June 2023 / INVESTMENT INSIGHTS

2023 China Midyear Market Outlook

A more broad-based recovery after initial reopening, though some bumpiness is expected.

Key Insights

- Despite some softer macro data recently, the initial stage of economic reopening largely met our expectations, with the services sector leading the way.

- We expect the recovery to broaden with some bumpiness due to the volatile base, uncertainties in the external economy, and geopolitical tensions.

- The regulatory environment should normalize, with more support for the private sector. Valuations are attractive versus growth for China equities.

China’s economic reopening has largely played out as we had expected in December 2022. Initially, there were a string of positive economic surprises that boosted investor confidence. China’s first‑quarter gross domestic product (GDP) growth number, for example, came in at 4.5%, much better than the consensus forecast of 4%. The consumption rebound was also strong, led by strong services sector recovery.

- Travel-related consumption services rebounded very strongly.

- Catering notched above 20% growth in March and overall around 14% in the first quarter.

- Industrial production was a little weak as were exports prior to the rebound in March, but both were within expectations.

Residential property remains a key uncertainty after the sharp contraction last year. The property market in the first quarter appears bifurcated. We have seen a healthy rebound in higher-tier cities where policy restrictions on home purchases at the city level have eased. Sales numbers in lower-tier provincial cities remained weak, however, which may be partly due to net migration to larger cities. Property sales by value rose 4.1% in the first quarter, while new home prices increased for a third consecutive month in March. First-quarter national new home starts remained in contraction territory, though the magnitude narrowed.

Outlook for the Second Half of 2023: Recent Softness in Macro Data Unlikely to Derail 2023 Economic Recovery Trajectory

We believe the recent weakness in China’s macro data is more likely to be a temporary hiccup than a major trend that could derail 2023’s recovery trajectory. We anticipate a gradual but more broad‑based economic recovery for the rest of the year and into 2024, with some bumpiness expected due to the volatile base, uncertainties in the external economy, and geopolitical tensions. In such an environment, stock picking is our focus in navigating the uncertainties.

Annual growth rates for retail sales, fixed investment, and industrial output surged in April, but this was due to the base effects arising from Shanghai’s lockdown in April 2022. Base effects are likely to distort year-on-year data comparisons throughout 2023, adding considerable “noise” to the monthly data releases. Four-year compound annual growth rates show that the Chinese economy lost some momentum after the first phase of reopening ended.

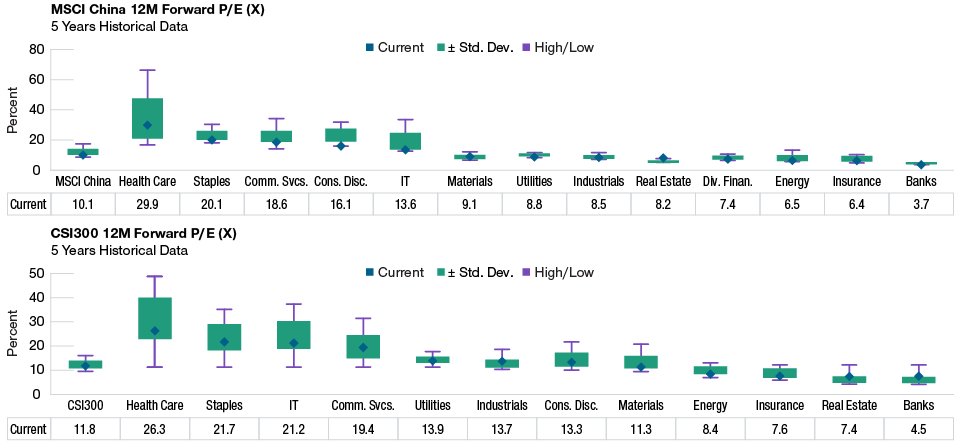

Following softer economic data in April, investors have recently become concerned about the sustainability of economic recovery. As a result, the rally in Chinese stocks that began last October has stalled recently, leaving the market at attractive valuations, especially in sectors such as communication services and information technology (IT) (Figure 1).

We believe the initial phase of China’s reopening—benefiting consumer services in areas such as travel, entertainment, hotels, and restaurants—has largely played out. However, the economic recovery should have legs. Because of the pandemic, it is estimated that the services sector failed to create as many as 30 million jobs cumulatively in the past three years (source: Morgan Stanley Research). As “experience” types of consumption recovered in the first phase, we expect employment in these areas to improve and the recovery to broaden out in the second phase to include job recruitment agencies and the broader consumer space, including goods consumption. Later in 2023 or early in 2024 we should see the third recovery phase begin as late‑cycle themes start to gain traction with improved business confidence, such as advertising companies and private investment.

China Valuations Are Attractive

(Fig. 1) 12-month forward price/earnings ratio. Five years historical data.

As of April 30, 2023.

Sources: FactSet, I/B/E/S, MSCI, Wind, Goldman Sachs Global Investment Research. Financial data and analytics provider FactSet: Copyright 2023 FactSet. All rights reserved. Please see Additional Disclosures page for information about this MSCI information.

Earnings Forecast: China Versus Rest of the World

(Fig. 2) Annual EPS growth forecasts (%) for 2023 and 2024

As of April 30, 2023. There is no guarantee that any forecasts made will come to pass. Actual results may vary.

EPS = earnings per share. ACWI = MSCI All Country World Index; U.S. = S&P 500 Index; China = MSCI China Index.

Sources: MSCI, S&P, Goldman Sachs Global Investment Research. Please see Additional Disclosures page for information about this MSCI & S&P information.

Given the recent softness in macro data, the possibility of selective fiscal measures to support growth is increasing, although it is difficult to forecast their timing and magnitude. Monetary policy in China should remain supportive throughout 2023. The People’s Bank of China (PBoC) cut its reserve requirement ratio for banks in March. Credit growth, like other economic data, showed some volatility in recent months, and most China economists now expect one or more interest rate cuts this year. This may be facilitated if the Federal Reserve is currently close to peak monetary tightening in the U.S. In addition, should there be external demand uncertainty to weaken China’s export growth, we believe regulators have fiscal tools or easing housing policies, such as second-home restrictions, to support better growth.

Overall, the government’s full-year GDP growth target of “around 5%” is not demanding. We think the volatile base will lead to bumpiness in monthly macro data, but the recovery trajectory is unlikely to be derailed.

Consensus earnings forecasts for the MSCI China Index in 2023 showed an initial upward revision after reopening, which has since been trending down. A key factor is that the impact of the COVID-19 outbreak in the fourth quarter of 2022 and early in 2023 has made near-term forecasting difficult. Following the wave of COVID-19 cases in January, around half of Chinese companies missed their earnings expectations in the first quarter of 2023. We expect this to turn around in the coming months as the second and third legs of the recovery play out. As Chinese companies emerge from 2022’s negative impact from COVID lockdowns and weakness in residential property, they may reveal more confidence about demand recovery (Figure 2).

More Support for the Private Sector

A feature of the new leadership since the National People’s Congress (NPC) in March has been the stream of government statements supporting the private sector. After the regulatory crackdowns in 2021 and last year, many foreign investors remain unconvinced. Investors may also have been disappointed by no big fiscal stimulus measures since the NPC. The government’s economic policy changes in 2023 have until now been more micro than macro in nature. What is important to us, however, is that we find Premier Li Qiang to be pro-business. Under him, we expect a greater degree of policy consistency over the next couple of years. We look for more stabilization‑type policies to reassure the private sector and boost business confidence.

Anecdotally, Alibaba’s proposed restructuring into six business units shows that China’s private sector companies may sense more freedom for self-help and flexibility in the current environment. In addition, online game approval is normalizing, and recently some of the foreign game titles were also approved. These positive signals will likely bring more vibrant energy and innovation to the private sector, a contrarian view we take that stands in contrast to the negativity commonly encountered.

As another example, China recently released a regulatory policy for artificial intelligence (AI) companies. Some commentators viewed this negatively given that it came so quickly when the AI industry was in its early stages. But we view the government as learning from the past. Historically, Beijing often let new industries grow in size for a number of years before bringing in government regulations. This risked creating negative investor sentiment as the businesses involved were already big and the impact of the new regulations was uncertain. This time, Beijing has stepped in early to guide the industry and to provide regulatory direction. This should help companies to adjust their products and business models at an early stage in order to comply with the new regulations.

Easing Geopolitical Tensions

China remains an essential part of the global economy. Despite the potential decoupling in select high-tech areas, such as leading-edge semiconductors and biotech, we believe that China can be a key contributing factor to counter global inflation.

The Chinese government has shown its willingness to cooperate with the U.S., as evidenced by the solution reached on audit inspections of U.S.-listed Chinese companies. The resumption of high-level talks between the U.S. and Chinese governments and the more constructive comments on China in the recent G-7 Summit Statement suggest that geopolitical tensions are easing.

We see the strategic competition between China and the U.S. as structural. The two countries and the rest of the world are adjusting to the new environment and will have to find a balance. During this process, we as investors must focus on finding areas that are unlikely to be adversely impacted by policy change or that stand to benefit from the reshaping of supply chains.

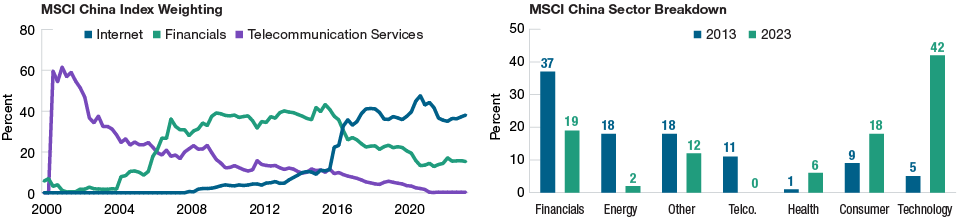

China’s Rapidly Evolving Equity Market Structure

(Fig. 3) Consumer, health care, and technology have grown in importance; financials, energy, and telecoms have shrunk

As of April 30, 2023.

Technology: information technology, media and entertainment, and internet and direct marketing retail. Consumer: consumer staples and consumer discretionary ex internet and direct marketing retail. Financials: financials and real estate. Telecom Services (Telco.): communication services ex media and entertainment. Other: industrials, utilities, and materials.

T. Rowe Price uses the current MSCI/S&P Global Industry Classification Standard (GICS) for sector and industry reporting.

Please see Additional Disclosures page for information about this MSCI and this Global Industry Classification Standard (GICS) information.

Sources: Bloomberg Finance L.P. FactSet., Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

Investment Opportunities

The structure of China’s equity market has evolved dramatically over the past two decades, and we expect this to continue (Figure 3). Dynamic industry and sector trends are the norm for China. Investors therefore need to anticipate each key trend if they are to stay ahead of the game. Figure 3 shows that since 2013 the consumer, health care, and technology sectors have grown significantly in importance, while financials, energy, and telecoms have all shrunk.

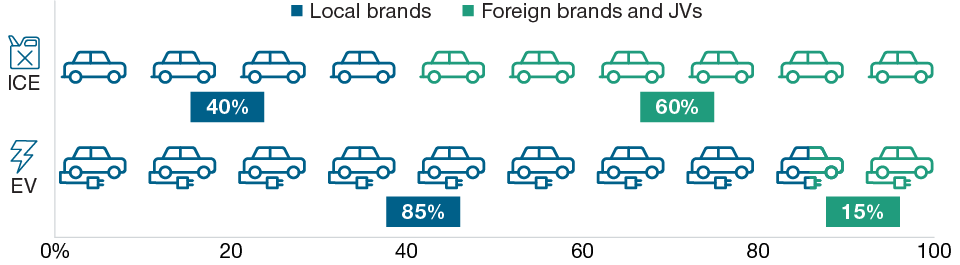

For a good example, consider how rapidly electric vehicles (EVs) are currently disrupting China’s auto industry. Our industry analysts attended the Shanghai Auto Show in April and confirmed our belief that EVs have become the mainstream in the Chinese auto industry. Out of over 100 new models launched during the show, more than 70% were EVs, heavily outnumbering traditional internal combustion engine (ICE) vehicles. Local brands continue to lead the way, with over 80% market share in the EV market (Figure 4).

The EV ecosystem can offer exciting investment opportunities in many areas, including Chinese companies with leading-edge technology in powertrains, fast charging, autonomous driving, auto component supply chains, and industrial equipment manufacture, particularly those that benefit from volume growth and content gain stories. China is not only the largest EV market in the world, it has also become the largest auto exporter globally. In the first quarter of 2023 alone, over 800,000 units were shipped, driven by demand from emerging markets. Under such rapid industry disruption, we believe that stock selection will be crucial in pursuing the future beneficiaries in this space.

We continue to find interesting investment ideas in the domestically listed A-share space, especially in industrial areas where we find structural market share gainers with strong product offerings. Since 2018, several factors have happened simultaneously that structurally drove the domestic players gaining more market share, the combined power of which is likely to be underappreciated by the market. These factors include:

- an accelerated pace of domestic substitution since the 2018 trade war with the U.S.

- the EV and renewable energy trends have accelerated since 2020, driving demand growth for key industrial components

- COVID-related supply chain disruption to foreign suppliers provided an opportunity for Chinese players to enter the market

In EV, Local Brands Dominate China’s Auto Market

(Fig. 4) Share of local makers versus foreign and joint venture (JV) brands

As of April 30, 2023.

ICE = internal combustion engine; ICE vehicles are conventional vehicles powered solely by an internal combustion engine. EV = electric vehicle.

Source: Goldman Sachs Global Investment Research; T. Rowe Price analysis.

We are also spending more time than before looking at some of the listed state‑owned enterprises (SOEs). China’s SOE reforms have encouraged them to switch from being revenue-driven to being more return-driven with a greater focus on profitability, cash flow, and dividend distribution. Overseas investors are often biased against SOEs simply because they fall within the public sector, even those with a good management team and a strong track record. We search for SOEs with the right incentive scheme, improving return profile, strong cash flow generation capability, solid growth outlook, and attractive valuations that fit into our growth investment framework.

In view of a gradual and more broad‑based recovery with volatility, investors can position their portfolio with a balance along the growth spectrum, including fast-growing disruptors with unique technology or business models and high-quality compounders that can potentially grow their earnings and cash flow.

Conclusion: The Return of Confidence

As consumer confidence gradually returns, the recovery in consumption from services to goods (within goods from small-ticket items to large-ticket products) should in turn pave the way for a pickup in corporate confidence and eventually a rebound in private investment in 2024. Compared with other major economies, China is at a different stage of its business cycle. Benign inflation in contrast to the decades‑high readings seen in other economies gives China the leeway to maintain an accommodative monetary policy and also to introduce selective fiscal support should that prove necessary.

We believe the new leadership’s focus on promoting business is a force to be reckoned with. As the economy stabilizes, the breadth and depth of China’s market should provide ample opportunities for bottom-up investors. The undemanding valuations of Chinese equities have created an investment case for long-term investors, in our view.

Additional Disclosures

MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of Morgan Stanley Capital International Inc, (“MSCI”) and Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. (“S&P”) and is licensed for use by [Licensee]. Neither MSCI, S&P nor any third party involved in making or compiling the GICS or any GICS classifications makes any express or impIied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability and fitness for a particular purpose with respect to any or such standard or classification, Without limiting any or the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

Copyright © 2023, S&P Global Market Intelligence (and its affiliates, as applicable). Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statements of fact.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Jacqueline (Jackie) Liu is a portfolio manager in the International Equity Division. She manages the China Growth Leaders Strategy. Jackie is a member of the Board of Directors of T. Rowe Price Investment Consulting (Shanghai) Co., Ltd. She is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Hong Kong Limited.