August 2023 / ASSET ALLOCATION

Leaning Into Real Assets

Attractive valuations and improving fundamentals may boost commodities.

Key Insights

- Although equities have rallied so far in 2023—supported by falling inflation and improving economic growth expectations in the U.S.—commodity prices have lagged.

- Our Asset Allocation Committee recently added to real assets equities, given attractive valuations for commodity-related assets and improving fundamentals.

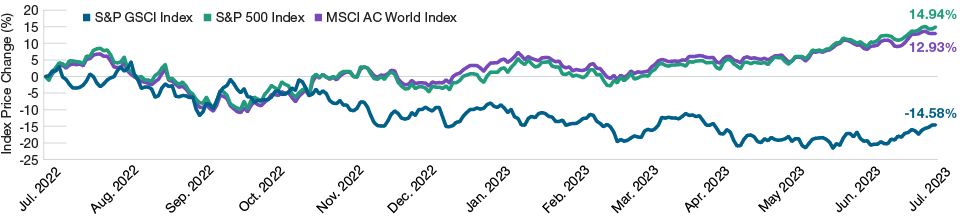

Since the beginning of this year, equity markets have advanced as inflation and economic growth expectations improved in the U.S. However, despite this uptick, commodity prices have been moving in the opposite direction (Figure 1).

Commodities, which are highly sensitive to global economic growth, have been weighed down by elevated recession risks, especially outside the U.S. Demand has also been muted due to considerable weakness in the Chinese property market and a surprisingly mild winter, particularly in Europe, which reduced the need for natural gas and oil. Meanwhile, the supply impact of Russia’s invasion of Ukraine has been more moderate than expected.

Commodities Left Behind

(Fig. 1) Stocks versus commodities.

July 25, 2022, through July 24, 2023.

Past performance is not a reliable indicator of future performance.

Sources: Bloomberg Finance L.P., S&P, and MSCI. See Additional Disclosures.

Energy Stock Valuations Are Attractive

(Fig. 2) Monthly valuation percentiles over the past 30 years.

July 30, 1993, through June 30, 2023.

Actual outcomes may differ materially from estimates. Valuation is calculated as next 12 months price-to-earnings (P/E) ratios.

Sources: Bloomberg Finance L.P. and S&P. See Additional Disclosures.

But these headwinds may be fading as energy sector fundamentals improve. China has recently signaled its intention to provide more support to its property market, and Russia’s decision to prevent grain exports through the Black Sea could be disruptive to some global economies. Valuations for commodity‑related equities have therefore become attractive (Figure 2).

Further, the number of active oil and gas rigs—a useful predictor of energy supply trends—has been decreasing at an accelerated pace since February, an indication that energy supply levels may be peaking. With this backdrop, the commodities sector is likely to benefit amid strong demand and limited supply.

Inflation could also boost commodity‑related equities. Although inflation seems to be moderating in the near term, there are concerns that prices could rebound and surge higher, as they did during the early 1980s when the Federal Reserve eased restrictive monetary policy prematurely. As a result, our Asset Allocation Committee recently increased its allocation to real assets, which include a large allocation to commodity‑related equities.

Additional Disclosures

MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such

The S&P Indices are products of S&P Dow Jones Indices LLC, a division of S&P Global, or its affiliates (“SPDJI”) and has been licensed for use by T. Rowe Price. Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC, a division of S&P Global (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); T. Rowe Price’s Products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P Indices.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

August 2023 / GLOBAL FIXED INCOME

Tim Murray is a capital market strategist in the Multi-Asset Division. Tim is a vice president of T. Rowe Price Associates, Inc.