May 2021 / INVESTMENT INSIGHTS

Emerging Markets Should Largely Keep Pace With U.S. Rebound

Yield curves may steepen as growth recovers

Highlights

- Growth: Although different emerging markets (EM) countries are at very different stages of their recoveries, growth across EMs as a whole is expected to rebound strongly this year, largely keeping pace with the U.S. growth rebound.

- Inflation and monetary policy: While headline inflation in EMs may recover quickly, core inflation will likely take longer to return to pre‑coronavirus pandemic levels. Although a few EM central banks have hiked rates this year and others may follow, most are expected to remain on hold, with more serious hikes expected in 2022.

- Fiscal policy: Emerging markets are on course to undergo fiscal consolidation at a faster pace than most developed economies. Elevated debt‑to‑GDP ratios are expected to stabilize over the next few years, with Brazil and South Africa being the focal points over debt sustainability.

- Rates and currencies: EM yields are low by historical standards but remain attractive compared with depressed U.S. yields. A gradual recovery in EM economies should lead to some curve steepening. EM currencies look fairly priced at the moment.

- Ratings: EM ratings have fallen from pre‑pandemic levels, though perhaps not by as much as expected. Colombia, India, and Romania are at risk

Growth

EM growth recovered during the second half of last year, but most countries’ gross domestic product (GDP) remains below 2019 levels. The recovery has been led by exports and industrial production, which were largely back to 2019 levels by the third quarter of last year, while services and investment/construction continued to lag. However, data for the fourth quarter of 2020 suggest that investment/construction has begun to bounce back in some countries.

Different EM countries are at very different stages of their recoveries and their paths toward fiscal consolidation, which will inevitably influence the speed of overall recovery across EMs.

We believe monetary conditions will remain relatively loose for much of the year, although some central banks may begin to hike rates and markets will start to price in further hikes next year.

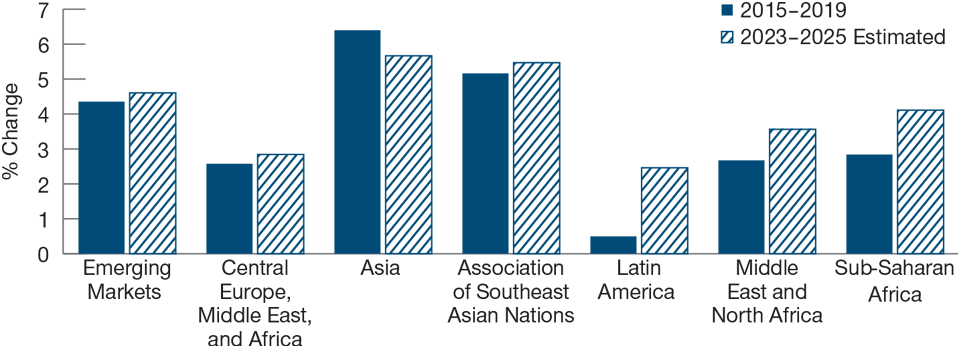

Despite the enormous U.S. fiscal stimulus, EMs are expected to largely keep pace with the U.S. growth rebound this year. The International Monetary Fund (IMF) is expecting growth for EMs as a whole to bounce back from ‑2.4% last year to 6.3% in 2021, then 5% in 2022. It is predicting that EM growth in the period 2023–2025 will exceed that of the period 2015–2019 (Figure 1). Growth could be even stronger than this if the spillover from the U.S. fiscal stimulus is particularly strong or the spending down of savings accumulated during the crisis is more forceful than expected. A swift resumption of the credit cycle, which has been contained for a number of years, could add a further impetus to growth.

Downside risks include potential delays to vaccination programs in some countries and subdued growth in China as it seeks to normalize policy now that the pandemic is under control. Any anticipation of policy tightening in the U.S. or rising inflation concerns could also keep EM growth in check.

Inflation and Monetary Policy

Inflation in EMs was low in 2020, which is unsurprising given the collapse in growth and commodity prices (although there were some exceptions). Core inflation has been structurally falling since 2015, likely reflecting weaker demand conditions over the period versus the prior five years. While headline inflation—which generally follows oil prices—may recover quickly, core inflation is likely to rise more slowly, given the time it will take for output gaps to close and activity to normalize.

EM Growth Is Set to Bounce Back

(Fig. 1) Growth should be faster in 2023–2025 than it was in 2015–2019

As of March 31, 2021.

Source:

IMF World Economic Outlook database/Haver Analytics.

Inflation uncertainty is probably higher during this economic recovery than in previous ones due to uncertainty over the pace of recovery in developed markets. Overall, however, the rebound in inflation in EMs is likely to remain modest, given that inflation is likely to remain at pre‑pandemic levels in much of Latin America and Asia.

EM central banks have been managing their monetary situations fairly prudently during the pandemic. Most are expected to remain on hold this year, although some—such as Mexico and Indonesia—have cut rates, others—such as Brazil and Russia—have hiked rates, and still others—such as Chile and the Czech Republic—are expected to hike rates at some point this year. More serious hikes are expected in 2022. Given expectations that the Federal Reserve will keep rates lower for longer, EM central banks should find themselves ahead of the U.S. in hiking rates even if there is something of a lag in their full recoveries this year.

On the financial side, most EM countries went into the crisis with several years of credit cycle consolidation behind them. Although financial conditions in EM ex‑China have become very easy due to lower external funding costs and low domestic rates, credit cycles in most countries remain tepid.

Fiscal Policy

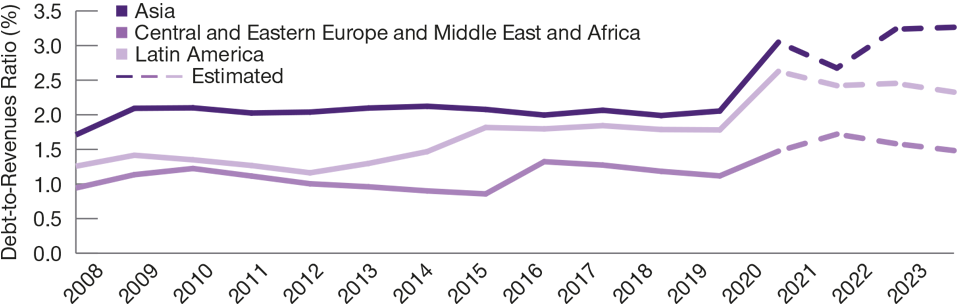

The fiscal deficits that arose in emerging markets last year were heavily driven by declining revenues as there were limited increases in spending. I believe fiscal consolidation will be driven by a mix of spending cuts and cyclical revenue rebounds and will occur at varying paces across regions—Asia, for example, is likely to maintain loose fiscal policies for longer than other EM regions. Overall, emerging markets are on course to undergo fiscal consolidation at a faster pace than developed markets.

The crisis has resulted in debt‑to‑GDP ratios spiking in many countries. The IMF expects these to largely stabilize in EMs, with ratios increasing only slowly over the next few years. Interest rate growth differentials are expected to revert to pre‑coronavirus levels, while net borrowing is likely to be slightly higher than normal. Contingent liabilities could push debt trajectories higher.

Higher‑rated countries are expected to continue to use their balance sheets to support their economies, while lower‑rated countries are expected to begin fiscal consolidation earlier. Brazil and South Africa remain the focal points for debt sustainability concerns among major EM countries: Brazil’s effort to keep rates low to contain debt service has been challenged by inflation and growing pressure for rate hikes; South Africa’s policy of maintaining high real rates to support its assets and maintain confidence in the rand has meant that the average interest rate on its debt is higher than its growth rate, potentially cannibalizing private investment. Both countries need to demonstrate that they have the political ability to make progress toward fiscal consolidation during 2021/22.

Latin America Expected to Lead EM Fiscal Consolidation

(Fig. 2) Asian countries are likely to maintain looser policies for longer

As of March 31, 2021.

2021–2023 figures are estimated.

Source: IMF Fiscal Monitor database/Haver Analytics.

Rates and Currencies

While EM yields are historically low in both absolute and real terms, they remain attractive compared with depressed U.S. yields. Only a small number of countries currently have real yields that are higher than their historical average, most notably China, Thailand, and Colombia.

A gradual recovery in EMs, with central banks only moving tentatively to hike rates this year, should lead to curve steepening. The market has priced this in to some extent: The spread between two‑year and 10‑year sovereigns from a number of countries are relatively steep versus history. In a number of countries, curves are at their steepest for several years.

EM currencies have had a mixed time since rallying in November/December as, in my view, the U.S. recovery temporarily pulls ahead on the back of vaccination progress and fiscal stimulus. Emerging markets should pull some of that gap back as the year goes on as U.S. stimulus has positive spillover effects on EM trade and EM countries begin to catch up on vaccinations.

In general, EM currencies remain fairly priced (the manufacturing exporters) to cheap (the commodity exporters) on a real adjusted exchange rate basis. Only among the strongest exporting countries during the crisis are currencies slightly expensive relative to history.

Ratings

EM credit ratings have unsurprisingly fallen from pre‑pandemic levels, though perhaps not by as much as expected given the size of the shock. Although there was a sizable deterioration in fiscal metrics and external debt, an improvement in currency reserves has helped to mitigate the shock. Credit agencies have downgraded more aggressively than T. Rowe Price analysts, although the biggest downgrades appear to be in the frontier markets of Latin America and Sub‑Saharan Africa.

Among the major EM countries, South Africa and Mexico have been on the receiving end of across‑the‑board downgrades, while several other countries were downgraded by one agency. Colombia, India, and Romania are at risk of losing their investment‑grade status, with at least two negative outlooks on BBB‑ ratings. Turkey also looks vulnerable.

Issuance got off to a strong start this year and markets seem open to funding most EM countries, even lower‑rated ones. The market is dominated by short‑term debt that should be easy to roll over in the current market environment. Despite concerns about EMs’ ability to manage the crisis and the fact that there are more than 70 EM countries eligible for debt relief under the World Bank’s Debt Service Suspension Initiative, none of the key EM countries are under significant stress at the moment in my opinion.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

May 2021 / MULTI-ASSET SOLUTIONS