February 2022 / INVESTMENT INSIGHTS

Rethinking Fixed Income Allocations

Sourcing strategies with varying risk and return drivers is key

Key Insights

- The evolution of fixed income markets and increasingly diverse strategies dictate the need to evaluate strategies along a flexibility and liquidity continuum.

- Asset allocators should consider a risk-budgeting approach to allocate across the fixed income continuum based on their policies and guidelines.

- We believe that core bonds still have an important role to add diversification and liquidity to a portfolio, but this role is now smaller and less impactful.

Clients often ask us about how to approach the fixed income allocation within a broadly diversified portfolio in terms of sourcing return and risk. We encourage these questions because we believe that a deeper dive into fixed income as part of an asset allocation review is necessary to determine if a client is getting the most potential out of the fixed income allocation.

At a minimum, asset allocators should know how each component of their fixed income portfolio contributes to their goals as well as how it does or does not overlap with other parts of the portfolio. This is particularly true given the rapidly expanding investible universe in sectors such as emerging markets debt, bank loans, and private credit. The range of nontraditional and more flexible bond strategies that rely less on markets and more on manager skill that are available to allocators is also meaningfully larger than it was only five years ago, making it much more difficult to categorize strategies based on traditional asset class labels.

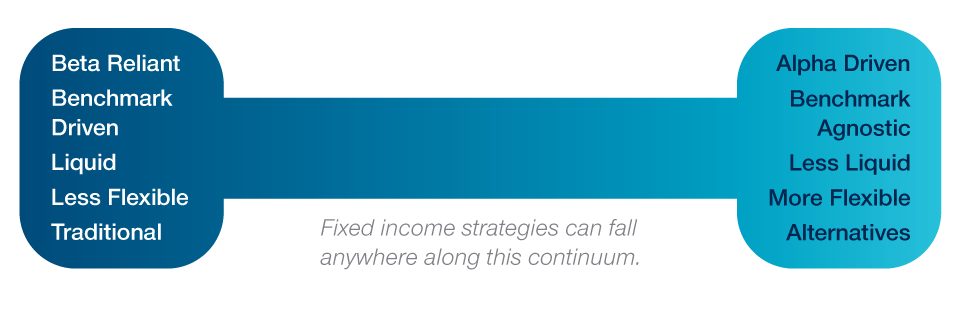

Allocating Along the Continuum

Relying primarily on core investment‑grade bonds with a modest allocation to non‑core below investment‑grade bonds may handcuff your potential to generate returns and mitigate risk. T. Rowe Price’s multi‑asset team has found that better investment return and risk outcomes are found using approaches that incorporate more flexible fixed income strategies. This may require a mindset shift for some, but the change can be relatively easy to implement and monitor. We suggest viewing the fixed income allocation and underlying strategies along a continuum.

We believe asset allocators are better served by increasing the breadth within the fixed income portion of their portfolios by adding exposure to alternative—or more flexible—fixed income investments that complement the traditional bond allocations.

Understanding Risk Contribution at the Strategy Level and the Total Portfolio Level

Investors should aim to understand the risks driving the fixed income component strategies and their contribution to total portfolio risk. At a minimum, investors should have a good understanding of each strategy’s exposure to risk-free rates and equities and each strategy’s contribution to these exposures at the total portfolio level since they are often the primary sources of diversification and growth. But we also recommend digging a layer or two deeper to understand additional exposures—including credit spreads,1 inflation, currency, illiquidity, and active risk—as they can all be sources of growth and diversification. Not doing so increases the likelihood of surprises at the strategy or total portfolio level that may come from overlapping risks across strategies.

In the context of a broader portfolio, a nontraditional, more flexible fixed income strategy is essentially a source of nondiversified alpha.2 Examining the fixed income components from a bottom‑up view and designing beta3 exposure can help make the fixed income allocation more efficient in both capturing alpha and managing risk exposure. Understanding the underlying fixed income strategies in a portfolio can help determine whether perceived changes in alpha are actually movements in beta. Monitoring the strategies over time and in different market environments can help differentiate between alpha and beta.

Understanding these risk interactions will inform investors about how to fund strategies to keep risk steady or to adjust it. When looking to increase a credit allocation, for instance, knowledge of the impact on overall portfolio risk will help determine whether to fund the allocation change from core or core plus fixed income strategies or from a combination of fixed income and equity exposures depending on the risk factors associated with the increased credit allocation.

Core Bond Allocation Still Plays a Key Role

We believe that core bonds still have an important role as a way to add diversification against a downturn in risk assets as well as liquidity and stability to a portfolio. However, this role is smaller and less impactful than in the past because we do not expect the same level of diversification given today’s miniscule yields. The size of the core component should be based on the client’s unique needs to meet short‑term liabilities or expenses. We suggest that investors consider complementing a core bond allocation with other types of fixed income strategies, such as liquid alternatives, that are less correlated with core bonds in a range of market environments.

Another traditional element of a fixed income allocation—carry, or the difference in yield between a fixed income investment and the risk‑free rate—should now play an even larger role in a portfolio, in our view. This is particularly true because valuations in essentially all asset classes are elevated relative to historical standards.

1 Credit spreads measure the additional yield that investors demand for holding a bond with credit risk over a similar‑maturity, high‑quality government security.

2 Alpha is the risk‑adjusted excess return of an investment relative to its benchmark.

3 Beta measures the relative volatility, or risk, of a security or group of securities relative to the risk of the broad market or a specific factor.

WHAT WE’RE WATCHING NEXT

A negative correlation between Treasury bond prices and risk assets allows Treasuries, which are a cornerstone of most core bond allocations, to act as an effective diversifier for sell‑offs in higher‑risk asset classes such as equities and high yield bonds. While the level of correlation has changed over time, we still believe that longer‑term Treasuries again are a useful hedge against a major downturn in risk assets.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

February 2022 / INVESTMENT INSIGHTS