitude of the issue with a magnitude of response, governments, capital owners, and asset managers must work together to incentivize and align listed businesses with better practices. Impact investing is one way to do this by adding a perspective into the investment process directed at the broader consequences of a business’s operations.

While we are early in this journey, we truly believe that being on the right side of change with respect to the focus on the true impact of a business will be crucial within private-equity and public equity portfolios alike.

Q. How do you make a difference for clients as an impact investment manager?

We aspire to be a partner to our clients, using our full breadth of ideas to harvest both impact and alpha over the long term, while managing for risk, given challenging times, will invariably come to our natural habitat of investing.

Impact investing has grown tremendously in recent years, and we do not believe there needs to be a sacrifice of return potential in order to implement a values‑based approach. This is directly linked to how positive environmental and social outcomes are becoming more measurable, which in turn is being reflected in the economic potential of a business.

Part of my role as an impact investor is helping individuals and institutions make sense of what’s happening in the world around us and how that could manifest into risks and opportunities within investment portfolios. For example, as the environmental costs of climate change accelerate, planning for the future and thinking about climate mitigation can genuinely help a company’s bottom line.

As businesses become more conscious and active in aligning capital with the economic returns that can legitimately flow from addressing environmental or social tensions, I expect opportunities to grow. That is important because breadth is a key foundation of consistency and meeting the return objectives of impact investing. In short, we are in an era of growth with respect to the opportunity set of impact stocks.

However, in the same way that our environmental sustainability journey requires resilience, commitment, iteration, and imagination, so too will the journey of investing for impact, with a deep analysis and a long‑term belief system acting as a core driver of decision-making.

Q. How does an investment manager contribute to positive impact?

Impact is achieved within an investment portfolio in more ways than simply owning and capturing the economics and activities of certain types of companies. It involves directing fresh capital toward desired impact outcomes, alongside impact‑oriented company engagement, proxy voting, and the associated influence feedback loop.

As a starting point, it is important to screen companies from an impact lens for both materiality and measurability of the desired outcome. This requires an understanding of a business in the context of a defined impact framework expressing clear principles and intentions and identifying businesses that are best in class. For us, this is driven by a combination of evaluating a company’s current and future operations and the alignment of earnings or revenues with the United Nations Sustainable Development Goals (UN SDGs), with a holistic perspective on a business, using the five dimensions of impact framework.1 We use the word “future” very deliberately, given the rapid evolution of many businesses and the need to look forward from the starting point of today’s well‑known and understood fundamentals.

Our investment process embeds clear principles of materiality and measurability and forms the basis for identifying positive impact for clients. However, we also aim to be additional in the outcomes we create and accelerate through engagement and voting.

As a truly global asset manager, we are ready to supply new capital to areas of target impact. We will also use our position of ownership to enter into dialogues with companies where we can see the potential to accelerate the good aspects of their operations, while helping to mitigate the negative externalities that naturally exist even in the purest of business operations. Change will take time and require resilience, but this is consistent with many aspects of successful long‑term investing.

Q. How does your portfolio differ from the theme/factor of ESG, sustainability, or even impact?

It is important to distinguish that impact investing is not environmental, social, and governance (ESG) integration, and it is also a different discipline from sustainable investing. It does, however, incorporate both but also takes a step further. In any era of rapid change, it is important to blend an understanding of the historic factor of a company’s impact with the future footprint of a business, in both impact and economic terms.

Impact investing in public equity markets lives in the same domain as other styles of investing. We do not believe there needs to be a sacrifice of return potential, and we believe the opportunity set is unrecognizable from a decade ago. However, impact investing backed by stock‑picking outcomes requires equal if not greater levels of due diligence in research to avoid excessive concentration, crowding, and disappointment. In our view, a forward‑looking perspective, a stable and expert research foundation, and a good level of imagination will be key features of successful investment processes.

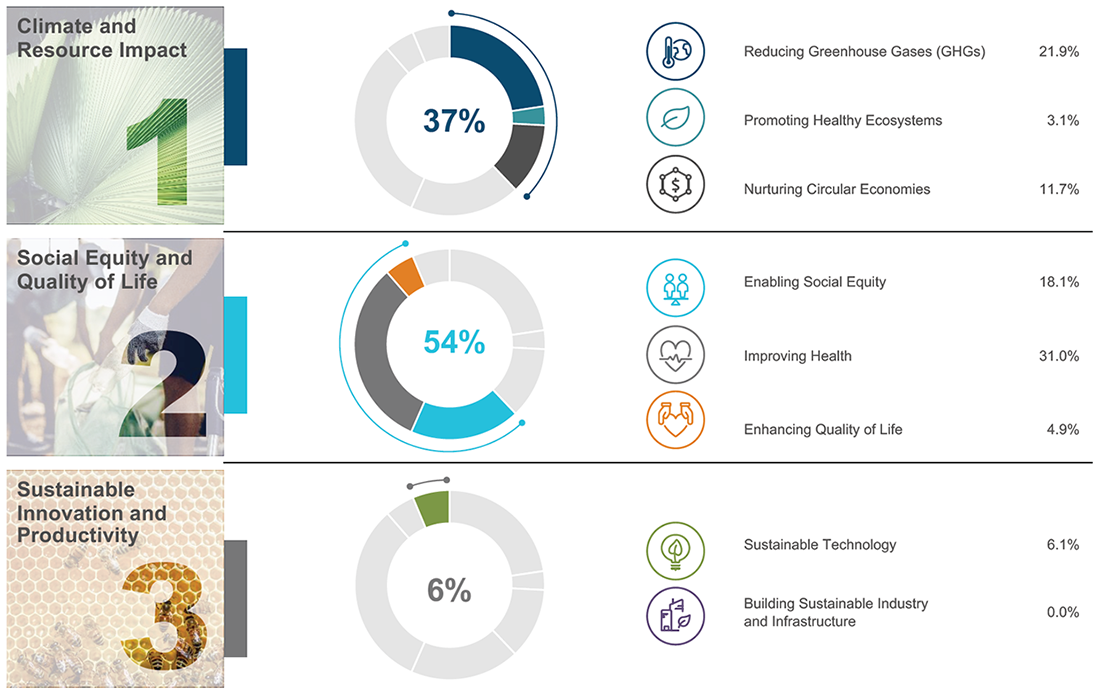

Positioning by Impact Pillar and Sub‑pillar

Global Impact Equity Representative Portfolio

As of March 31, 2021.

Numbers may not total due to rounding.

The representative portfolio is an account in the composite we believe most closely reflects current portfolio management style for the strategy. Performance is not a consideration in the selection of the representative portfolio. The characteristics of the representative portfolio shown may differ from those of other accounts in the strategy. Please see the GIPS® Composite Report for additional information on the composite.

Source: T. Rowe Price uses a proprietary custom structure for impact pillar and sub‑pillar classification.Cash weight was 1.65% as at March 31, 2021.

We start at the bottom‑up level in all we do, blending the best of our fundamental research with the impact insights created by our responsible investment team. Given the breadth of the opportunity set, we apply breadth of ownership, which originates from our global nature and global research capabilities.

We appreciate that many clients may wish to focus on certain themes within the spectrum of impact, but we believe there are benefits in a degree of breadth and long‑time horizon that we provide. Ultimately, success will depend on expert knowledge of bottom‑up stock fundamentals, including the next generation of impact‑oriented private companies that are expected to come to market over the next decade.

To give more detail, we use a decision‑making structure based on three impact pillars (Climate and Resource Impact, Social Equity and Quality of Life, and Sustainable Innovation and Productivity) and eight sub‑pillars, so we can maintain breadth of impact and objectively manage position size. This approach is one of the stages we undertake in impact assessment, in this case identifying current and future revenue alignment with the desired future impact we are targeting. We believe looking forward is one of the key components that differentiates an index with a future outcome, a crucial aspect of successful impact investing.

Aside from the decision‑making framework, we are also very conscious of the need to openly communicate stock selection decisions and impact outcomes to our clients. By looking at a portfolio through the lens of a business’s operations and alignment with the UN SDGs, our approach goes some way to redefining the portfolio along the lines of impact we are seeking to capture, and clients desire evidence of that.

Q. How do you approach the challenge of data and measurement in the impact sphere?

With a forward‑looking perspective and a combination of aggregate analysis where it makes sense, along with individual and holistic analysis where it does not. To be clear, data to measure impact today remain incomplete, while common standards of impact measurement have not been developed on a par with performance/returns analysis. This makes impact measurement inescapably complex.

In an environmental dimension, we are seeing strong and positive change in disclosure that is allowing for better measurement of environmental impact. In a social dimension, our key communication tool will need to focus on singular impact intentions and outcomes versus those intentions, in both discreet and compounded time horizons. The mechanism of any good impact manager to communicate successes and failures will be through the annual impact report attaching to any strategy.

Any system that relies solely on historic data is only part of the perspective you need to measure and capture impact. This is, at times, a strong debating point because evidence is important in the field of impact investing, as clients invest based on values they expect to be upheld.

The challenge for the industry is that impact investing lives in a complex world of risk and opportunity—one of great change and disruption. The solution for us is to be a good partner and contribute to innovation in the field of impact measurement and reporting, helping clients navigate this journey with the data and trust they need. Leveraging multiple dimensions of our research expertise (both responsible and fundamental) while investing for clients in the field of responsible investing and impact reporting will, we believe, be a real advantage over the long term.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

June 2021 / WEBINAR