May 2022 / GLOBAL ASSET ALLOCATION

Global Asset Allocation: May Insights

Discover the latest global market themes

1. Market Perspective

- Global growth estimates are trending lower on heightened geopolitical risk, and COVID-19 lockdowns in China are weighing on supply chains and potentially exacerbating already elevated inflation.

- Despite moderating growth expectations, developed market central banks are expected to advance tightening policies to combat decades‑high inflation, with the US Federal Reserve leading with the most aggressive plans, followed by the Bank of England. The European Central Bank (ECB) accelerates ending asset purchases and considers future rate hikes, while the Bank of Japan remains steadfast on its policy of yield curve control.

- Emerging market central banks remain biased towards tightening to fend off inflation and defend currencies, while China policies continue moving in the opposite direction to stimulate the economy to help catch up to growth targets following COVID-19 lockdowns.

- Key risks to global markets include central bank missteps, commodity impact of the Russia‑Ukraine conflict, lingering inflation and China balancing growth amid COVID-19 lockdowns.

2. Portfolio Positioning

As of 30 April 2022

- Despite lower valuations amid recent declines, we remain underweight equities given a moderating growth and earnings outlook with a hawkish Fed battling high inflation. Within fixed income, we remain underweight bonds and overweight cash.

- Within equities, we continue to overweight value and underweight growth to provide a hedge should inflationary pressures persist longer than expected.

- Within fixed income, we continue to favour inflation-protected securities and shorter‑duration and higher‑yielding sectors through overweights to emerging market debt and high yield bonds supported by still solid fundamentals while keeping a cautious eye on liquidity and volatility.

- To provide some defence against growing market risks, we further moderated our underweight to European government bonds following recent moves higher in rates.

3. Market Themes

Where to Hide?

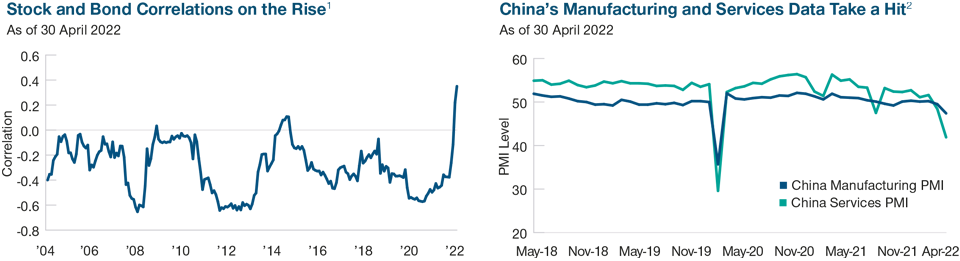

War, inflation and lingering COVID-19 impacts have set the stage for a challenging start to 2022 for investors, with both stocks and bonds down over 9% in response. While dynamic, stocks and bonds on average have a low correlation with each other, and their correlation can move sharply negative during risk‑off periods. However, this time is quite unique, with runaway inflation sparking aggressive central bank tightening all while growth is moderating amid a world full of rising risks. These concerns of rising rates and inflation are contributing to a retreat in bonds. At the same time, rising rates and slowing growth are weighing on equity markets in a period where valuations are already above average. This unfortunate rise in stock‑to‑bond correlation is weighing on even the most conservative of investors. While it’s hard to gauge the path forward given the unprecedented confluence of issues facing global markets, a cautious approach is warranted, especially to mitigate more extreme tail events, including more persistent inflation or a hard landing in the economy.

Past performance is not a reliable indicator of future performance.

1 Chart represents rolling 2-year correlation of monthly price changes of the S&P 500 Index and U.S. 10-Year Treasury Futures.

2 Chart shows China Manufacturing PMI Index and China Non-Manufacturing PMI Index (representing Services PMI).

Sources: Bloomberg Finance L.P. and S&P (see Additional Disclosures).

Walking a Tightrope

As the rest of the world is seeing fewer outbreaks and learning to cope with COVID‑19, China, on the other hand, has faced a new wave of outbreaks, forcing it to enact ‘zero‑COVID’ lockdown policies, which are taking a toll on the nation’s growth and potentially spilling over to the rest of the world. The stringent lockdowns in Shanghai, an export hub, and most recently in Beijing are weighing on the ability to transport goods, further impacting already fractured global supply chains. The market increasingly expects China to further ease monetary and fiscal policy in response to the recent weakness. However, as they do, they will not want to reflate speculative bubbles that they burst last year, most notably the housing sector. With the presidential election approaching and President Xi Jinping up for an unprecedented third term, he seems determined to reach China’s lofty 5.5% gross domestic product target that is severely challenged by COVID‑19 lockdowns. This leaves policymakers walking a tightrope should they seek to maintain the aggressive lockdowns and reach growth targets while providing just enough stimulus not to overheat some sectors of the market.

For a region-by-region overview, see the full report (PDF).

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.