March 2024 / GLOBAL EQUITIES

Global Earnings: Q4 Results Overview

What next for global equities

Overview

With the Q4 2023 earnings season largely behind us, I wanted to share some observations on what we have been seeing in markets and what it might imply for global equities in 2024. The key points are:

- The Q4 earnings season was generally better-than-expected in the U.S., while Europe continued to lag.

- In America, the Magnificent 7 mega cap names were a big driver of Q4 earnings.1 But there were signs of life outside of the top mega-cap stocks as well. We see earnings growth in the rest of the index playing catch-up or even overtaking the Magnificent 7 in the second half of 2024.

- Importantly, company commentaries suggest the U.S. economy and consumer both remain healthy.

- Stock selection among T. Rowe Price’s global equity strategies has again been positive, contributing to portfolio performance, with the majority of our holdings reporting beats on both the top and bottom line.

Q4 Corporate Earnings Highlights

U.S. (S&P500):

- 489 S&P500 constituents, or 98% of companies have reported so far (as of 29 February 2024).

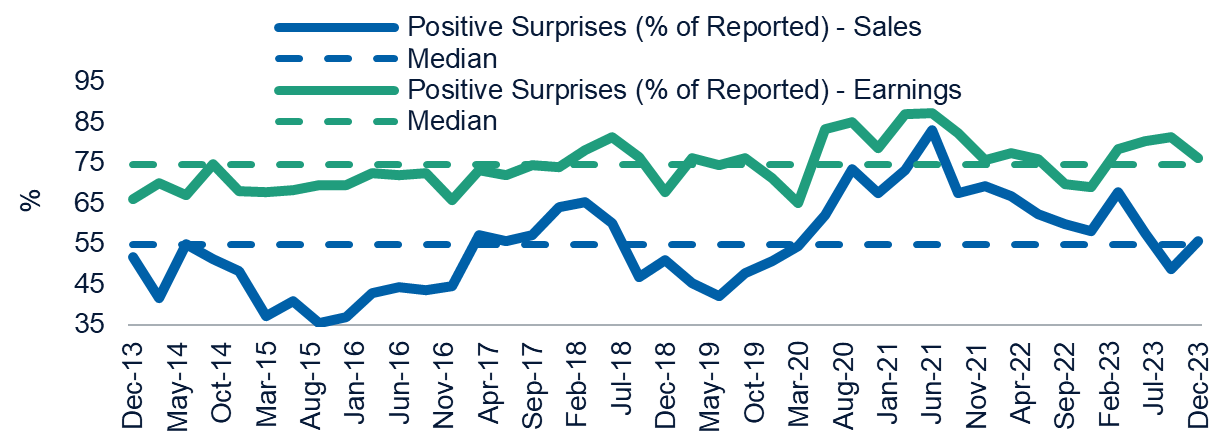

- Of those 56% have beaten on sales, and 76% on earnings, so we are continuing to see the positive benefits of operating leverage.

- Overall U.S. earnings growth is coming in around 8% plus, versus pre-season consensus expectations of 1.2%.

- Commodity sectors and Healthcare have been weak, and Discretionary, Technology and Communication Services have driven the bulk of the earnings growth in Q4.

- On a sequential basis, the number of companies beating estimates on sales has increased while those beating on earnings has declined somewhat from the third quarter, as can be seen in the chart below from JP Morgan:

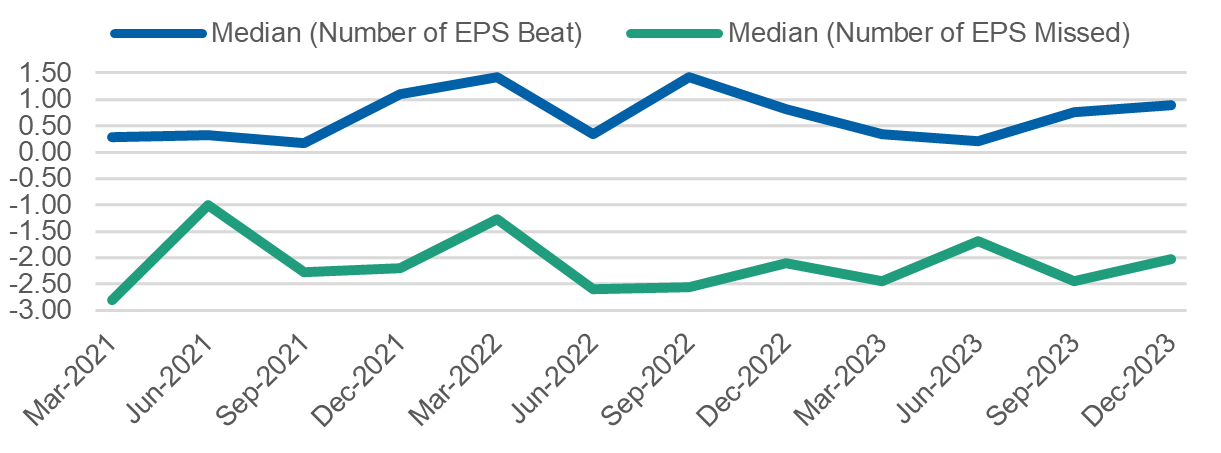

- On average, earnings misses by U.S. firms in Q4 were punished more than beats were rewarded. The median outperformance for beats was around 89 basis points while the median underperformance was about 200 basis points which is more than usual. One possible explanation for this wide divergence is that investors’ expectations were higher than those of sell-side research heading into earnings announcements.

Another decent quarter for U.S. corporate earnings

(Fig. 1) Percentage of S&P 500 companies beating

As of 29 February 2024.

Source: Bloomberg Finance LP. Please see Additional Disclosures page for more information about the S&P 500 Index.

U.S. earnings misses were punished in Q4

(Fig. 2) S&P 500: Median outperformance of earnings beats and misses

As of 29 February 2024.

Source: Bloomberg Finance LP. Please see Additional Disclosures page for more information about the S&P 500 Index.

Europe (MSCI Europe)2

- 87% of MSCI Europe companies have reported. Of those, only 32% have beaten on sales, with 38% having beaten on earnings.

- European earnings growth fell around 9%, in line with expectations. Q4 results were weighed down by energy & materials stocks, which fell around 30% year-on-year. Excluding those two sectors, Q4 earnings growth would be positive, around 2% to 3% year-on-year.

Companies’ Q4 commentaries/ Broad trends

- Big tech clearly continues to do well. We are seeing from them an acceleration in the public cloud, capex is trending higher, while managements have been cutting costs to boost the bottom line. Companies like Meta are showing their monetization levers as well as meaningful contributions from AI. A broad range of tech companies - from AMD to ServiceNow and Alphabet - are talking about seeing demand for AI- related products and services.

- Industrial companies like Caterpillar, United Rentals, Parker Hannifin etc. are seeing positive momentum. Orders and backlogs are strong, and we are seeing the ISM manufacturing gauge inflect positively. Companies are highlighting that supply-chain conditions are stable or easing.

- The U.S. consumer still appears to be healthy. We are seeing consumer confidence improving as gasoline goes lower, spending on leisure is still strong, credit card spending does not seem over the top, and the negative effect of inflation on real post-tax incomes is abating. While still tight, the labor market doesn’t seem to be a serious constraint and many managements have referenced conditions as being more balanced.

Impact of the ‘Magnificent 7’ versus other stocks

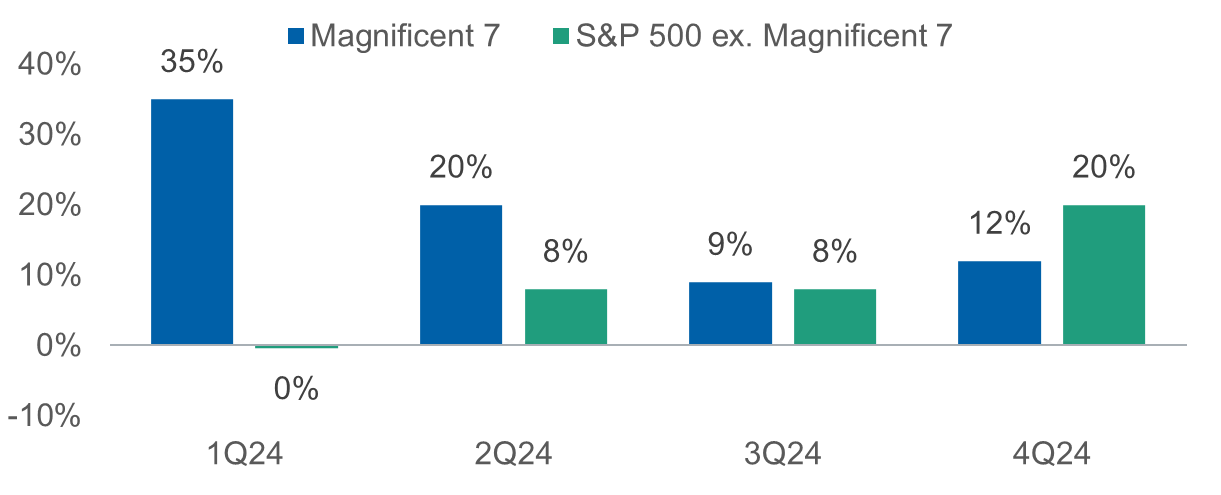

- While the Magnificent 7 were responsible for the bulk of S&P 500 earnings growth in Q4, earnings beats have nevertheless occurred on a broader base.

- The popular mega caps saw earnings growth tracking +60% in Q4 versus negative low single digits for the remaining 493 S&P constituents.

- Overall, the Magnificent 7 beat their earnings estimates by around 10% in Q4, which is slightly ahead of the rest of the market. The standouts here were Amazon and Nvidia. For Amazon, a recovery in retail margins along with resilience in AWS drove a strong beat at operating income level (~26%) in Q4, while Nvidia reported a strong beat for both sales and earnings of 8% and 12% respectively on already lofty expectations. (Source: Bloomberg Finance L.P.) Interestingly, stocks with USD100 billion or more in market cap also posted the same beat rate (7%) as other S&P 500 stocks.

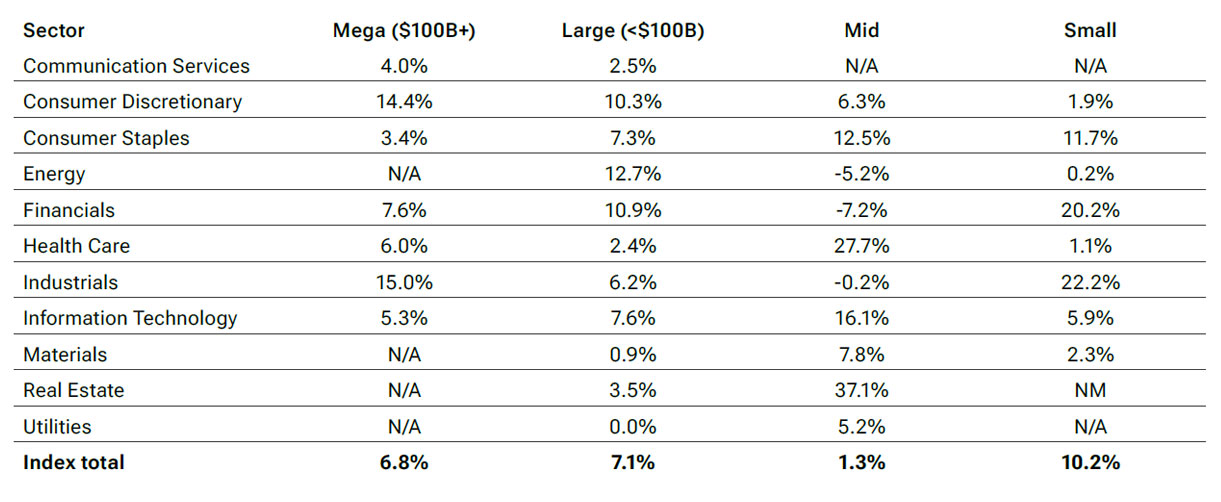

- The chart below from BofA below is quite interesting as it highlights that when looking at the US market, the largest beats have actually been coming from small cap stocks.

- When looking at consensus earnings expectations for the rest of the year, many analysts expect the growth rate of the “S&P 493” to catch up and overtake the Magnificent 7 in the fourth quarter of 2024.

U.S. Q4 earnings was not all about mega caps

(Fig. 3) Actuals vs. consensus from reported companies based on market cap

As of 12 February 2024.

Source: BofA US Equity & Quant Strategy.

Based on the S&P 500 for Mega and Large caps and Russell indices for Mid and Small.

U.S. earnings: a change in leadership expected later in 2024

(Fig. 4) Magnificent 7 vs. the other 493 quarterly EPS YoY

Source: BofA Global Research. As of 12 February 2024.

That suggests a reason for performance in the U.S. equity market to broaden out over the course of the year, providing more opportunities for stock pickers.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

March 2024 / INVESTMENT INSIGHTS

March 2024 / MULTI-ASSET INSIGHTS

Rahul Ghosh is a portfolio specialist in the Equity Division, representing the firm's global equity strategies to clients across the Asia ex Japan region. Rahul is a vice president of T. Rowe Price Singapore Private Ltd.