August 2023 / ESG

2023 Proxy Voting Summary

Key trends in T. Rowe Price’s proxy voting activity over the past year.

Executive Summary

In this report, we summarize the T. Rowe Price Associates (TRPA) proxy voting record for the 12-month reporting period ended June 30, 2023. Our goal is to highlight some of the critical issues in corporate governance during the period and offer insights into how we approach voting decisions in these important areas. This report is not an all‑inclusive list of each proxy voted during the year but, instead, a summary of the year’s most important themes.

Thoughtful Decisions Leading to Value Creation

At T. Rowe Price Associates, proxy voting is an integral part of our investment process and a critical component of the stewardship activities we carry out on behalf of our clients. When considering our votes, we support actions we believe will enhance the value of the companies in which we invest, and we oppose actions or policies that we see as contrary to shareholders’ interests. We analyze proxy voting issues using a company‑specific approach based on our investment process. Therefore, we do not shift responsibility for our voting decisions to outside parties, and our voting guidelines allow ample flexibility to account for regional differences in practice and company‑specific circumstances.

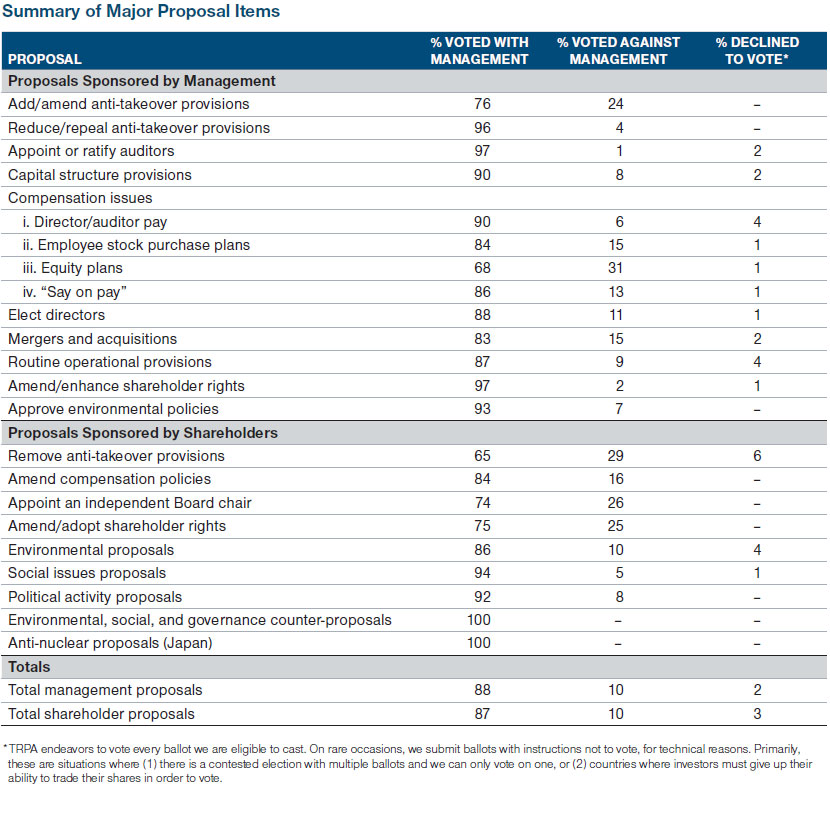

The following table is a broad summary of some of our proxy voting patterns and results for the reporting period covering July 1, 2022, through June 30, 2023, across our global equity-focused portfolios.

Themes From Vote Results

The categories above represent a subset of our total voting activity during the reporting period, but these are the most prevalent and significant voting issues. In the following section, we discuss some of these categories in detail.

In this voting period, we have identified two distinct but related trends that stand out. The first is a continuing decline in our overall support levels for shareholder proposals of an environmental or social nature. The second is a broadening out of our voting guidelines to reflect the different needs of our investing clients who choose investment mandates emphasizing not only financial returns but also environmental or social impact.

Social, Environmental, and Political Proposals

While shareholder resolutions can be an effective means of instigating change under certain circumstances, in most cases we find that direct engagement and the election of directors are more targeted ways for investors to express reservations over a Board’s oversight of strategic, financial, human capital, environmental, or other issues related to the company’s performance.

Over the past two years, issues such as racial justice, income inequality, worker safety, and climate change had been on prominent display within the corporate sector due to a confluence of events, including the coronavirus pandemic. Shareholder resolutions addressing such issues received notably higher‑than‑average support in 2021 from certain investors and higher visibility when compared with previous years, although these support levels began to subside in 2022.

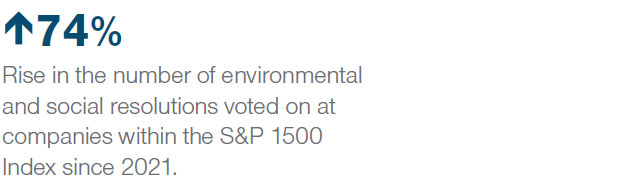

In this most recent proxy voting season, investor support for such resolutions was relatively low. There are multiple reasons for this outcome. It began when the U.S. Securities and Exchange Commission (SEC) decided to allow more proposals across a wider range of environmental and social topics to move forward. Since that time, the number of environmental and social resolutions voted on at companies within the S&P 1500 Index rose 74%, from 170 in the 2021 season to 296 this year.

The traction that so many of these resolutions gained in 2021 seemed to not only attract a new set of proponents in the subsequent two years but also inspired experienced proponents to expand their topics of advocacy. Our observation is that the increase in the volume of proposals resulted in a decrease in their overall quality. We observed more inaccuracies in proposals, more poorly targeted resolutions, and more proposals addressing non‑core issues. In addition, we observed a marked increase in the level of prescriptive requests. Proponents moved swiftly from disclosure‑based requests seeking additional reporting on environmental, social, and governance (ESG) matters to action‑based requests seeking specific commitments, capital investments, or structural changes from the targeted companies.

Our view on these prescriptive proposals is that they usurp management’s responsibility to make operational decisions and the Board’s responsibility to guide and oversee such decisions. Our overarching framework for determining how to vote on these proposals uses an economically centered, returns-focused lens. We do not believe it is consistent with our fiduciary duties to support proposals that, intentionally or not, are designed to impose burdensome requirements on the corporation that have no clear path to long-term value creation.

Amid this activity by shareholders, changes in the geopolitical landscape prompted investors and issuers to widen the scope of previous discussions around the shape an energy transition may take and the importance of energy security.

Another important development over the past three years is the pace at which issuers have collected and disclosed decision-relevant data on environmental and social considerations. When a company’s ESG disclosures are comprehensive and quantitative enough to meet our needs as investors, we are less inclined to support shareholder resolutions seeking additional reporting.

Finally, there was a marked increase this year in activity by advocacy groups known to be critical of using ESG considerations in corporate decision-making. Previously, these ESG counter-resolutions were rare, but so far in 2023 we have voted on dozens of them across our portfolios.

Expanded Voting Guidelines

The second significant development over the past year is our expansion of our proxy voting guidelines to accommodate investment strategies with objectives other than purely financial returns. These specialized strategies are labeled according to their mandates, such as impact or net zero portfolios. Clients in such strategies have made a choice to balance financial returns alongside other goals, such as specific social or environmental indicators.

Because these strategies’ objectives are different from our regular, returns-focused portfolios, it stands to reason that their proxy voting framework should be different as well. The T. Rowe Price Associates ESG Investing Committee approved separate voting guidelines for these investments. This is the first year that both the impact and net zero voting guidelines were implemented and reported separately.

Most of the voting guidelines for these strategies are aligned with our long-standing views on governance and accountability. However, they tend to support more shareholder resolutions of an environmental and political nature than the rest of our portfolios. This is because the clients in these strategies have explicitly chosen to balance financial with social or environmental objectives. For these investors, it is appropriate to ask companies to take additional measures toward the disclosure, management, and mitigation of ESG risks, even if we believe these may impact financial returns.

As a group, the T. Rowe Price impact and net zero strategies supported 70% of shareholder-sponsored resolutions in the environmental category. They supported 6% of resolutions of a social nature. They supported 67% of resolutions seeking additional disclosure on political spending or lobbying.

The reason for the level of social support by the impact and net zero strategies being lower than in the other two areas is twofold. First, it reflects the fact that social topic shareholder resolutions were not generally related to a net zero mandate. Second, there were a very small number of social topic shareholder resolutions at companies held in impact strategies. In a number of cases, upon reviewing the resolution, the portfolio managers of these strategies opted to engage on the topic rather than support the resolutions, given company‑specific circumstances. While voting is one stewardship tool, it is not the only one. The measured approach taken by these strategies this year may change in the future if proponents focus on more material concerns that remain unaddressed by the companies in these portfolios.

2023 Voting Outcomes

Global Voting Themes

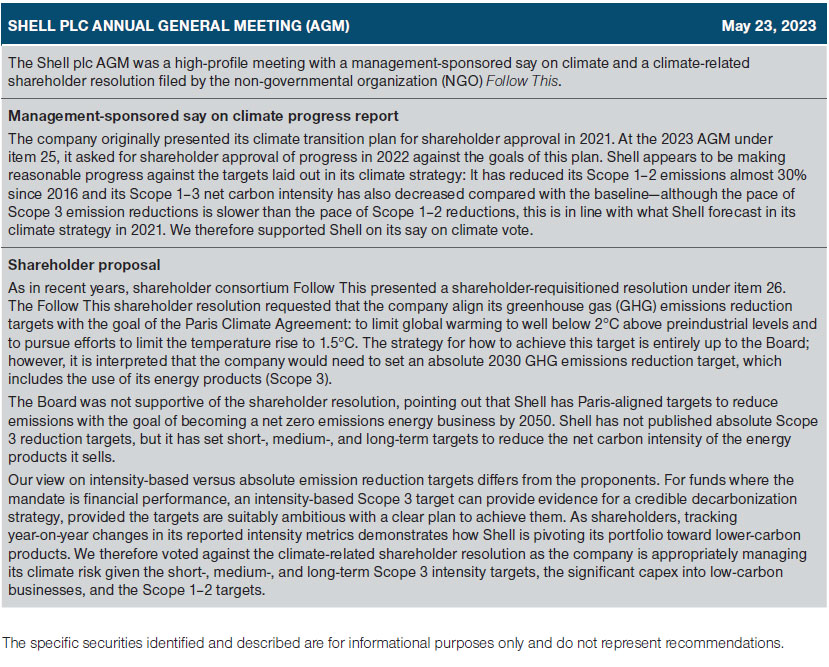

Outside the U.S., another significant development is affecting voting patterns, particularly in Europe, the Middle East, and Africa (EMEA) and Australia. In these markets, there is a growing embrace of voluntary, management-sponsored climat resolutions, or so-called say on climate votes. The purpose of these votes is for the company to present the details of its medium- and long-term climate strategy and reporting to investors for their endorsement. In markets where the say on climate voting concept has not gained traction, the spotlight remains on a small number of high-profile environmental resolutions brought by shareholders. In markets where the say on climate concept is more prevalent, we observe a more naunced dynamic where the management-sponsored resolution may compete with a proponent's request for additional disclosure, as in the example below.

In this reporting period, there were 30 say on climate votes across all TRPA global equity-focused portfolios. As the table shows, we supported 93% of them.

In Japan, notable developments include a growing use of shareholder resolutions targeting environmental disclosure and actions, progress on female Board representation, and a growing level of investor activism.

A Decline in Support for Social, Environmental, and Political Proposals

We supported the recommendations of corporate Boards on environmentally oriented shareholder proposals in 86% of cases this year. That compares with 84% last year.

We sided with Board recommendations 94% of the time on socially focused resolutions this year, up from 87% last year. Similarly, we agreed with Boards 92% of the time on resolutions addressing corporate lobbying and political spending, compared with 70% in 2022.

These figures do not include two unique subcategories of shareholder resolutions, which we have identified as separate line items in the table. These are ESG counter‑proposals, and a set of resolutions aimed at persuading Japanese electric utility companies to discontinue the use of nuclear power. In our analysis, we separate these two categories because they represent the appropriation of the shareholder resolution process to address a narrow and non-economically based agenda.

Across the markets where shareholder-sponsored resolutions are permitted, average support levels for environmental and social proposals fell substantially in 2023. We conclude that other institutional investors shared our concerns about the quality of the resolutions put forth this year.

T. Rowe Price Associates publishes a detailed analysis of our votes on environmental and social shareholder proposals in the first quarter of each year. This paper, “For or Against: The Year in Shareholder Resolutions,” can be found on our website.

Election of Directors

We recognize that it is the Board of Directors’ responsibility to develop and guide corporate strategy and oversee management’s implementation of that strategy. We generally do not support shareholder‑led initiatives that we believe may infringe upon the Board’s authority. However, one of the fundamental principles underlying our proxy voting guidelines is accountability. Directors are the designated representatives of shareholders’ interests. Therefore, our voting reflects our assessment of how effectively they fulfill that duty.

Examples of how we apply this principle in our proxy voting decisions include:

- U.S. market—We generally oppose the reelection of non‑executive directors at companies that have been publicly traded issuers for more than 10 years yet still maintain protective mechanisms more appropriate for early‑stage companies. Such mechanisms insulate directors from accountability.

- Global—We generally oppose the reelection of directors at companies where we have identified serious, material environmental or social risks but the Board still does not provide sufficient evidence that it is addressing the issue. Companies in sectors with significant exposure to climate risk, for example, should be disclosing their annual direct greenhouse gas emissions totals, at a minimum.

- Global—We have identified a set of companies with serious, ongoing, and unmitigated ESG controversies beyond climate risk. Such controversies include incidents of fraud, large‑scale industrial accidents, findings of widespread harassment or discrimination, and other incidents raising concerns about systemic mismanagement of key risks at the company. We oppose the reelection of directors at companies in these categories.

- Global—We oppose the reelection of individual directors who have exhibited egregious failures to represent investors’ interests in specific situations.

- Regional—We maintain a regionally determined expectation of Board diversity across the markets where we hold investments. Generally, we oppose the reelection of key Board members in cases where the Board still comprises members of a single gender and where the Board’s overall diversity does not meet its widely adopted local market standard.

- Global—Other situations where we believe shareholders are best served by voting to remove directors include failing to remove a fellow director who received less than a majority of shareholder support in the prior year, neglecting to adopt a shareholder‑proposed policy that was approved by a majority vote in the prior year, adopting takeover defenses or bylaw changes that we believe put shareholders’ interests at risk, maintaining significant outside business or family connections to the company while serving in key leadership positions on the Board, promoting the decoupling of economic interests and voting rights in a company through the use of dual‑class stock without adopting a reasonable sunset mechanism, failing to consistently attend scheduled Board or committee meetings, and implementing a policy or practice that we believe is a breach of basic standards of good corporate governance.

The election of directors is the single largest category of our voting activity each year, representing 48% of our total voting decisions this period. In 2023, we supported 88% of director elections globally, compared with 89% last year.

Our expectation is that TRPA will continue to prioritize Board accountability as the best mechanism to provide feedback to corporate issuers on a variety of issues, including ESG concerns. Select shareholder resolutions serve as a secondary mechanism, to the extent that they are well crafted and aligned with the economic interests of long‑term investors.

Executive Compensation

Annual advisory votes on executive compensation—the nonbinding resolutions known as “say on pay”—are a common practice globally. As a result, executive compensation decisions remain a central point of focus for the dialogue that routinely takes place between companies and their shareholders. In our view, corporate disclosure in the annual proxy filings improves every year as Board members endeavor to explain not only what they paid their executive teams but also why.

In the UK, we have found companies to be particularly sensitive to the cost-of-living crisis, with many making one‑time payments to the broader workforce during the year. The fairness section in our proxy voting guidelines was introduced during the coronavirus pandemic and has been applied in the UK market during the 2023 AGM season. The following case study provides an illustration.

In the past year, we voted against the compensation vote at 13% of companies. Generally speaking, we are most likely to express concerns about a compensation program when we have observed a persistent gap between the performance of the business and executive compensation over a multiyear period. Other common reasons for our opposition to these resolutions are situations where (1) the Board uses special retention grants without sufficient justification and (2) the use of equity for compensation is high but executives’ ownership of the stock remains low.

Broad‑Based Equity Compensation Plans

We believe a company’s incentive programs for executives, employees, and directors should be aligned with the long‑term interests of shareholders. Under the right conditions, we believe equity‑based compensation plans can be an effective way to create that alignment. Ideally, we look for plans that provide incentives consistent with the company’s stated strategic objectives. This year, we supported the adoption or amendment of such compensation plans approximately 68% of the time.

For the compensation plans we did not support, our vote was usually driven by the presence of a practice that we felt undermined the link between executive pay and the company’s performance, such as:

- compensation plans that, in our view, provide disproportionate awards to a few senior executives

- plans that have the potential to excessively dilute existing shareholders’ stakes

- plans with auto‑renewing “evergreen” provisions

- equity plans that give Boards the ability to reprice or exchange awards without shareholder approval

Mergers and Acquisitions

We generally vote in favor of mergers and acquisitions after carefully considering whether our clients would receive adequate compensation in exchange for their shares. In considering any merger or acquisition, we assess the value of our holdings in a long‑term context and vote against transactions that, in our view, underestimate the true underlying value of our investment. In this reporting period, T. Rowe Price Associates opposed 15% of voting items related to mergers and acquisitions.

Takeover Defenses

We consistently vote to reduce or remove anti‑takeover devices in our portfolio companies. We oppose the introduction of shareholder rights plans (so‑called poison pills) because they can prevent an enterprise from realizing its full market value and create a conflict of interest between directors and the shareholders they represent. We routinely vote against directors who adopt poison pill defenses without subjecting them to shareholder approval.

A positive development over the past several years has been a trend of companies dismantling their long‑standing antitakeover provisions at the urging of their shareholders. When such provisions are embedded in the company’s charter, a shareholder vote is required in order to remove them. We enthusiastically support management efforts to remove takeover defenses.

Conclusion

Company‑specific voting records are made available on our website each year on or around August 31, reflecting a reporting period of July 1 of the preceding year to June 30 of the current year. This report serves as a complement to these detailed voting records, highlighting the key themes that emerge from our voting decisions. In addition to this report, we provide an overview of our voting activity each year in our ESG Annual Report.

For more information, visit troweprice.com/esg.

A Note About Our New Corporate Structure

On November 19, 2020, T. Rowe Price announced plans to establish T. Rowe Price Investment Management, Inc. (TRPIM), a separate, U.S.-based, SEC-registered investment adviser. TRPIM jas a distinct investment platform with independent research and stewardship teams. TRPIM makes proxy voting decisions separately from other parts of T. Rowe Price. The separation of TRPIM's investment platform became effective July 1, 2022.

Due to the separation, the proxy voting figures used in our 2022 Proxy Voting Summary Report are not comparable to those in our 2023 reports, which cover each entity separately.

The 2023 Proxy Voting Summary Report for TRPIM will be available at troweprice.com/esg.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Donna Anderson is the global head of Corporate Governance. Donna leads the firm’s proxy voting and engagement efforts and serves as a specialist for incorporating governance considerations into the firm’s investment research process. She is cochair of the ESG Committee , a member of the Valuation Committee, and a director of the T. Rowe Price Trust Company. She is a vice president of T. Rowe Price Group, Inc.

Jocelyn Brown is the head of Governance, EMEA and APAC, for T. Rowe Price International Ltd. She is a member of the ESG Committee. Jocelyn is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.