March 2021 / INVESTMENT INSIGHTS

Why Credit Investors Need to Become Active Duration Managers

The importance of duration for credit performance and five ways to improve it

Key Insights

- Duration has become a key driver of credit returns over the past decade, highlighting the importance of active duration management for credit investors.

- Techniques to manage duration include using structural curve positioning, allocating across regions and currencies, and using derivatives.

- Actively managing the total duration of a portfolio by adjusting duration exposure for short periods can also significantly enhance returns.

Credit investors typically pay little attention to duration, seeing themselves primarily as bottom‑up investors who specialize in sector and security selection. However, over the past decade, duration has become a major driver of credit total returns, making it increasingly difficult to ignore. Managing duration is likely to be a key source of performance for credit investors in the future—giving investors who are skilled in it a major potential advantage.

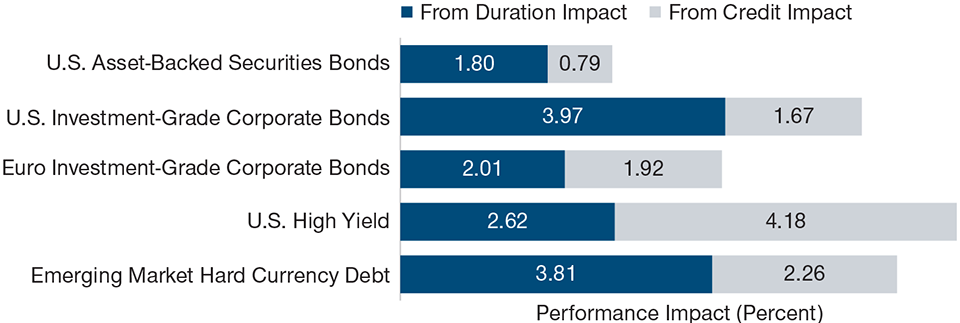

Duration Has Been a Major Driver of Credit Returns Over 10 Years

(Fig. 1) In most strategies, it has exceeded returns from credit impact

As of December 31, 2020.

Past performance is not a reliable indicator of future performance.

Sources: Bloomberg Barclays U.S. Corporate Bond Index, Bloomberg Barclays U.S. ABS Index, Bloomberg Barclays Euro Corporate Bond Index, Bloomberg Barclays U.S. High Yield Bond Index, and Bloomberg Barclays EM Sovereign and Quasi Sovereign Bond Index (see Additional Disclosure). Analysis by T. Rowe Price.

The fixed income market has evolved considerably since the global financial crisis. Vast injections of central bank liquidity have driven down bond yields and encouraged corporate issuers and investors to extend out the curve—bonds of more than 10 years’ maturity now comprise more than 28% of the Bloomberg Barclays Global Aggregate Corporate Index (As of December 31, 2020). The average credit investor now holds a lot more duration than in 2009: The duration of the index has increased by around two years, or around 1.4 times, since then. And while credit strategies have performed very well over that time, much of that performance has been effectively “engineered” by central banks supressing sovereign bond yields. Changes in underlying risk‑free rates—the duration impact—have accounted for the majority of the returns of U.S. and European investment‑grade debt, emerging market hard currency bonds, and U.S. asset‑backed securities over the past 10 years and have contributed significantly to the returns of U.S. high yield strategies using index returns as a proxy (Figure 1).

The Post‑pandemic Recovery May Pave the Way for Inflation

The strong influence of duration on credit returns has not been a problem while yields were trending lower. However, with most of the major central banks at their lower bound on interest rates, the downtrend in yields is probably at its end. Indeed, the market has already started to price a return to more normal conditions as vaccination programs ramp up and fiscal stimulus takes the reins from monetary policy. If economies bounce back quickly once restrictions are lifted, anticipation may build about central bank rate hikes and the cessation—or slowing down—of asset purchase programs, posing a risk for credit investors.

This has echoes of 2013, when market panic over the prospect of the U.S. Federal Reserve cutting back its quantitative easing programs triggered the “taper tantrum” as government bonds sold off dramatically, causing large losses for credit investors (the Bloomberg Barclays Global IG Corporate USD Hedged Index declined 5% in less than two months). Although we believe there is no immediate prospect of rate hikes, the enormous amount of monetary stimulus injected into the global economy since the coronavirus swept the world will have to be reduced at some point and could potentially cause sovereign bond yields to spike even higher.

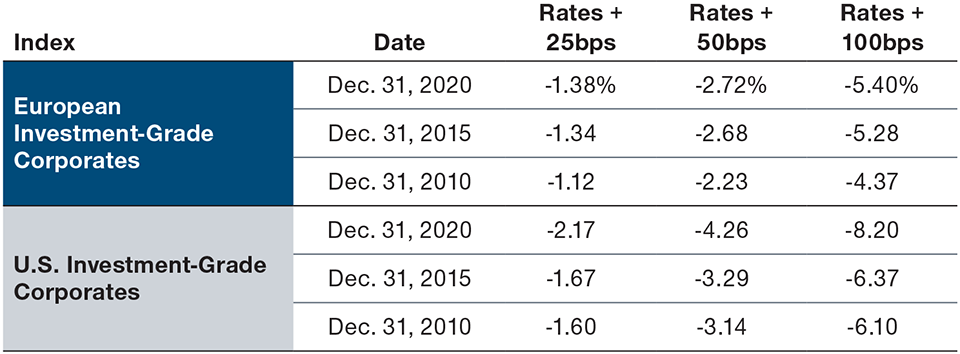

Credit Duration Has Increased Since 2010

(Fig. 2) U.S. and European investment‑grade indices have become more sensitive to rate rises

As of December 31, 2020.

Shows the hypothetical performance impact from different potential increases in interest rates based on index composition as of each date.

Sources: Analysis is based on the Bloomberg Barclays Euro Corporate Bond Index and Bloomberg Barclays U.S. Corporate Bond Index. Bloomberg PORT (see Additional Disclosure). Analysis by T. Rowe Price. Analysis based on the Bloomberg PORT full valuation model. The model assumes a parallel Treasury curve movement. Stress testing is hypothetical, for illustrative purposes only, and figures do not represent actual investment results. Actual investment results may differ materially.

This is not the main risk to credit investors, however. Central banks are determined to avoid another taper tantrum and equally determined to avoid a premature withdrawal of monetary stimulus, preferring instead to maintain easy liquidity conditions until the economic recovery is well advanced. This means the greatest risk to credit is that the surge in economic activity after the coronavirus restrictions are lifted fuels inflation, resulting in a further steepening of the yield curve—and losses for long‑duration bond portfolios.

Duration Management in Practice

Five ways to actively manage interest rate risk

The current combination of very low sovereign yields and credit spreads puts credit bondholders in a vulnerable position. Long‑duration sovereign and investment‑grade credit bonds have already suffered losses this year as vaccine rollouts, economic recovery, and rising inflation expectations move into view. In the past, holding corporate debt has often helped to mitigate the impact of sovereign yield spikes as credit duration was lower and spreads were able to compress, cushioning the blow from rising risk‑free rates. This diversification impact has diminished over the past decade, however, as U.S. and European investment‑grade corporate indices have become more sensitive to rate rises (Figure 2).

Dynamically Managing Duration Risk

This does not mean, however, that credit investors should systematically reduce the duration of their bond portfolios. On the contrary, we believe that duration will continue to provide some beneficial properties to credit portfolios, particularly as the correlation between sovereign bond and credit returns should remain low. This means that during higher‑volatility “risk‑off” periods in financial markets, the duration component of credit should offset some of any spread widening, helping to reduce the overall volatility of the portfolio. Credit investors who systematically reduce the duration of their bond portfolios must be prepared to accept higher volatility in their returns, especially during more turbulent times.

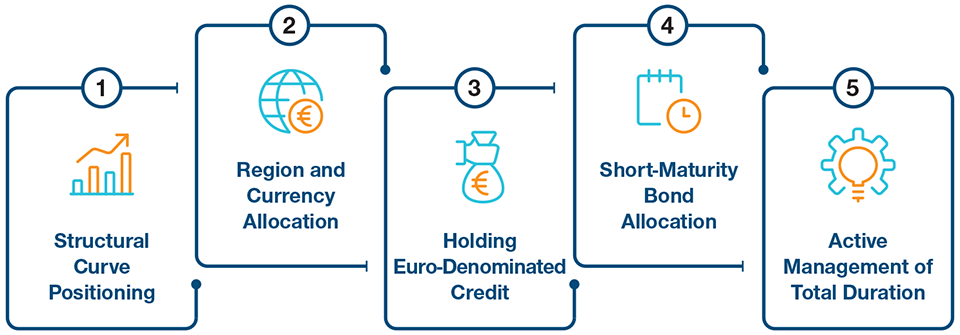

A better approach, in our view, would be to try to mitigate the impact of rising yields through portfolio construction and dynamically managing duration risk. There are five ways to do this:

1. Structural Curve Positioning: One way to do this would be to use structural curve positioning, specifically by adopting curve steepener initially, followed by a curve flattener. Curve steepeners are typically constructed by underweighting the long end of the credit curve and using short‑maturity government bond futures or interest rate swaps to make up the lost duration. They typically work well when markets are concerned about inflation and the possibility of rate hikes in the more distant future, and they have the added benefit of improving the carry and roll‑down profile of the portfolio, which should boost returns even if the yield curve remains unchanged. Once central banks start to withdraw monetary accommodation, however, it may be prudent to consider shifting to a curve flattener position. Curve flatteners should outperform if central banks are able to anchor long‑term inflation and rate expectations later in the cycle.

2. Allocating Across Regions and Currencies can also help to mitigate duration risk. Many investors are wary of emerging market corporate debt, for example, as they regard it as too high risk. Yet there are many investment‑grade issuers in emerging markets these days, and emerging market credit has lower duration as well as higher yields than developed market credit—at the end of December, the Bloomberg Barclays Emerging Markets USD Aggregate Corporate Index had a yield of 3.81% and a duration of 4.73 years, compared with a yield of 1.37% and a duration of 7.49 for the Bloomberg Barclays Global Corporate Index. Allocating to emerging market credit can, therefore, should provide greater yield while simultaneously lowering duration risk.

3. Holding Euro‑Denominated Credit may also help to offset duration risk in the current environment. The European Central Bank is likely to be slower to hike interest rates than other central banks, and when it does eventually raise rates, it will probably be by less. This means that, over the longer term, the euro yield curve could be more resilient to sell‑offs than the U.S. dollar yield curve and, therefore, that euro‑denominated corporate bonds should offer a degree of insulation against future spikes in yields.

4. Allocating to Shorter‑Maturity Bonds is an obvious way of reducing duration risk, but one that comes with the disadvantage of providing less yield than investing in longer‑dated bonds. This can be overcome by using derivatives in the form of credit default swap indices (CDX). Investment‑grade CDX offer a way of gaining exposure to a benchmark without taking on the duration risk of longer‑dated securities. Combining an allocation to short‑duration bonds with exposure to investment‑grade CDX therefore enables an investor to construct a portfolio that has similar carry and spread to the benchmark, but with less duration.

5. Active Management of Total Duration: Finally, it is worth pointing out the potential benefits of actively managing the total duration of the portfolio. While significantly reducing the overall duration of a portfolio is probably not a desirable long‑term option, adjusting the overall duration exposure for short periods, depending on circumstances, can significantly boost returns. Doing this well will not be possible for everyone. It requires a rigorous monitoring of macroeconomic factors and government bond markets, on top of developments within industries and individual securities, which may not come naturally to all credit managers given their typical preference for focusing on bottom‑up analysis.

Duration Management Set to Become a Key Driver of Returns

Lockdown measures imposed to control the spread of the coronavirus led to the worst global economic contraction since World War II. The rollout of vaccination programs across the world is expected to fuel a rapid recovery this year, although some economies will require continued government support for a while yet. As the recovery gathers momentum, inflationary pressures may build, leaving central banks with the difficult choice of when to begin raising rates: Hiking rates too early could damage a fragile recovery; doing it too late could mean inflation rises too quickly, meaning more aggressive hikes will be required further down the line.

We believe central banks will be reluctant to raise rates in the near term because of the vulnerable state of the global economy. However, if inflation pressures build, anticipation of future rate rises may cause yield curves to steepen. As duration in credit has steadily risen over the past decade, corporate bonds no longer offer the same degree of insulation against sovereign yield spikes as they did in the past. Credit investors who add dynamic duration management to their traditional skills of sector and security selection are therefore likely to perform better over the next few years than those who do not.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.