April 2021 / INVESTMENT INSIGHTS

The Long-Term Appeal of Durable Growers Remains Intact

Some of the best large-cap growth stories have often contained multiple chapters

Key Insights

- The shift in market leadership from growth to value may persist but should not preclude certain quality growth stocks from performing well, in our view.

- We focus on identifying opportunities where we think the market undervalues the potential durability of a company’s growth story.

- E‑commerce is an area where we see secular tailwinds and options for well‑positioned companies to expand into adjacent business lines.

The value stocks in the large‑cap Russell 1000 Index have outperformed their growth counterparts in recent months, but this near‑term regime shift does not dim our conviction in high‑quality companies that we believe can compound in value over the long run by growing their revenue and cash flows.

When the market focuses more on a robust cyclical recovery in certain companies’ earnings, our approach can lag in the near term. Nevertheless, the two of us remain confident that the rewards of the portfolio’s emphasis on potential compounders are most likely to be realized over a full market cycle.

We strive to develop a deep understanding of the companies driving innovation. We also have observed the market’s tendency to undervalue the potential durability of a company’s free cash flow growth. Our differentiated insights into these factors look beyond the near term and are critical in shaping how we position for the long run—a point underscored by the portfolio’s holdings in e‑commerce, an area where we see strong secular tailwinds and options for companies to expand into adjacent business lines.

Secular Growth’s Enduring Appeal

What should investors make of the market’s recent rotation from large‑cap growth stocks into their value counterparts?

The main factors powering this regime shift do not appear to have exhausted themselves, although considerable uncertainty remains in the near term. So much depends on the progress in taming the coronavirus pandemic, as the combination of some return to normalcy and massive fiscal stimulus could unleash a powerful wave of pent‑up demand that would favor value stocks with greater sensitivity to economic conditions. The market bid up certain growth stories last year, seemingly without regard to valuation, suggesting that this unwinding process for selected growth stocks could have more room to run in the near term. (See Figure 1.) However, we note that many of the large‑cap growth bellwethers now trade at valuations that no longer appear unreasonable when we consider these companies’ growth prospects.

In addition, underlying business fundamentals do not lead us to believe that this change in market leadership will necessarily or ultimately prove to be durable.

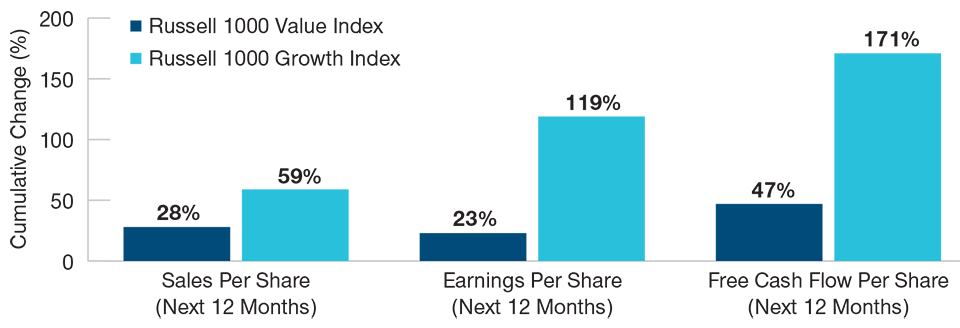

Value’s extended run of relative underperformance since 2005 coincided with a period of widespread innovation, especially among rapidly growing technology companies, which has disrupted several value‑oriented industries by siphoning profit pools and/or introducing deflationary pressures that compress profit margins. The disparate fortunes of the disruptors and the disrupted help to explain the wide gap in per share revenue, earnings, and free cash flow growth between growth and value stocks in the Russell 1000 Index prior to the pandemic. (See Figure 2.)

Large‑Cap Growth Valuations Remain Elevated

(Fig. 1) Russell 1000 Growth Index price‑to‑earnings ratio

Past performance is not a reliable indicator of future performance.

December 31, 1997, to February 28, 2021.

Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

Once the cyclical forces driving the recent outperformance in value stocks begin to fade and/or their valuations become frothy, we believe that the secular forces driving innovation and disruption—trends that we weigh heavily in our search for potential long‑term compounders—should return to the fore.

Selective Cyclicality

In terms of relative performance, the early stages of the business cycle—when the market tends to favor stocks that offer the most torque to accelerating economic growth—can present near‑term challenges for the high‑quality secular growers that we favor. However, as long as the high‑quality companies in the portfolio can execute their long‑term strategies and grow their cash flows rapidly, we remain confident in their potential to compound in value over a full economic cycle.

Our bottom‑up approach to buying and holding potential compounders has resulted in a portfolio that should offer some leverage to an acceleration in economic growth, even if we do not buy cyclical stocks purely for exposure to a near‑term economic recovery.

Facebook’s and Alphabet’s (Google’s parent company) advertising businesses may stand to benefit from the economic recovery if progress in containing the coronavirus pandemic creates a surge in demand for travel and other industries that advertise heavily online. We view this near‑term cyclical exposure as a welcome option in the current environment, but our longer‑term thesis hinges, in part, on our belief that online advertising should take share from traditional media outlets that have been losing audience. In both instances, we continue to monitor regulatory developments in the U.S. and Europe and consider these factors in our assessment of Facebook’s and Alphabet’s risk/reward profiles.

Divergent Fundamentals Before the Pandemic

(Fig. 2) Large‑cap growth names have exhibited superior fundamentals

June 1, 2007, to March 31, 2020.

Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

Our valuation discipline means that we are finding fewer opportunities in cyclical sectors that meet our investment criteria, although we did take advantage of weakness last year to add incrementally to some names in the restaurant and hospitality industries as well as select opportunities in the industrials and financials sectors. Here, we focused on companies that we believe should emerge stronger from the pandemic and have the potential to compound in value over a multiyear time horizon, thanks to the quality of their businesses and idiosyncratic potential growth drivers.

Still, the portfolio places a heavy emphasis on high‑quality companies that we believe offer exposure to powerful secular growth trends, especially those related to the digitalization of the enterprise and consumer behavior.

E‑Commerce: A Case Study Potential Durable Growth

Instead of debating whether it’s time to sell down or add to cyclical stocks in the near term, the two of us remain focused on the area where we believe we have an edge and can potentially add the most value over a full economic cycle: identifying opportunities where we think that the market does not fully appreciate the possible strength and length of a company’s growth story.

E‑commerce is one area where we are finding compelling opportunities, in part, due to our differentiated insights and willingness to look beyond the near term.

The health crisis accelerated adoption of e‑commerce among households and small to mid-size businesses that previously had little to no online presence. Although these behavioral shifts worked to the benefit of the secular growers that have exposure to these trends, this phenomenon naturally raises questions about the extent to which pulled‑forward growth may have shortened these companies’ growth runways.

Yes, adoption of online shopping has accelerated significantly. But a comparison of e‑commerce penetration rates in the U.S. and Europe to economies in Asia suggests that this trend has more room to run as consumers become more comfortable purchasing a growing array of products online, including groceries and other retail categories that had proved resistant to online competition.

Amazon.com, for example, offers exposure to this trend through the breadth of production selection on its online marketplace, its substantial logistics investments that are increasing the array of items on which it offers one‑day shipping, and its foothold in the grocery category through its Whole Foods Market subsidiary. But the adjacent opportunities stemming from this core business are also a key part of our investment thesis. By virtue of Amazon.com’s proximity to the point of purchase, the company’s unique insights into consumer spending have enabled it to create a growing online advertising business.

The potential for growth stories that have a second and third chapter is part of what gives us confidence in the e‑commerce names in which we have invested—from a software company that provides modular e‑commerce solutions for small and mid-size businesses to Facebook and other online platforms that are leveraging their massive user bases to push into the emerging fields of interactive and social commerce. We believe that, at scale, these e‑commerce operations should lend themselves to ancillary opportunities in online payments and targeted advertising. Further down the line, the data generated by buyers and merchants on these platforms could also form the basis of various fintech products, among other possibilities.

With the market often overly focused on the near term, we believe that some of our best opportunities to add value come from developing a deep knowledge of industry dynamics and our willingness to take a longer view on how a company’s potential growth story might evolve.

A Thoughtful Transition

Larry Puglia is retiring from T. Rowe Price at the end of this year, after more than 31 years at the company. Paul Greene, a 14‑year veteran at the company, will become portfolio manager of the US Large‑Cap Core Growth Equity Strategy effective October 1, 2021. A lengthy transition is consistent with our long‑held practice of deep and extensive collaboration. Paul has been the associate portfolio manager of the strategy since January 1, 2020, and has worked closely with Larry since 2010, when he became a member of the strategy’s Investment Advisory Committee. In addition, Paul has worked with Larry for many years as an analyst covering media and internet stocks and shared a similar focus on investing in potential long‑term compounders during his tenure (October 1, 2013, to the end of 2019) as portfolio manager of the Communications and Technology Equity Strategy. Many of the large communication services companies that Paul covered became very significant positions in the US Large‑Cap Core Growth Equity Strategy.

WHAT WE’RE WATCHING NEXT

In addition to monitoring company‑level developments, we’re paying close attention to developments in Washington, D.C., especially how President Joe Biden’s infrastructure spending bill shapes up later in the year. The administration has been vocal in its support for initiatives that would encourage the adoption of electric vehicles, one of the key growth trends we’re watching, as well as increases in corporate and personal tax rates that could have important implications for markets and investors.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

April 2021 / MULTI-ASSET SOLUTIONS