December 2023 / EMERGING MARKETS

Time to rethink traditional thinking in emerging markets

Time to rethink traditional thinking in emerging markets

Key Insights

- Some investors continue to view emerging markets as a purely short‑term, tactical allocation—offering potentially high returns, but at a cost of heightened risk and volatility.

- However, this traditional thinking fails to appreciate the broad diversity and nuance that exists between emerging market regions, countries, and companies.

- We consider some of the ongoing myths and misconceptions surrounding emerging equity and debt markets—and the investment opportunities that this presents.

The external environment affecting emerging markets (EM) has materially changed in recent years, with slowing global growth and tightening financial conditions creating a more challenging backdrop. For some, this only confirms the perception of EM as a purely short‑term, tactical allocation—offering potentially high returns, but at a cost of heightened risk and volatility. However, this traditional thinking no longer fairly represents today’s emerging markets, highlighting the need for a more granular approach to investing. While the global backdrop has become more challenging, it also serves to highlight the broad and differentiated nature of emerging markets, as fundamentally well‑anchored countries diverge from weaker counterparts. In this article, we address some of the ongoing myths and misconceptions surrounding emerging markets and the potential investment opportunities this presents for adept, active investors.

Emerging markets make up a significant part of the world. While definitions vary, the International Monetary Fund (IMF) currently classifies 162 countries as emerging or developing economies and 41 countries as advanced economies.1 This makes for a fertile investment landscape, offering wide variation in economic cycles, fundamental drivers, and market influences. The old view of EM as a tactical investment—best avoided during periods of global market or economic uncertainty—not only underappreciates the sheer scope of investment opportunities, it also fails to understand how significantly the EM universe has evolved in recent decades. Understanding the universe in detail, and the nuances that exist between countries, assumes even greater importance when one considers the still relatively scarce level of analyst coverage.

Emerging markets are the engine of the global economy

(Fig. 1) Yet they remain significantly underrepresented on world financial markets

As of April 2023.

Source: International Monetary Fund, World Economic Outlook Database.

Myth 1: Slowing global growth means avoid emerging markets

The playbook for investing in emerging markets has changed, with decisions no longer predominantly driven by the stage of the global economic cycle. Where once an expanding global economy, strong commodity prices, and moderate monetary conditions might have been seen as prerequisite conditions, the increasingly domestically driven nature of many EM economies means they are much less dependent on external factors. While these are still influential, they are part of a broader mosaic, alongside fundamental influences at country, sector, and stock‑specific levels. Today’s EM landscape, therefore, demands a more granular approach, and country‑by‑country expertise, as broad EM generalizations become increasingly tenuous. In addition to differences by country, EM offer a varied menu of assets to invest in, including hard currency sovereign and corporate debt and local currency debt, as well as deeper, more mature, equity markets.

The external environment has also materially changed in recent years, and the steep increase in developed market interest rates, particularly in the U.S., is set to persist for longer than initially anticipated. The impact of this policy tightening is being felt disproportionately across emerging debt markets, with a clear division opening up in the landscape. On one side is a group of countries, including Mexico and the larger economies in South America (e.g., Brazil, Chile, Peru, Colombia), that are underpinned by robust fundamentals. This group continues to be able to access credit markets, and spreads have remained reasonable and relatively stable.

On the other side is a set of fundamentally weaker EM countries that, as a result, are finding credit markets increasingly closed off to them. In the decade prior to the coronavirus pandemic, when global base interest rates were close to zero, many EM countries were able to access international capital markets for the first time, issuing new bonds at manageable spreads and with relatively low risk of default. Today, however, with base rates close to 5.5%, these countries are simply unable to issue new bonds at spreads that are sustainable. With no access to the market, they are struggling to refinance debt nearing maturity, and many have either defaulted already or are at risk of doing so.

Similarly, on the equity side, we are also seeing the EM universe split along fundamental lines, with three groups emerging, namely: (i) countries that continue to deliver solid growth rates (south/Southeast Asia and some parts of Africa), (ii) countries where growth is structurally slowing (north Asia), and (iii) countries where the picture remains mixed and a wide range of outcomes are being seen (Latin America and central Europe, the Middle East, and parts of Africa). Once again, through detailed research and a good understanding of regional and country‑specific dynamics, it is possible to find fundamentally good businesses at potentially distressed prices.

Myth 2: Emerging markets offer few defensive qualities

One of the biggest investor misconceptions is that EM are all about dynamic, growth‑oriented companies, while more defensive, value‑oriented opportunities are few and far between. Asset flows confirm this perception, with data showing that the bulk of all active money flowing into the EM equity universe is invested in growth/core strategies, while only a fraction of total flows is invested in value‑focused strategies. This huge bias means that a lot of value‑oriented opportunities, particularly in traditional “old economy” areas like manufacturing, are being overlooked or ignored. Consequently, there are many good businesses flying under the radar at potentially very depressed prices.

The current environment of increased global uncertainty only adds to the appeal of these value‑oriented EM companies, given the sensitivity of growth‑oriented investments to higher interest rates. Companies with relatively low‑risk profiles, reasonable price‑to‑earnings levels, and predictable earnings streams may not fit the traditional view of a “dynamic” EM investment, but these businesses exist. The beauty of these durable companies is that, over time, they can deliver significant compounded returns. They are unlikely to be among the very best EM performers in any single year, but when you look back over a 5‑ or 10‑year period, particularly when market uncertainty/volatility has been a feature, the value creation becomes evident.

Myth 3: The risk of error, from central banks or company management, is greater in emerging markets

Significant reform measures have been implemented in many EM countries, meaning that most are no longer just a few bad decisions away from a crisis. Detailed research is central in identifying those countries that are truly committed to consistent, market‑friendly policy direction while helping to avoid those that are moving in the wrong direction. Similarly, on the corporate side, great strides have been made in terms of improving governance and becoming more shareholder focused. Where once complicated governance structures, immature institutions, and unskilled management were common features of the EM corporate landscape, today these characteristics are much more the exception than the rule.

Even when sharp sell‑offs do occur in EM debt markets, we no longer fear that these events pose a systemic risk to the wider asset class. Over the past 25 years, when such periods have occurred, they have proved relatively short‑lived, creating opportunities to enter the market at potentially very depressed valuation levels.

On the equity side, evidence of stronger management discipline and better decision‑making is a key factor, suggesting a positive longer‑term outlook for EM equities. At a broad level, companies are generating more free cash flow, compared with previous decades, as management teams pay more attention to spending and other capital allocation decisions. In the current environment, selectivity will be key—identifying those countries with stronger, domestically driven economies and companies geared to the domestic economy where earnings growth and profit margins look sustainable or can potentially improve.

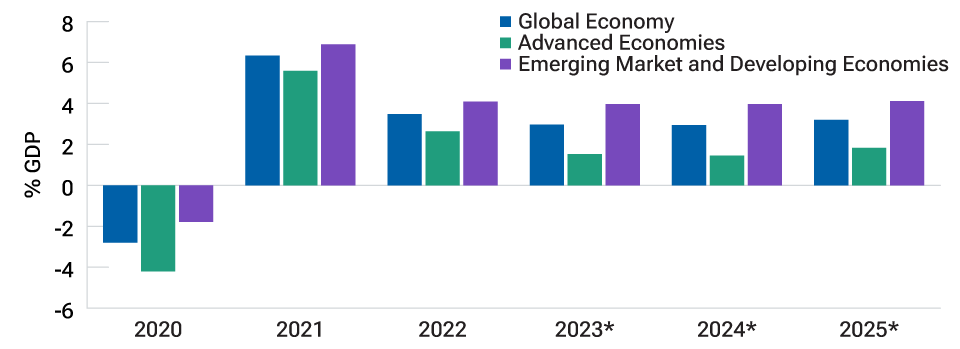

World economic outlook—October 2023

(Fig. 2) Annual growth projections

As of October 31, 2023.

*Estimated data. Actual outcomes may differ materially from estimates.

Source: International Monetary Fund, World Economic Outlook Database; data analysis by T. Rowe Price.

Myth 4: The growth potential of emerging markets will be more subdued going forward

The growth of EM debt as an asset class in recent years means that investors can access a much deeper, and more diverse, range of credit opportunities, spanning countries, financial and nonfinancial corporate issuers, and the full rating spectrum. While we recognize that market uncertainty and a mixed global economic outlook are important influences on the broad EM outlook, these need to be weighed against the strengths of individual domestic economies and the positive secular trends that continue to support long‑term optimism in EM generally. For example:

- Many EM countries continue to enjoy positive economic growth at rates well ahead of developed markets (Fig. 2). This is indicative of burgeoning economies that are less dependent on the developed world to prosper. Internal trade between EM economies has now surpassed external trade volumes with developed market economies, while a growing EM middle class is supportive of long‑term domestic demand.

- EM still have a lot of room to potentially improve productivity and catch up with developed market peers. Large, young, and increasingly educated workforces are central to closing this gap, along with the broadening adoption of technology. However, delivering on this potential is becoming increasingly differentiated, and it is more important than ever to have a good grasp of which countries are succeeding and which are at risk of stagnating.

Myth 5: ESG considerations significantly lag developed market peers

While environmental, social, and governance (ESG) investing has entered the mainstream in developed markets, there is an ongoing perception that less importance is attached to these factors in EM. However, EM companies have made great progress in improving their ESG credentials in recent years, with many businesses today displaying standards in line with global best practices. While some EM countries and companies are more progressed than others, the direction of travel is positive, with countless examples of companies including ESG factors as a core component of their long‑term business strategy.

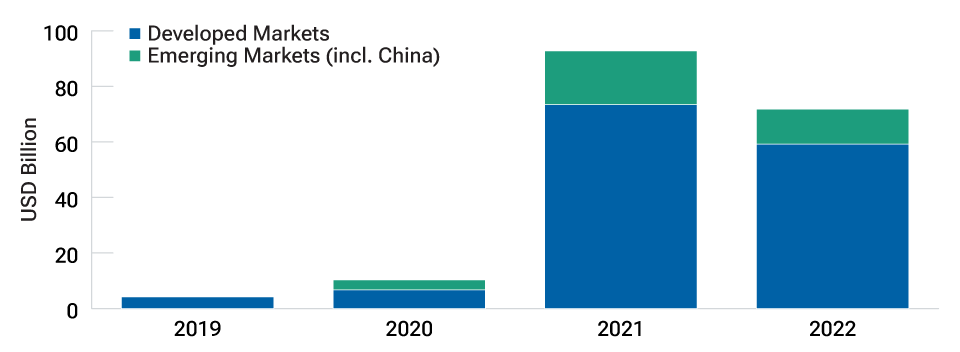

Issuance of sustainable bonds in EM has also noticeably increased in recent years, driven by robust issuance from some relatively new participants, including the Philippines, Mexico, Colombia, and Chile. This adds to the prominent issuance in more seasoned markets, like China (Fig. 3). While EM are still well behind advanced economy issuance, this is a trend we expect to continue as EM sovereigns increasingly look to finance their sustainable development goals.

Global sustainable bond issuance

(Fig. 3) Issuance of EM sustainable bonds is notably rising

As of December 31, 2022.

Source: Bloomberg Finance L.P., analysis by T. Rowe Price.

It is also worth highlighting the huge investment made by China in recent years in transitioning from fossil fuels to cleaner energy sources. China is now the world‘s largest producer of wind and solar energy and also the largest domestic and outbound investor in renewable energy. This seismic shift is creating knock‑on benefits for EM countries and companies geared to this transition, as well as having positive implications for energy security and affordability across the EM region.

While the slowdown in global demand poses a key near‑term challenge for EM, this kind of environment tends to create significant opportunities for informed, research‑driven investors as weak sentiment and traditional investor thinking heighten the potential for overselling. This is no single, homogenous entity, but rather a diverse universe of many countries, each at a different stage in its growth cycle, and with varying demographic and industry influences. In the near term, we anticipate stronger, domestically driven EM economies to perform best, as they detach from export‑oriented counterparts more directly impacted by slowing global growth. Longer term, EM remain a dynamic area of investment, offering superior growth potential relative to developed markets. The information asymmetry that exists in EM, and the predominance of passive investment flows, only adds to the potential for company mispricing in the vibrant, diverse, and highly nuanced EM universe.

Additional Disclosure

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Chris Kushlis is an emerging market sovereign analyst in the Fixed Income Division at T. Rowe Price. He is a vice president of T. Rowe Price Group, Inc. and T. Rowe Price International Ltd.

Mr. Kushlis has 15 years of investment experience, eight of which have been at T. Rowe Price. Prior to joining the firm in 2007, he was an advisor to the U.S. executive director at the International Monetary Fund.

Mr. Kushlis earned a B.A. from Middlebury College and an M.A. from the Johns Hopkins School of Advanced International Studies. He also has earned the Chartered Financial Analyst designation.