November 2020 / INVESTMENT INSIGHTS

Navigating Fallen Angels in the Post-Coronavirus Landscape

Uncertainty means investors should proceed with caution

Key Insights

- Investment‑grade bonds downgraded to junk, known as fallen angels, have become a prevalent part of the credit landscape due to the coronavirus crisis.

- While unprecedented monetary easing and evidence from history suggest fallen angels could perform well, potential pitfalls ahead call for caution.

- Headwinds, including a second coronavirus wave and the shape of the economic recovery, mean investors should tread diligently rather than just follow trends.

The coronavirus pandemic led to the shuttering of wide parts of economies worldwide, and while many countries and companies have reopened or are reopening cautiously, the impact this has had on credit is apparent. The first half of the year was littered with record numbers of closures, defaults, and ratings downgrades. This has included a record amount of debt downgraded from investment grade to junk—so‑called “fallen angel” bonds.

At first glance, one could think of this as an opportune time to jump on these downgrades, given their historical tendency to relatively outperform. However, the unparalleled market environment and uncertain times ahead mean investors should take stock before trying to take advantage.

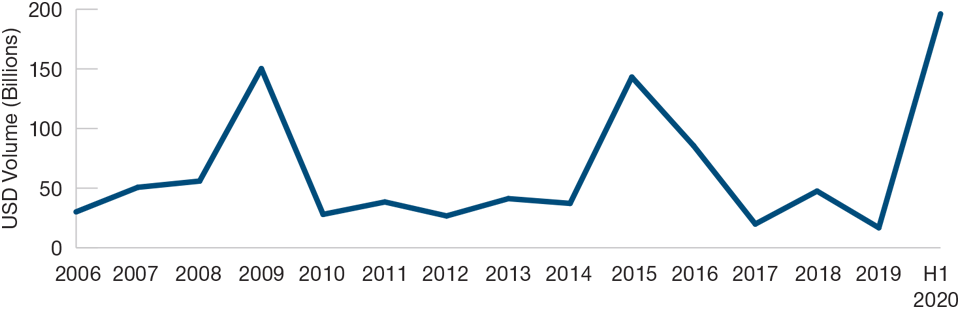

An Unprecedented Year of Fallen Angels

(Fig. 1) The first half of 2020 already broke the record for fallen angels (by dollar amount)

As of June 30, 2020.

U.S.-dollar denominated universe.

Source: J.P. Morgan Chase (see Additional Disclosure).

A Record‑Breaking Amount of Fallen Angel Debt

While fallen angels—the term used to describe bonds that initially received investment‑grade credit ratings on issuance but have subsequently been downgraded to sub‑investment grade—are not a new phenomenon, the scale of the downgrades seen in the first half of 2020 dwarfs what we’ve seen previously. March saw more than USD 90 billion in downgrades from investment grade, nearly twice as much as the previous monthly record of USD 48 billion in 2005. By the end of June, 2020 had already seen the highest number of fallen angels by dollar amount on record, with some USD 197 billion.

Cyclical industries in particular, such as transportation and energy, have been hit hard. Even household names have not been spared, with carmaker Ford seeing its USD 36 billion debt pile consigned to high yield in March.

History Suggests the Time Is Now

Viewed from a historical perspective, this surge in fallen angel volume could provide an opportunity for investors operating in the investment‑grade and high yield spaces. Fallen angel securities tended to outperform those other two fixed income asset classes over the last two decades. According to T. Rowe Price research, fallen angels globally have outperformed investment‑grade and high yield counterparts by around 3% or more on an annualized basis since 1998.1

This dynamic is the result of the forced and reactionary selling that fallen angels face when downgraded. Once a bond slips out of the investment‑grade universe, some vehicles, such as passive investment‑grade exchange‑traded funds (ETFs), will be forced to sell those securities. The bonds are also likely to face reactionary selling as well from investors spooked by a downgrade, further depressing their price. For active managers, this provides an opportunity to pick up otherwise healthy credits that have been discounted due to a downgrade.

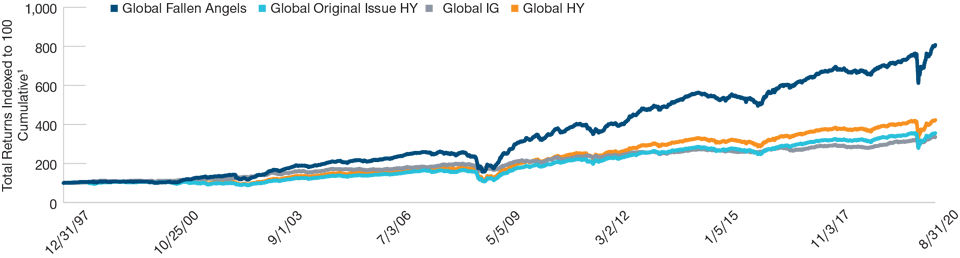

Fallen Angels Have Outperformed Since the Global Financial Crisis

(Fig. 2) On a total return basis, investment‑grade and high yield peers lag behind

As of August 31, 2020.

1 Cumulative/annual returns calculated from daily Bloomberg data. Indices used for reference: Global Fallen Angels = ICE BofA Global Fallen Angel High Yield Index, Global Original Issue HY = ICE BofA Global Original Issue High Yield Index, Global IG = ICE BofA Global Corporate Index, Global HY = ICE BofA Global High Yield Index.

Source: T. Rowe Price research.

Unprecedented Easing Provides Further Support

While historical analysis may provide support for fallen angel‑filled markets, there are features of the current market environment that could further boost fallen angel bonds. The most apparent has been the unprecedented wave of support from major central banks, both in terms of its depth and breadth. As well as cutting rates and initiating asset purchase programs, some institutions have targeted fallen angels directly. In particular, the Federal Reserve announced in April that it would begin to buy corporate bonds in the high yield segment if they have been downgraded from investment grade owing to coronavirus‑induced problems. A month later, the Fed began purchases of corporate bond ETFs. The European Central Bank, meanwhile, has said that it would accept debt downgraded to junk after April as collateral from banks in return for its ultra‑cheap loans; however, this is not yet included in its bond‑buying program. While the ceiling of individual performance will be driven by a bond’s fundamentals, this broad‑based support of the downgraded corporate market should help limit the potential for fallen angels to lose further value.

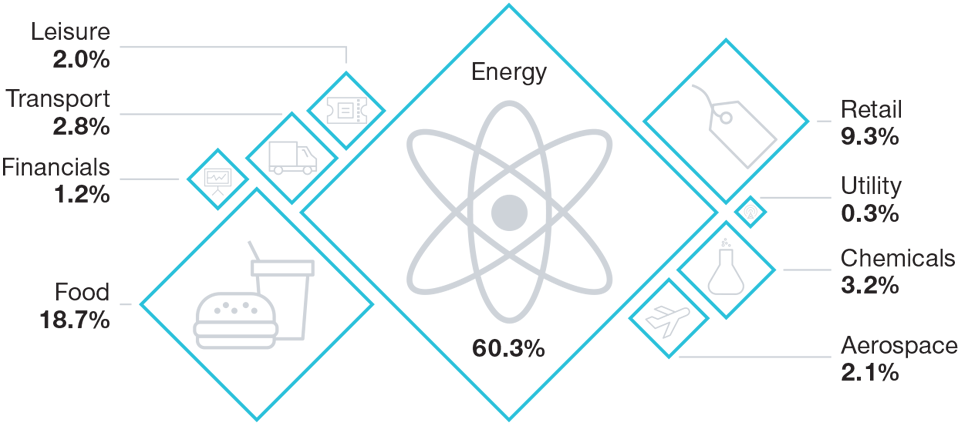

The Energy Sector Dominates the Fallen Angel Landscape This Year

(Fig. 3) Cyclical industry credits in particular have suffered due to the coronavirus worldwide

As of June 30, 2020.

Source: T. Rowe Price research. USD-denominated fallen angels.

Fresh Outbreak, Slow Recovery Could Clip Their Wings

To benefit from the new set of fallen angels, however, it is not wise to blindly purchase bonds and expect a rising tide to lift all boats. A number of potential pitfalls lie ahead:

Slow Economic Recovery: For instance, spread‑tightening expectations are intertwined with a quick rebound of the global economy post‑coronavirus. Should the recovery be slower than expected, the risk of higher default rates among the asset class increases.

Further Coronavirus Impacts: Reemerging concerns over fresh coronavirus outbreaks, and the reintroduction of stricter measures to mitigate them, could stress fallen angel bonds further.

With these headwinds in mind, it is vital that investors navigate these challenges with rigorous security selection. In particular, this includes recognizing which sectors are more at risk and potentially more vulnerable to a second spike. So far, for example, many cyclical industries have borne the brunt of the pain from the coronavirus, with industries such as transportation, energy, leisure, and retail making up 75% of fallen angels. Overall, we anticipate that USD 300 billion worth of non-financial investment grade issuers’ debt could be downgraded to junk by the end of 2020. In our view, sectors we consider overly COVID‑sensitive and would look to avoid include airlines, transportation, and retail real estate investment trusts.

We are hopefully past the worst of the coronavirus pandemic. However, for financial markets, corporate credits, and investors, the road ahead is still a long one as the shape of a recovery takes form. Investors need to operate diligently in an environment where credit is by no means certain, rather than simply trust that history can repeat itself when it comes to fallen angels.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

November 2020 / INVESTMENT INSIGHTS