January 2021 / MULTI-ASSET SOLUTIONS

Creativity in a Low-Yield Era

Bond investors could face more challenging markets in 2021

Strengthening economic recovery in 2021 would carry risks for bond investors, warns Mark Vaselkiv, chief investment officer, Fixed Income. He says investors will need to be creative in seeking out fixed income sectors—such as floating rate bank loans and emerging market corporates—that potentially can do well in a rising interest rate environment.

Massive infusions of central bank liquidity successfully stabilized global credit markets in 2020, even as a pandemic‑driven flight to quality pushed already‑low sovereign yields even lower. These dual trends produced strongly positive returns across most fixed income sectors.

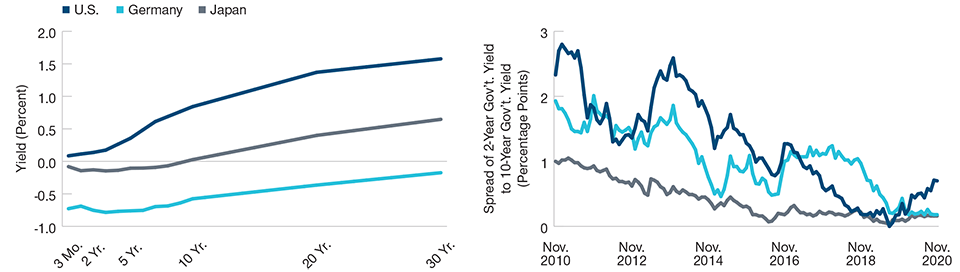

Moving into 2021, however, investors face a more challenging environment, Vaselkiv says. With short‑term yields at ultralow or negative levels and the U.S. yield curve steepening as economic growth and inflation expectations revive (Figure 1), interest rate risk could become a critical issue, he cautions.

Credit markets also no longer appear as attractive as they did after central banks launched their rescue operations in 2020, Vaselkiv says. With investment‑grade (IG) and high yield credit spreads back closer to their historical norms—despite the lingering effects of the pandemic—active sector and security selection are likely to play more critical roles in seeking yield and managing risk in 2021.

We think it will take significant creativity to find attractive opportunities in such a low interest rate environment,” Vaselkiv says.

Creativity, Vaselkiv notes, could mean moving further out the credit risk spectrum, potentially increasing allocations to floating rate loans and other low‑duration assets, and seeking opportunities in ex‑U.S. debt markets. Skilled credit analysis could be crucial to success.

Yield Curves Are Lower but Steeper Than at the Beginning of 2020

(Fig. 1) Sovereign yield curves (left) and yield curve slopes (right)

As of November 30, 2020.

Past performance is not a reliable indicator of future performance.

Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

An Expanded Credit Universe

For credit investors, the flood of new U.S. dollar‑denominated corporate issuance seen in 2020—an estimated USD 2 trillion in investment‑grade debt and more than USD 500 billion in high yield debt—offers both potential opportunities and additional risks, Vaselkiv says.1

On one hand, yields in the credit universe still appear attractive on a relative basis, in Vaselkiv’s view. While many companies have increased their debt loads, he says, in many cases liquidity ratios actually have improved. This should help businesses in cyclical sectors such as energy, airlines, and lodging fend off insolvency until economic conditions normalize.

However, ample financing also could allow structurally weak firms to survive even though their longer‑term prospects for profitability appear dim. “We may end up with a universe of companies that limp along for the next five to seven years just because the credit markets keep them afloat,” Vaselkiv says.

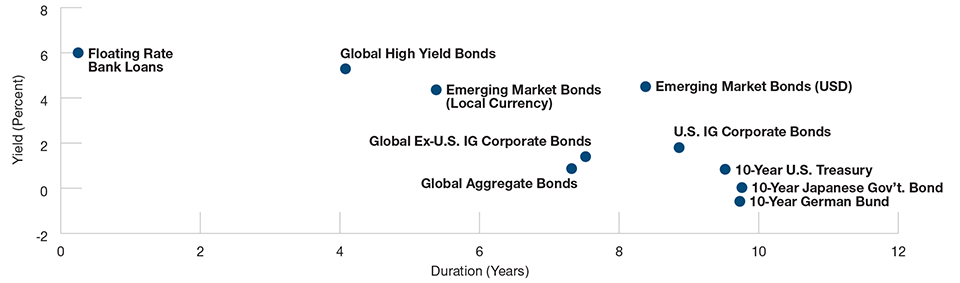

In an environment where short‑term rates are at or close to zero, but prospects for a post‑pandemic recovery appear to be brightening, duration—a key measure of interest rate risk—could become a top issue for many fixed income investors in 2021, Vaselkiv says.

Extended durations for high‑quality sovereigns and investment‑grade corporates (Figure 2) mean that even modest upticks in interest rates and inflation could produce significant capital losses on those assets, he warns.

Potential Opportunities in Floating Rate and Emerging Market Debt

Floating rate bank loans—syndicated loans to companies that are then sold to mutual funds and other institutional investors—offer potentially attractive advantages in this environment, according to David Giroux, CIO, Equity and Multi-Asset. Bank loans sit higher in the borrower’s capital structure than high yield bonds, he notes. Historically, he says, this has resulted in higher recoveries in default situations.

Interest Rate Risk Potentially Makes Shorter‑Duration Assets More Attractive

(Fig. 2) Yield versus interest rate risk (duration)

As of November 30, 2020.

Yields and duration are subject to change.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved; J.P. Morgan Chase & Co.; and Bloomberg Barclays (see Additional Disclosures). Index performance is for illustrative purposes only and is not indicative of any specific investment. Investors cannot invest directly in an index. Floating Rate Bank Loans = J.P. Morgan Leveraged Loan Index; Global High Yield Bonds = Bloomberg Barclays Global High Yield Index; Emerging Market Bonds (Local Currency) = J.P. Morgan GBI‑EM Global Diversified Composite Index; Emerging Market Bonds (USD) = J.P. Morgan EMBI Global Index; Global Ex‑U.S. IG Corporate Bonds = Bloomberg Barclays Global Corporate IG Index; U.S. IG Corporate Bonds = Bloomberg Barclays U.S. Investment Grade Corporate (300MM) Index; Global Aggregate Bonds = Bloomberg Barclays Global Aggregate Index; 10‑Year U.S. Treasury = U.S. Benchmark Bond–10 Yr; 10‑Year German Bund = Germany Benchmark Bond–10 Yr; 10‑Year Japanese Gov’t. Bond = Japan Benchmark Bond–10 Yr.

The floating rate feature of bank loans also gives them an extremely low duration profile—comparable to U.S. Treasury bills and other short‑term instruments—but with substantially higher yields, Giroux says. “Historically, floating rate loans have been the one fixed income sector that has tended to appreciate when interest rates are rising,” he argues.

Fixed income assets outside the U.S.—especially emerging markets corporate debt denominated in local currencies—also could hold opportunities for global bond investors in 2021, Vaselkiv says. A weaker U.S. dollar, he adds, could enhance that appeal by potentially boosting returns on nondollar assets for dollar‑based investors and potentially improving the creditworthiness of U.S. dollar bond issuers.

Key factors such as relative interest rates, relative growth rates, and relative monetary liquidity suggest that the trend toward U.S. dollar depreciation could continue in 2021, Vaselkiv argues. “Historically, U.S. dollar currency cycles have tended to last for significant amounts of time,” he says. “This potentially bodes well for international allocations—not just in fixed income, but also for equity names that generate a large portion of their earnings outside the U.S.”

Conclusions

For fixed income investors, 2021 could be challenging, as the falling yields and tightening credit spreads that boosted broad market returns in 2020 aren’t likely to play that role again. Rather, extended durations and the potential for a modest revival in inflation could make managing interest rate risk a portfolio priority, boosting the appeal of floating rate assets.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

January 2021 / INVESTMENT INSIGHTS