December 2020 / GLOBAL MARKET OUTLOOK

Asia ex-Japan: Constructive Outlook for Equities in 2021

High-quality growth businesses on reasonable multiples

Key Insights

- Asia in general managed the pandemic well in 2020. North Asian economies normalized fairly quickly. Others, like India, are lagging but show signs of improvement.

- Despite strong year‑to‑date performance, Asian markets offer an attractive risk/reward profile relative to their global counterparts from a valuation perspective.

- While there are pockets of expensive stocks such as biotech, internet platforms, and electric vehicles, many high‑quality growth businesses trade on reasonable multiples.

Our views remain constructive on the medium- to longer-term outlook for Asia ex‑Japan equities. Even as global growth may be slower to recover than earlier hoped for, we think domestic demand in the Asian region should hold up relatively well. In their responses to the coronavirus pandemic, governments have had to achieve a balance between adding the right level of stimulus and not adding too much or withdrawing too early. Although all countries saw deterioration in fiscal balances as they had to add some stimulus during 2020, the level of deterioration in Asia in general is more measured compared with some other parts of the world. In addition, due to falling imports and lower commodity prices, most Asia ex‑Japan governments have been able to keep their current account balances healthy. This should bode well for Asian FX from here, while periods of U.S. dollar weakness historically have been good for regional equity returns.

We are seeing signs of China starting to withdraw some liquidity, but we feel Beijing can continue to calibrate policy stimulus as needed in 2021. China’s policymakers are not out of ammunition, and there is room for them to do more should this become necessary. We maintain a cautious outlook on the frayed relations between the U.S. and China. This is expected to remain one of the key risks to Asia ex‑Japan markets in 2021. U.S./China relations will likely remain tense even under a Biden administration. Perhaps the areas of contention may shift, but we think U.S. national security concerns over technology are unlikely to go away.

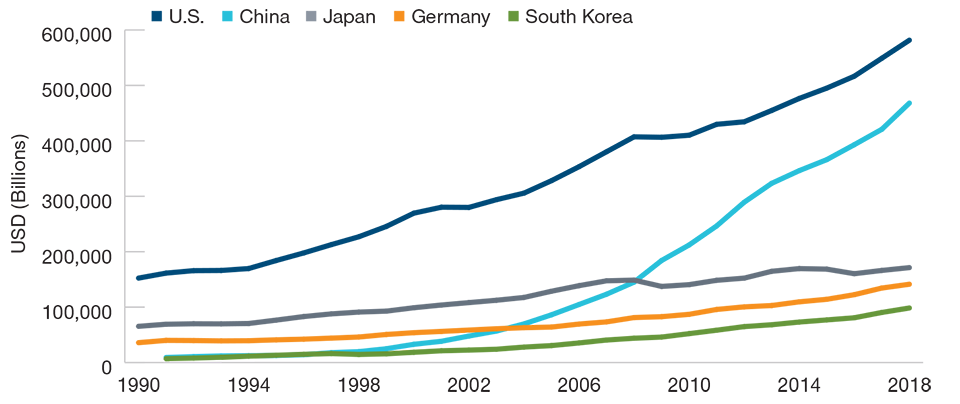

China’s Research and Development (R&D) Spending Has Been Growing Rapidly

(Fig. 1) Gross domestic expenditure on R&D (USD billions)

As of December 2018.

Source: OECD (2020), Gross domestic spending on R&D (indicator). doi: 10.1787/d8b068b4-en (Accessed on 27 November 2020).

We think the growth of intra‑regional trade will continue to rise over time. The recent Regional Comprehensive Economic Partnership (RCEP) trade agreement between the Association of Southeast Asian Nations (ASEAN) and five other Asia Pacific countries should further boost this in the medium to long term. While it is too early to quantify the potential impact of this deal on our investments, the direction is positive as we expect that the rise of intra‑regional trade will definitely increase efficiency and enhance economic growth.

Turning to companies, in general, Asian companies entered the pandemic in good shape from a balance sheet perspective. We can see that free cash flow for the region held up well despite the hit to earnings in 2020. We are seeing more investment opportunities in Asia with companies that are benefiting from increasing domestic demand due to import substitution. Consumption has generally held up well thanks to low household debt levels.

China to Continue to Lead Asian Economic Recovery in 2021

China’s economy has largely returned to normal—the only major economy to have done so. Domestic consumption and services are likely to drive growth next year, and the recent rebound in retail sales is encouraging. Potential positive growth spillovers in 2021 are likely to be increasingly felt by China’s Asian neighbors. Growth prospects among the emerging market economies still appear to be narrowly focused on China and northeast Asia.

The monetary and fiscal measures deployed by various governments in Asia to stem the impact of the outbreak should continue to be supportive in 2021. Even in the countries that have been affected the worst the number of cases is not obviously declining, but mortality rate for COVID‑19 (the disease caused by the coronavirus) has been low, which is partly attributable to the relatively young populations in India, Indonesia, and the Philippines. More importantly, people are starting to go back to normal life in places like India and ASEAN as governments loosen lockdowns and the extreme fear factor of the virus subsides with the prospect of vaccines becoming widely available in 2021.

Sticking With Our Bottom‑Up Investment Style

We believe that Asia ex‑Japan equity markets continue to offer opportunities to investors looking for reasonably valued, high‑quality growth companies that can successfully navigate this temporary period of uncertainty due to the coronavirus to eventually emerge stronger than before.

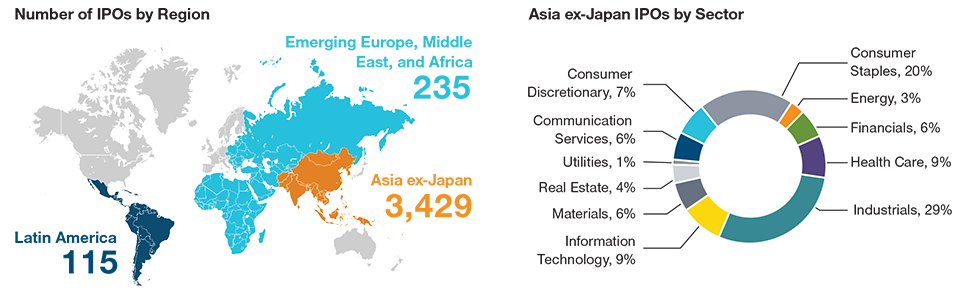

Asia’s Opportunity Set Is Large and Dynamic

(Fig. 2) Number of initial public offerings (IPOs) by region, December 2015 to December 2019

As of December 31, 2019.

Source: Financial data and analytics provider FactSet. Copyright 2020 FactSet. All Rights Reserved.

Across the region, we expect that the coronavirus outbreak may hasten consolidation in a number of industries, and we are focusing on companies that potentially stand to benefit from this acceleration. Domestic consumption remains an overarching theme in our portfolio. We believe that Asian households are generally under-levered and consumption is a secular opportunity.

We also favor potential beneficiaries of import substitution (especially in China) as domestic companies come up with ways to replace imports with local products, especially amid heightened geopolitical tensions. We find that the trade issue is prompting Chinese companies to source more products locally. Given the vulnerability of some parts of the global supply chain to external disruption revealed by the coronavirus, this trend is likely to continue.

Some of these domestic‑focused Chinese companies today could emerge as global players over time. In China, we look for companies that should benefit from the increasing demand for premium products, while across countries there may be opportunities in businesses that could benefit from consolidation in fragmented industries. When we think about our bottom‑up stock picks, we also look at the extent of a company’s innovation, not merely in the use of technology, but also in other ways as it seeks to improve market positioning.

Investment Opportunities in 2021

Stock markets generally have done well this year, but Asia ex‑Japan is still relatively better value versus other markets, in our view. There are pockets of very expensive stocks in Asia, such as biotech, some software names, some Chinese tech companies, and new energy vehicle theme stocks. But we believe there are also many high‑quality growth businesses still trading at reasonable multiples relative to their own history and relative to a lower cost of capital. This is the area where we naturally own the most stocks.

We also find good value in some of the cyclical stocks that were hit hard by COVID‑19 but which we think will emerge just as strong or even stronger after the pandemic. These tend to be companies that have suffered a short but sharp cyclical downturn thanks to the coronavirus. This is where we have been adding in recent months as we get closer to better testing capabilities, treatment, and, of course, a vaccine.

The Asia ex‑Japan region continues to be very dynamic, constantly offering us new opportunities to invest in. Our process favors companies that should come out of the crisis stronger. These tend to be companies that are leaders in their sectors and should be able to gain market share and consolidate their industries. We favor companies that are likely to benefit from a strong capital structure and are likely to weather a potentially prolonged downturn in business activity. While we recognize that the current environment presents a challenge to earnings forecasts, we expect to see healthier earnings growth reestablished in 2021 and beyond. It will remain key for governments to strike the right balance between adding stimulus without overstimulating or withdrawing too early. In terms of other risks in the region, we are of the view that U.S./China relations are unlikely to go back to the pre‑Trump era—despite some return to traditional diplomacy—with persisting tensions around technology.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.