Partnering with Us

For more than 80 years, T. Rowe Price has partnered with clients to develop investment solutions to meet their needs and deliver sustainable long-term investment results. For the past 26 years, we have been managing multi-asset portfolios that deliver value across equities, fixed income and alternatives by using various combinations of strategic and tactical asset allocation, fundamental and quantitative analysis, security selection, overlays and outcome-based elements.

IMPORTANT COMPONENTS TO CONSIDER IN TODAY'S MARKET:

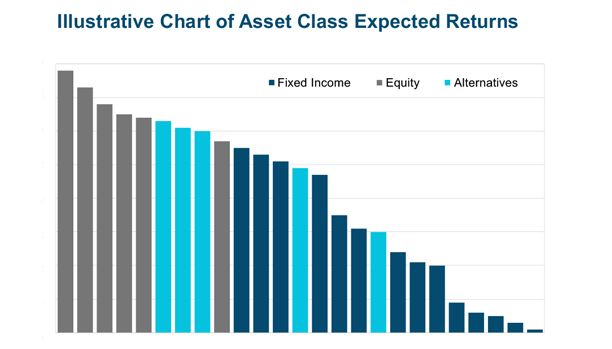

CAPITAL MARKET ASSUMPTIONS

CAPITAL MARKET ASSUMPTIONS

The T. Rowe Price Capital Market Assumptions (CMAs) reflect five-year forecasts for 25 asset classes under five distinct macroeconomic scenarios: baseline, early recession, late recession, bull market, and conditioned on history.

CMAs are best understood as forecasts for the central tendency of forward returns. For this reason, our approach to portfolio construction relies on the use of multiple methods of optimization and robustness checks.

Our baseline forecast incorporates the insights of senior portfolio managers and analysts across our Equity, Fixed Income, and Multi-Asset Divisions and we believe this interdisciplinary approach to developing CMAs, which captures both fundamental and quantitative insights, delivers the best thinking of T. Rowe Price.

VIEW MORE INSIGHTS

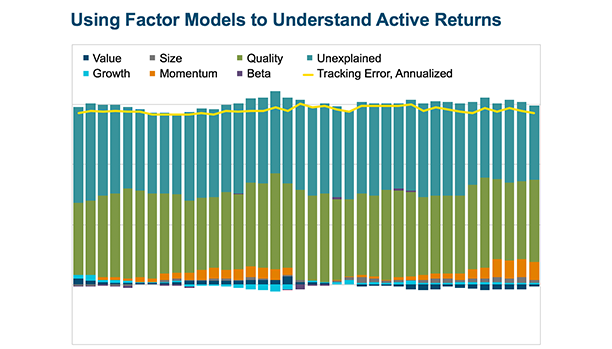

FACTOR ANALYSIS

FACTOR ANALYSIS

The utilization of risk factor analysis has grown significantly in recent years. As the number of risk tools and factor definitions that investors face has increased, so have the potential uses and misuses.

At T. Rowe Price we have dedicated considerable effort to defining and building our approach to portfolio risk factor analysis:

- We have built a robust, proprietary framework that does not rely on any one single approach.

- We are cognizant of the fact that every investment portfolio is unique and needs to be approached individually.

- We consider how evolving market environments require the constant revalidation of risk tools, factors and analysis types.

We apply the same rigorous framework when assessing our client portfolios to ensure that our clients have an equally deep understanding of their portfolio factor exposures and potential opportunities to enhance performance through more deliberate risk management.

VIEW MORE INSIGHTS

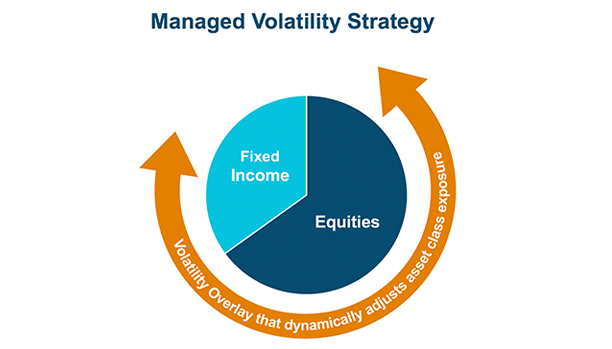

MANAGED VOLATILITY

MANAGED VOLATILITY

Managed volatility strategies use volatility forecasting seeking to help clients stabilize their portfolio's volatility through time. This strategy can be used in multi-asset and single-asset applications, such as equities, to complement other risk managed equity strategies such as minimum (or low) volatility equities.

A managed volatility strategy's main objectives are:

- Stabilizing volatility.

- Mitigating downside risk.

- Maintaining a risk profile in line with an investor's tolerance.

- Preserving long-term portfolio return expectations.

The use of managed volatility capabilities in combination with a single strategy or a multi-asset portfolio may be particularly timely given the recent increase in market volatility and investor concerns regarding drawdown risk.

Our dedicated managed volatility portfolio management team is experienced in the development of a wide range of custom managed volatility solutions for investors around the world.

VIEW MORE INSIGHTS

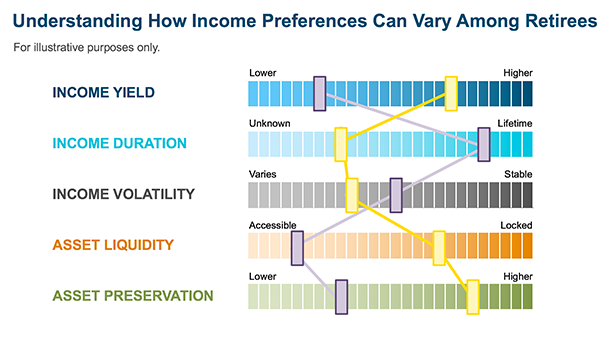

RETIREMENT INCOME

RETIREMENT INCOME

As demographics change and the general population ages, investors across the globe are shifting their focus from wealth accumulation to income distribution.

While the investment marketplace has an abundance of accumulation-oriented solutions, there is little consensus on the optimal manner to construct income solutions that address the many factors that influence retirement income design, including longevity, volatility of income, minimum income sufficiency and legacy goals. With this multitude of considerations, along with a spectrum of products that can address them in various ways, one thing is clear – there is no “one size fits all” approach to generating income in retirement.

As we continue to expand our suite of investment products designed specifically for retirement, T. Rowe Price is also leveraging our extensive research on the importance of incorporating investor preferences when designing retirement income strategies. Our investment and research teams have designed sophisticated tools and analytics that measure the ability of a retirement income solution to meet specific investor preferences, creating a framework that can be used to deliver customized solutions across a spectrum of products. This framework is intended to be flexible, as individual needs and retirement income solutions vary widely by region. Our retirement income expertise capitalizes on a long history of success in the retirement market, both as a retirement plan provider as well as a leading manager of Target Date Funds.

VIEW MORE INSIGHTS

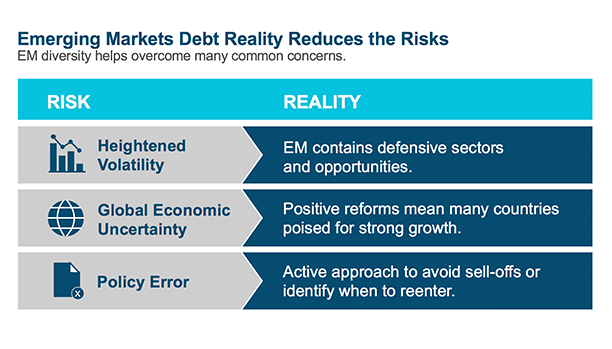

OPPORTUNITIES IN EM DEBT

OPPORTUNITIES IN EM DEBT

Emerging Markets Debt offers an opportunity to generate higher income in environments when developed markets offer a low yield while providing portfolio diversification benefits.

As Emerging Markets countries have matured, debt issuance has grown enormously across its three distinct sectors*:

- Hard currency Sovereign Debt outstanding has grown 143%.

- Hard currency Corporate Debt outstanding has grown 297%.

- Local Currency Government debt outstanding has grown 144%.

The use of Emerging Markets Debt for diversification and return opportunity, whether through a single strategy or a customized blend of the three sectors, offers exciting opportunity for global investors.

With over $80 BN (USD) in Emerging Markets debt and equity investments, more than 50 dedicated EM investment professionals and almost 40 years investing in Emerging Markets, T. Rowe Price is a leading source of innovative and effective Emerging Markets investment solutions.

*Source: JP Morgan. Data from (12/31/08 – 03/31/19). Analysis by T. Rowe Price.

VIEW MORE INSIGHTS

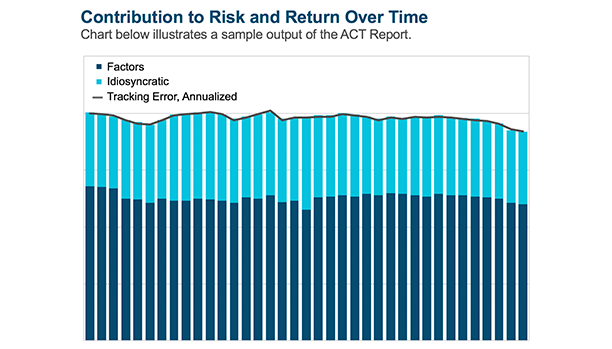

ALPHA, CORRELATION & TRACKING ERROR: THE ACT REPORT

ALPHA, CORRELATION & TRACKING ERROR: THE ACT REPORT

Constructing a properly, but not overly, diversified multi-manager portfolio requires insights that are not always readily identifiable. The true characteristics of any given allocation are not easily observable. To address this uncertainty, T. Rowe Price's Alpha, Correlation, and Tracking Error Report (ACT), is a diagnostic tool that evaluates a multi-manager investment allocation and identifies a wide range of enhancement opportunities.

The ACT report provides an objective evaluation of investment manager performance, both individually and relative to other investment managers, emphasizing what each manager has contributed to the overall portfolio's risk, return, and diversification.

The ACT report is designed to facilitate an interactive and constructive dialogue with clients on their portfolio of active managers with a goal of helping to improve future portfolio outcomes.

VIEW MORE INSIGHTS

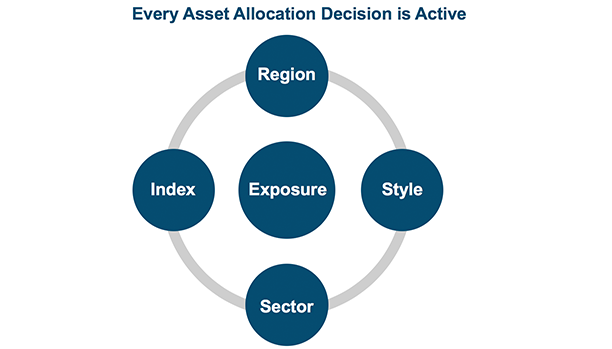

ASSET ALLOCATION VIEWPOINTS

ASSET ALLOCATION VIEWPOINTS

Timing the decision to reallocate among and within different asset classes and geographies confounds even the most experienced investor. At T. Rowe Price, we believe that tactical allocation complements thoughtful strategic design.

Our Asset Allocation Committee reviews global macro trends across all sectors with the goal of determining an optimal portfolio allocation over a 6-18-month time horizon. These insights are cascaded throughout the company and are used as a reference tool for all our investment professionals.

T. Rowe Price has been using a tactical asset allocation methodology for more than 26 years. The Asset Allocation Committee's perspectives are a cornerstone of the Multi-Asset Solutions team and lay the foundation for how we design outcomes for our clients.

VIEW MORE INSIGHTS

LIABILITY DRIVEN INVESTING (LDI)

LIABILITY DRIVEN INVESTING (LDI)

The post Financial Crisis U.S. equity bull market, combined with rising interest rates, has improved the funded status of most defined benefit plans in the United States and has in turn brought prudent pension plan risk management back into the forefront of many sponsors' minds.

The goal of preserving funded status may lead plan sponsors to consider the benefit of custom benchmarks specifically designed to mirror interest rate exposures in their liability and/or LDI solutions that improve the management and monitoring of funded status volatility.

T. Rowe Price has a proprietary Custom Liability Benchmarking framework that offers plan sponsors a level of precision not available through published benchmarks, resulting in closer tracking of plan present values, and improved attribution of the sources of LDI tracking error and funded status volatility.

/trp_image.coreimg.png/1608665488091/ccon0037735-slide8.png)

VIEW MORE INSIGHTS

WHY ACTIVE MATTERS

WHY ACTIVE MATTERS

The debate of active vs. passive investing is rooted in efficiency, alpha generation, risk mitigation and costs. With a backdrop of volatile markets and correlations increasing between disparate asset classes, we believe this strengthens the case for proven active management skill.

As an active manager, we also understand the place for passive investing and we are seeing more situations where institutional investors are looking for ways to blend both into their investment plan design. We view this as a logical step forward in the whole active vs. passive debate.

At T. Rowe Price, we believe in strategic investing, and that by leveraging our size, resources, and rigorous proprietary research, we have an extensive understanding of business models that affords us the patience and conviction to generate accretive long-term investment results.

VIEW MORE INSIGHTS