Rebalancing Through Market Drawdowns

A prudent approach can be critical when markets are stressed.

Executive Summary

- Although investors may be reluctant to add to higher-risk exposures in a market drawdown, we believe it is essential to maintain a prudent rebalancing approach.

- Our analysis of historical and simulated market drawdowns suggests that rebalancing potentially improves outcomes relative to a non-rebalanced portfolio.

- We believe investors should select the rebalancing rule that they think is most appropriate and adhere to it through all periods, including market drawdowns.

Rebalancing asset exposures is fundamental to prudent portfolio management and has long been considered a key determinant of long‑term performance. Regularly reorienting to targeted long‑term asset allocations helps ensure that all risk exposures in the portfolio are intentionally accepted. However, many investors may be reluctant to follow their normal rebalancing policies in periods of market stress, when adding to higher‑risk exposures may seem particularly unpalatable.

We believe it is essential that investors maintain a prudent rebalancing approach. Our analysis of both historical and simulated equity market drawdowns found that sticking to an investment policy’s rebalancing rule typically led to better outcomes when compared with a passive strategy of allowing portfolio exposures to drift with market movements.

In this paper, we analyze the impact of various rebalancing methods in both historical and simulated market drawdowns. We compare various rebalancing rules: two of them calendar‑based (monthly and quarterly) and two that rely on exposure bands (±2.5% and ±5.0%). Our findings suggest that during market drawdowns and subsequent price recoveries:

- Using Monte Carlo analysis, we found that all of the rebalancing rules we tested outperformed a non‑rebalanced portfolio in at least 90.9% of simulated scenarios.

- In our simulations, certain rebalancing methods potentially outperformed others during specific types of market drawdowns. However, it is impossible for investors to know in advance the type of drawdown they are experiencing.

- Our simulations suggested that there is no “silver bullet” rebalancing rule, given the multiple considerations that need to be addressed when designing and maintaining rebalancing policies.

We believe investors should select the rebalancing approach that they believe is most appropriate for them, given their own circumstances, and adhere to it through all periods, especially during market drawdowns and recoveries.

We believe it is essential that investors maintain a prudent rebalancing approach.

We believe it is essential that investors maintain a prudent rebalancing approach.

The Importance of Rebalancing

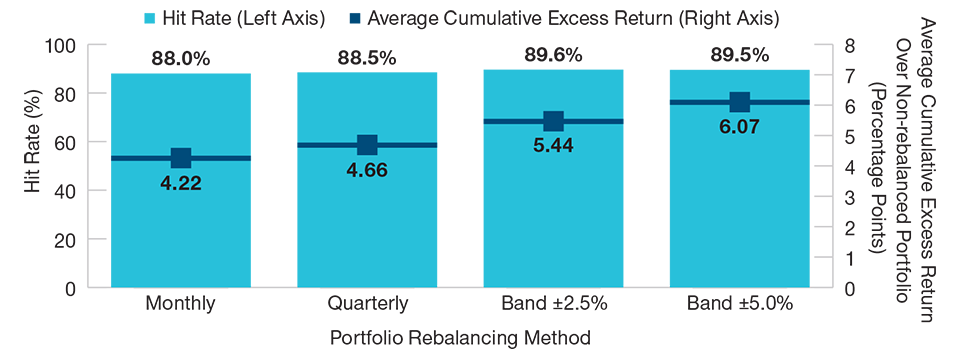

Establishing and implementing a portfolio rebalancing policy is widely believed to improve portfolio performance over full market cycles. Over rolling 10‑year periods since 1989, any of our four rebalancing methods would have outperformed a hypothetical non‑rebalanced portfolio. Figure 1 shows the average cumulative excess returns and hit rates (the percentage of all rolling periods in which the hypothetical rebalanced portfolio would have outperformed) for the various hypothetical rebalancing methods versus a hypothetical non‑rebalanced portfolio with assumed initial allocations of 60% to global equities and 40% to U.S. bonds.

The hypothetical rebalanced portfolios would have outperformed a hypothetical non‑rebalanced portfolio in a large majority of the historical 10‑year rolling periods covered in our study, ranging from an 88.0% hit rate for a monthly rebalancing rule to a 89.6% hit rate for a rule that sought to keep relative exposures within ±2.5% bands. The average margin of cumulative excess return would have ranged from 4.22 percentage points (for monthly rebalancing) to 6.07 percentage points (for a rebalancing policy based on ±5% bands).

Assuming a hypothetical starting portfolio balance of USD 1,000,000, the average improvement to ending balances from adhering to one of the rebalancing rules we tested would have ranged from USD 42,199 to USD 60,652.

Stick to the Policy Even During Market Drawdowns

Despite the potential benefits of adhering to clear portfolio rebalancing rules, investors may be tempted to abandon their rebalancing policies during market drawdowns to avoiding buying into falling markets. To examine the potential pitfalls of such an approach, we analyzed our four rebalancing methods in a sample of historical and simulated market sell‑offs.

Hypothetical Rebalanced vs. Non-rebalanced Portfolios1

(Fig. 1) Hit rates and average cumulative excess returns over rolling 10-year periods

January 31, 1989, through March 31, 2020.

1 Initial portfolio weights: 60% equity/40% bonds. Equities represented by the Morgan Stanley Capital International All Country World Index (MSCI ACWI); bonds by the Bloomberg Barclays U.S. Aggregate Bond Index. The results shown above are hypothetical, do not reflect actual investment results, and are not indicative of realized past or future performance. See appendix for rebalancing methodology.

Sources: MSCI and Bloomberg Index Services Limited (see Additional Disclosures); all data analysis by T. Rowe Price.

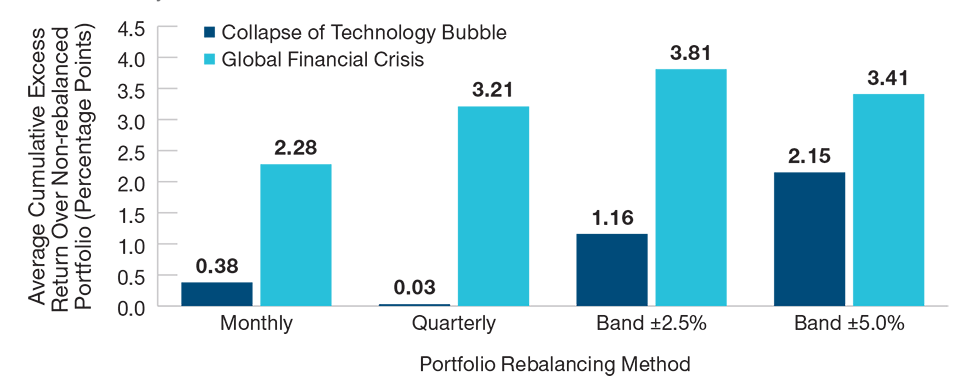

Outperformance of Hypothetical Rebalanced vs. Non‑rebalanced Portfolios1

(Fig. 2) Average cumulative excess returns from market peak through trough and recovery

1 Initial portfolio weights: 60% equity/40% bonds. Equities represented by the MSCI ACWI; bonds by the Bloomberg Barclays U.S. Aggregate Bond Index. The results shown above are hypothetical, do not reflect actual investment results, and are not indicative of realized past or future performance.

See appendix for bear market peak, trough, and recovery dates as well as information on rebalancing methodology.

Sources: MSCI and Bloomberg Index Services Limited (see Additional Disclosures); all data analysis by T. Rowe Price.

We first examined how the various rebalancing methods would have performed in two previous market events: the bear market that followed the technology bubble of the late 1990s, and the 2007–2009 global financial crisis. As shown in Figure 2, all of the hypothetical rebalanced portfolios would have outperformed a hypothetical non‑rebalanced portfolio, on average, during and after the two historical market events.

We found considerable dispersion across the rebalancing methods in terms of both the value added and the frequency of outperformance. Moreover, while historical scenarios can be insightful, future market sell‑offs and recoveries are likely to follow different paths. This observation prompted us to expand our analysis to study a wide range of simulated scenarios using Monte Carlo analysis to understand if certain rebalancing approaches could be more effective than others in market drawdowns.

In order to capture potential differences in efficacy across the four rebalancing methods analyzed, we modeled hypothetical equity/bond portfolios across 1,000 simulated equity market drawdowns and subsequent recoveries.

We sought to examine rebalancing methods from a variety of perspectives:

- Did the rebalancing methods work across the simulations in aggregate?

- Did the results change if we parsed the simulated data into more nuanced scenarios (e.g., depths and speeds of the drawdowns and recoveries)?

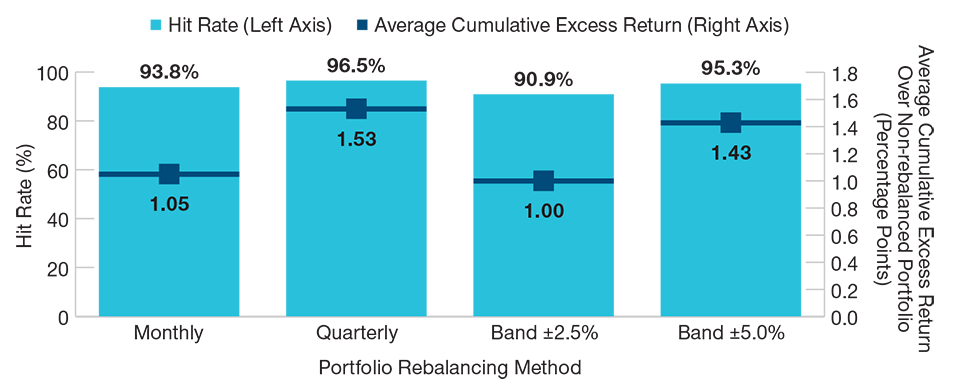

We found high conviction in our answer to the first question, as the hypothetical rebalanced portfolios outperformed a hypothetical non‑rebalanced portfolio in the vast majority of our simulated downturns at meaningful levels. Specifically, Figure 3 shows the percentage of the simulated scenarios in which a hypothetical rebalanced portfolio outperformed a hypothetical non‑rebalanced portfolio. In at least 90.9% of the simulated scenarios, the rebalanced portfolio outperformed the non‑rebalanced portfolio.

While rebalancing operated in a falling market during the drawdown and in a rising market through the subsequent recovery, each method tended to outperform a hypothetical non‑rebalanced portfolio over the full cycle. Additionally, as also shown in Figure 3, the outperformance of each rebalancing method versus a hypothetical non‑rebalanced portfolio was meaningful, ranging from 1.00 to 1.53 percentage points of additional cumulative excess return versus the passively drifting non‑rebalanced portfolio, which we would view as the “rebalancing alpha.”

While we believe the aggregate results of our simulations make a strong case for rebalancing, the path‑dependent nature of equity drawdowns and recoveries merits a closer look at the dispersion of potential outcomes across a variety of scenarios. Therefore, we examined subsets of results to ensure that our findings were robust across a range of simulated bear markets and recoveries. Specifically, we studied results within two segmentations of the data:

- the depth of the simulated equity drawdown

- the duration of the overall event from drawdown through recovery.

We again found that hypothetical portfolios that were rebalanced by any of the methods we modeled consistently outperformed a hypothetical non‑rebalanced portfolio.

Simulated Performance of Hypothetical Rebalanced vs. Non‑rebalanced Portfolios1

(Fig. 3) Hit rates and average cumulative excess returns across all simulations

1 Initial portfolio weights: 60% equity/40% bonds. Equities represented by the MSCI ACWI; bonds by the Bloomberg Barclays U.S. Aggregate Bond Index. The results shown above are based on Monte Carlo simulations. See appendix for information on simulation parameters and methodology.

Sources: T. Rowe Price, MSCI, and Bloomberg Index Services Limited (see Additional Disclosures); all data analysis by T. Rowe Price.

Figure 4 shows the results by equity depth. As noted, we saw outperformance across all rebalancing approaches. As the depth of the simulated equity market drawdown was deepened, we found that the looser rebalancing approaches (quarterly rebalancing and the ±5% bands) provided relatively better results. Intuitively, this made sense because, in a very deep drawdown, investors potentially could benefit by allowing their portfolios to drift into defensive assets. However, in reality, investors have no way of knowing the ultimate depth of a drawdown as they are experiencing it.

The most important takeaway here is that all of the rebalancing rules we examined potentially can add value, and investors should adhere to the approach that they believe makes the most sense given their overall situation.

Simulated Outperformance of Hypothetical Rebalanced Portfolios by Depth of Equity Drawdown1

(Fig. 4) Hit rates and average cumulative excess returns across all simulations

1 Initial portfolio weights: 60% equity/40% bonds. Equities represented by the MSCI ACWI; bonds by the Bloomberg Barclays U.S. Aggregate Bond Index. The results shown above are based on Monte Carlo simulations. See appendix for information on simulation parameters and methodology.

Sources: T. Rowe Price, MSCI, and Bloomberg Index Services Limited (see Additional Disclosures); all data analysis by T. Rowe Price.

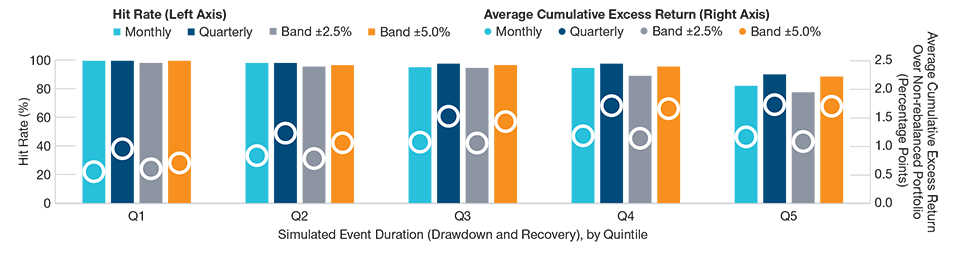

We also considered the dimension of time. Specifically, we studied the various rebalancing methods through drawdowns and subsequent recoveries of differing lengths. Again, Figure 5 shows that all of the rebalancing approaches we modeled consistently outperformed across scenarios, regardless of length.

It is important to distinguish between the two phases of a market sell‑off: the drawdown and the subsequent recovery. Because a non‑rebalanced portfolio allows risk‑asset exposures to adjust with market movements and, thus, does not continue buying into risk assets during a decline, rebalancing may underperform during drawdowns. However, by regularly returning portfolio allocations to targeted weights, a rebalanced portfolio potentially can be better positioned for a subsequent market rebound. As a result, a rebalanced portfolio may lead a non‑rebalanced portfolio in a recovery by a larger magnitude than its underperformance during the previous drawdown.

The fact that this conclusion held across various drawdown depths and event durations in our simulations gives us further confidence that investors should adhere to their usual rebalancing policies regardless of the market environment.

Simulated Outperformance of Hypothetical Rebalanced Portfolios By Total Event Duration1

(Fig. 5) Hit rates and average cumulative excess returns across all simulations

1 Initial portfolio weights: 60% equity/40% bonds. Equities represented by the MSCI ACWI; bonds by the Bloomberg Barclays U.S. Aggregate Bond Index. The results shown above are based on Monte Carlo simulations. See appendix for information on simulation parameters and methodology.

Sources: T. Rowe Price, MSCI, and Bloomberg Index Services Limited (see Additional Disclosures); all data analysis by T. Rowe Price.

Conclusion

Rebalancing portfolios in accordance with a set policy helps align allocations with investor expectations and potentially helps minimize unintended risk. Our results show that disciplined adherence to a balancing policy, both over the long term and through periods of market stress, potentially can lead to a meaningful improvement in portfolio performance.

While we recognize that buying assets that are falling in value can be a difficult decision, we believe that investors should not abandon their normal rebalancing policies, especially during market sell‑offs.

Additional Disclosures

MSCI. MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Appendix: Study Methodology

Hypothetical performance results (Fig. 2) are based on the following historical market events.

The date ranges shown above reflect the equity market peak for the MSCI ACWI prior to the downturn, the index trough, and the date of its recovery to the previous peak.

Simulation Analysis

The equity return paths in our simulations were based on the assumed parameters below and were modeled to reflect:

- drawdowns to a randomly chosen depth of -20% to -50%

- recoveries back to prior peak levels.

The performance of the hypothetical rebalanced and non-rebalanced portfolios were based on average daily returns and average daily standard deviation for the MSCI ACWI and the Bloomberg Barclays U.S. Aggregate Bond Index, pooled across drawdown and recovery periods for both the technology bubble and the global financial crisis. All index returns were gross of dividends.

Daily returns were assumed to reflect normal distributions, with the parameters defined below.

Rebalancing During Market Events

- Starting allocations: All portfolios were assumed to have starting allocations of 60% equity/40% fixed income at market peaks, ±5% equity. Approximately half of the portfolios were assumed to begin with equity overweights and half with equity underweights within the 5% band.

- Monthly rebalancing: Portfolios following a monthly rebalancing rule were assumed to be initially rebalanced exactly 21 days from the start of the simulated market event and every 21 days thereafter.

- Quarterly rebalancing: Portfolios following a quarterly rebalancing rule were assumed to be initially rebalanced on a randomly chosen day within the first 63 days of the simulated market event and every 63 days thereafter.

- Banded rebalancing: Portfolios following banded rebalancing rules were assumed to be initially rebalanced when portfolio equity allocation deviated ±2.5% or ±5.0% versus their 60% equity allocation targets and each time such a deviation occurred thereafter.

Simulated Event Duration (Drawdown & Recovery) Quintile Breakpoints

T. Rowe Price Methodology: Monte Carlo Analysis

Monte Carlo simulations model future uncertainty. In contrast to tools generating average outcomes, Monte Carlo analyses produce outcome ranges based on probability thus incorporating future uncertainty. The projections are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. The simulations are based on assumptions. The materials present only a range of possible outcomes. Actual results are unknown therefore results may be better or worse than the simulated scenarios. Investors should be aware that the potential for loss (or gain) may be greater than demonstrated in the simulations.

Modeling Assumptions

The primary asset classes used for this analysis are outlined in the Appendix. The analysis includes 1,000 scenarios. The portfolio is assumed to be rebalanced based on rules outlined in the Appendix.

Material Assumptions

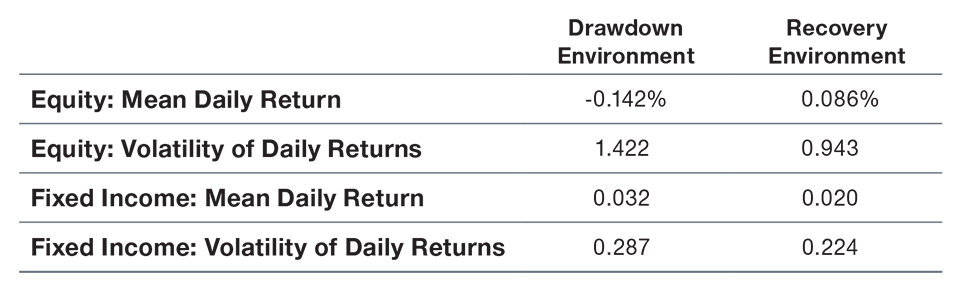

The primary assumptions underlying the analysis are mean daily returns and the volatility of daily returns of asset classes based on historical periods and the indexes noted in the Appendix.

Material Limitations

The analysis relies on return assumptions of asset classes (not investment products) to generate a wide range of possible return scenarios. There is no certainty that the future path of asset class returns is within the range of outcomes modeled. As a consequence, the results of the analysis should be viewed as comprehensive, but not exhaustive. Users should also keep in mind that seemingly small changes in input parameters may have a significant impact on results.

Additional material limitations include:

- Market crises can cause asset classes to perform similarly, lowering the accuracy of our projected return assumptions, and diminishing the benefits of diversification (that is, of using many different asset classes) in ways not captured by the analysis. As a result, returns actually experienced by the investor may be more volatile than projected in our analysis.

- Asset class dynamics, including but not limited to risk, return, and the duration of drawdown and recovery environments, can differ than those in the modeled scenarios.

- The analysis does not use all asset classes.

- Taxes, transaction costs, other potential expenses, potential for alpha from active management, and investment management fees are not taken into account.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Australia—Issued in Australia by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. For Wholesale Clients only.

Brunei—This material can only be delivered to certain specific institutional investors for informational purpose upon request only. The strategy and/or any products associated with the strategy has not been authorised for distribution in Brunei. No distribution of this material to any member of the public in Brunei is permitted.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45-106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

China—This material is provided to specific qualified domestic institutional investor or sovereign wealth fund on a one-on-one basis. No invitation to offer, or offer for, or sale of, the shares will be made in the People’s Republic of China (“PRC”) (which, for such purpose, does not include the Hong Kong or Macau Special Administrative Regions or Taiwan) or by any means that would be deemed public under the laws of the PRC. The information relating to the strategy contained in this material has not been submitted to or approved by the China Securities Regulatory Commission or any other relevant governmental authority in the PRC. The strategy and/or any product associated with the strategy may only be offered or sold to investors in the PRC that are expressly authorized under the laws and regulations of the PRC to buy and sell securities denominated in a currency other than the Renminbi (or RMB), which is the official currency of the PRC. Potential investors who are resident in the PRC are responsible for obtaining the required approvals from all relevant government authorities in the PRC, including, but not limited to, the State Administration of Foreign Exchange, before purchasing the shares. This document further does not constitute any securities or investment advice to citizens of the PRC, or nationals with permanent residence in the PRC, or to any corporation, partnership, or other entity incorporated or established in the PRC.

DIFC—Issued in the Dubai International Financial Centre by T. Rowe Price International Ltd. This material is communicated on behalf of T. Rowe Price International Ltd. by its representative office which is regulated by the Dubai Financial Services Authority. For Professional Clients only.

EEA ex-UK—Unless indicated otherwise this material is issued and approved by T. Rowe Price (Luxembourg) Management S.à r.l. 35 Boulevard du Prince Henri L-1724 Luxembourg which is authorised and regulated by the Luxembourg Commission de Surveillance du Secteur Financier. For Professional Clients only.

Hong Kong—Issued in Hong Kong by T. Rowe Price Hong Kong Limited, 6/F, Chater House, 8 Connaught Road Central, Hong Kong. T. Rowe Price Hong Kong Limited is licensed and regulated by the Securities & Futures Commission. For Professional Investors only.

Indonesia—This material is intended to be used only by the designated recipient to whom T. Rowe Price delivered; it is for institutional use only. Under no circumstances should the material, in whole or in part, be copied, redistributed or shared, in any medium, without prior written consent from T. Rowe Price. No distribution of this material to members of the public in any jurisdiction is permitted.

Korea—This material is intended only to Qualified Professional Investors upon specific and unsolicited request and may not be reproduced in whole or in part nor can they be transmitted to any other person in the Republic of Korea.

Malaysia—This material can only be delivered to specific institutional investor upon specific and unsolicited request. The strategy and/or any products associated with the strategy has not been authorised for distribution in Malaysia. This material is solely for institutional use and for informational purposes only. This material does not provide investment advice or an offering to make, or an inducement or attempted inducement of any person to enter into or to offer to enter into, an agreement for or with a view to acquiring, disposing of, subscribing for or underwriting securities. Nothing in this material shall be considered a making available of, solicitation to buy, an offering for subscription or purchase or an invitation to subscribe for or purchase any securities, or any other product or service, to any person in any jurisdiction where such offer, solicitation, purchase or sale would be unlawful under the laws of Malaysia.

New Zealand—Issued in New Zealand by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. No Interests are offered to the public. Accordingly, the Interests may not, directly or indirectly, be offered, sold or delivered in New Zealand, nor may any offering document or advertisement in relation to any offer of the Interests be distributed in New Zealand, other than in circumstances where there is no contravention of the Financial Markets Conduct Act 2013.

Philippines—THE STRATEGY AND/ OR ANY SECURITIES ASSOCIATED WITH THE STRATEGY BEING OFFERED OR SOLD HEREIN HAVE NOT BEEN REGISTERED WITH THE SECURITIES AND EXCHANGE COMMISSION UNDER THE SECURITIES REGULATION CODE. ANY FUTURE OFFER OR SALE OF THE STRATEGY AND/ OR ANY SECURITIES IS SUBJECT TO REGISTRATION REQUIREMENTS UNDER THE CODE, UNLESS SUCH OFFER OR SALE QUALIFIES AS AN EXEMPT TRANSACTION.

Singapore—Issued in Singapore by T. Rowe Price Singapore Private Ltd., No. 501 Orchard Rd, #10-02 Wheelock Place, Singapore 238880. T. Rowe Price Singapore Private Ltd. is licensed and regulated by the Monetary Authority of Singapore. For Institutional and Accredited Investors only.

South Africa—T. Rowe Price International Ltd (“TRPIL”) is an authorised financial services provider under the Financial Advisory and Intermediary Services Act, 2002 (FSP Licence Number 31935), authorised to provide “intermediary services” to South African investors.

Switzerland—Issued in Switzerland by T. Rowe Price (Switzerland) GmbH, Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified Investors only.

Taiwan—This does not provide investment advice or recommendations. Nothing in this material shall be considered a solicitation to buy, or an offer to sell, a security, or any other product or service, to any person in the Republic of China.

Thailand—This material has not been and will not be filed with or approved by the Securities Exchange Commission of Thailand or any other regulatory authority in Thailand. The material is provided solely to “institutional investors” as defined under relevant Thai laws and regulations. No distribution of this material to any member of the public in Thailand is permitted. Nothing in this material shall be considered a provision of service, or a solicitation to buy, or an offer to sell, a security, or any other product or service, to any person where such provision, offer, solicitation, purchase or sale would be unlawful under relevant Thai laws and regulations.

UK—This material is issued and approved by T. Rowe Price International Ltd, 60 Queen Victoria Street, London, EC4N 4TZ which is authorised and regulated by the UK Financial Conduct Authority. For Professional Clients only.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2020 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

ID0003313 (05/2020)

202005-1190298