May 2021 / INVESTMENT INSIGHTS

Implied support: A supporting actor, not the lead role in Asia credit

Chinese SOE defaults reaffirm importance of fundamental research.

Key Insights

- An increase in Chinese SOE credit events signals rising tolerance for defaults as policymakers focus on deleveraging and reducing risks in the financial system.

- Recent volatility in Huarong International bonds highlights the market’s concerns about potential repricing of the government support mechanism.

- Actively assessing SOE fundamentals could help identify high‑quality entities better able to withstand volatility during periods of uncertainty.

Since the 1970s, China’s state‑owned enterprises (SOEs) have undergone continuous reform efforts guided by central government policies. After decades of consolidation, streamlining operations, implementing market‑based ownership mechanisms, and improving corporate governance, the SOEs of today are significantly different entities from before.

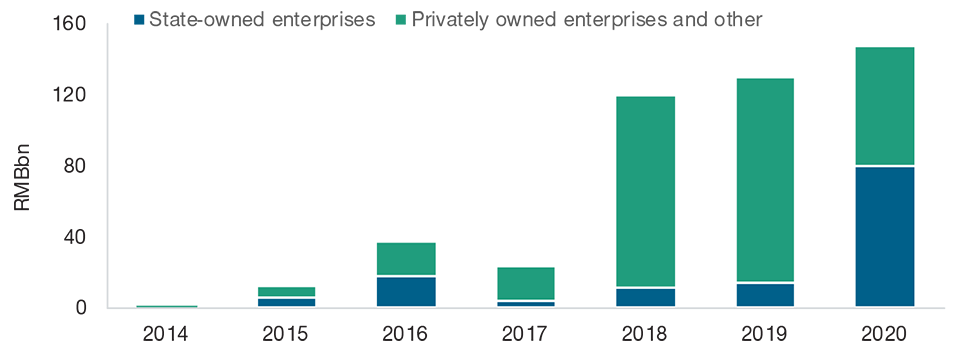

The market expectation for implicit government support has also changed, especially given China’s commitment to deleveraging and reducing risks in the financial system. In 2020, SOEs accounted for just more than half of onshore bond defaults in China, a significant reversal of the previous trend where private enterprise produced the majority of defaults. With a combined sum of about RMB 80 billion in default, that amount marks the highest level since 2014 when China first allowed onshore defaults as part of broader market‑based reforms.

Most recently, China Huarong Asset Management, which has been returning its focus to its traditional distressed asset management business since 2018, saw sharp trading volatility in its offshore U.S. dollar‑denominated bonds after delaying the release of its annual results due on March 31. This incident renewed questions about how to price in the expected level of implicit government support for troubled SOEs. With heightened uncertainty over how reform efforts could impact SOEs going forward, we feel that it is imperative for Asia credit investors to recognize that not all SOEs are in the same boat. Utilizing a rigorous, bottom‑up research process could help to identify the high‑quality entities that are likely better equipped to withstand any unexpected volatility.

SOE Reform Has Sought to Make Public Sector More Self‑Sufficient

SOEs originally formed the backbone of China’s modern economy and were tasked with meeting official production quotas. Although the role of private enterprise has since surged in tandem with China’s economic boom, SOEs continue to occupy a significant space in China’s economy and account for an estimated one‑quarter of industrial assets.1 There are well over an estimated 100,000 SOEs in China, with the very largest among them accounting for a significant portion of the country’s representation in the dollar‑denominated Asia credit asset class.

Successive reforms starting in the late 1970s sought to make SOEs more efficient by granting them greater operational autonomy and raising transparency standards. The government also prioritized oversight for SOEs in strategically important areas, like defense, agriculture, railways, and equipment manufacturing, while encouraging consolidation in non‑core areas.

In line with these efforts, the number of central SOEs decreased from 106 at the end of 2015 to 98 in 2019. The State‑owned Assets Supervision and Administration Commission also reported that, by the end of 2019, the disposal had been finalized for 2,041 so‑called zombie enterprises, which typically refers to companies unable to fund investments needed for future growth. A three‑year action plan was also unveiled in 2020 to enhance SOEs’ core competitiveness that includes steps like encouraging them to dispose of nonessential business and relieving them of obligations to undertake social programs.

Recent SOE reforms have been undertaken against the backdrop of China’s attempt to shift away from an export‑led economic model to one that is more balanced and focused on higher-quality and more sustainable growth. In support of these aims, the government has committed to reducing leverage in the financials sector, while taking care not to cause systemic impacts across the economy and capital markets.2 The intention behind this was made clear in the report issued by the Ministry of Finance at the recent convening of the National People’s Congress in April when it highlighted a commitment to “step up management of local government debt, make solid progress in defusing risks related to hidden local government debt, and promote sustainable fiscal development.”

Recent SOE Defaults Have Raised Questions About Implicit Government Support

Just as policymakers have ramped up efforts to make the public sector more self‑sufficient, they have also embarked on a path of financial deleveraging and credit cleanup, while making it clear that government support would not be extended to all SOEs. There have been some examples of this already in smaller, local SOEs.

In October, Brilliance Auto Group, which operates a joint venture with BMW, defaulted on one of its private bonds and began restructuring proceedings after being declared bankrupt the following month. Another example, Yongcheng Coal and Electricity Holdings Group, a coal miner based in Henan Province, defaulted on a RMB 1 billion loan in November and was later prohibited from issuing debt for one year. The same month, Tsinghua Unigroup, a technology company affiliated with one of China’s top universities, defaulted on a RMB 1.3 billion bond and two dollar bonds valued at about USD 1 billion.

In response to the spate of defaults, China’s interbank bond market regulator suspended China Chengxin International Credit Rating Group, a joint venture with Moody’s Investors Service, from issuing debt ratings for three months, citing a lack of due diligence in its research process. We believe that decision was made to restore investor confidence.

Increased Defaults From Public Sector

(Fig. 1) Onshore renminbi‑denominated bond defaults by SOEs and private enterprises

As of December 31, 2020.

Source: T. Rowe Price analysis with WIND data.

At the same time, the China Securities Regulatory Commission also outlined a set of key guidelines for future development, including the orderly and slow release of risks in key areas such as bond defaults. As a result, we expect the government will continue to display a rising tolerance for SOE defaults as part of its larger commitment to reducing risks in the financial system.

Huarong International Spread Widening Indicates Repricing of Government Support Assumptions

Questions regarding implicit government support for SOEs resurfaced when China Huarong failed to report its annual results in Hong Kong by a March 31 deadline, citing in a stock exchange filing that the auditor would require more time to audit the financial information for the previous year. In response, Moody’s, Fitch Ratings, and S&P Global Ratings all announced that the company had been placed under review for a potential ratings downgrade due to uncertainty caused by the lack of transparency.

The developments triggered significant volatility in the offshore dollar bonds issued by Huarong International, a wholly owned subsidiary of China Huarong. We feel that this volatility was partly due to the size of the parent company, China Huarong. Established in 1999 by the government to acquire distressed debt following the Asian financial crisis, China Huarong is one of the country’s largest asset managers and is majority‑owned by the Ministry of Finance. Since the arrest of its former chairman, Lai Xiaomin, in 2018, it has sought to restructure its operations and renew focus on its traditional business of distressed asset management.

China Huarong’s outstanding debt saw significant spread widening since delaying the release of its financial results. The market’s concerns on Huarong International’s dollar‑denominated debt has, in part, been driven by the structure of these bonds. Huarong’s dollar bonds have typically been issued out of special‑purpose vehicles with guarantees from a financially weak international subsidiary, but only a keepwell agreement with the ultimate parent, China Huarong.

Other dollar bond SOE issuers also saw spreads widen initially but since tighten over the same time frame, suggesting that contagion was limited to the most obviously troubled areas of the bond market.

We believe investors should be cautious about giving up too much credit spread for implied support, as governments may only react to provide support for state entities after markets have repriced risk of these uncertainties. Going forward, Asia credit investors should actively assess Chinese SOEs issuing dollar bonds on the basis of their standalone fundamentals with the understanding that implicit government support may not be readily available to troubled or underperforming entities.

In this environment, strategic investors have an opportunity to potentially capitalize on price dislocations through informed security selection. We also believe that diversifying exposure within the region and optimizing allocations within specific markets may help manage volatility during periods of market reform.

What We're Watching Next

SOE reforms have been underway for decades in China as the government sought to optimize efficiency in the public sector and mitigate financial risks. We expect this is likely to continue and could result in a growing tolerance for defaults, reaffirming the importance of monitoring the latest developments and limiting exposure to underperforming SOEs.

The overall China dollar bond market saw sharp volatility recently amid renewed questions about government support for SOEs. Going forward, we feel that it is imperative for Asia credit investors to utilize a rigorous, bottom‑up research process that will aim to identify high-quality entities that are potentially better equipped to withstand any unexpected volatility.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.