April 2022 / INVESTMENT INSIGHTS

Global Asset Allocation Viewpoints

Our experts share perspective on market themes and regional trends, plus insights into current portfolio positioning.

Market Perspective

As of 31 March 2022

- Geopolitical risks and lingering pandemic impacts are weighing on global economic growth expectations while putting upward pressure on already elevated inflation.

- Despite moderating growth expectations, developed market central banks are expected to advance tightening policies to fend off decades- high inflation, with the US Federal Reserve leading with the most aggressive plans. The European Central Bank signaled an accelerated timeline to ending asset purchases and beginning rate hikes, while the Bank of Japan remains steadfast to policy, taking recent action to keep rates anchored.

- Emerging market central banks remain biased towards tightening to fend off inflation and defend currencies, while China policy continues moving in the opposite direction to stimulate growth.

- Key risks to global markets include escalating geopolitical concerns, persistent inflation near already high levels, central bank missteps and the impact of a COVID-19 outbreak in China on global growth and supply chains.

Portfolio Positioning

As of 31 March 2022

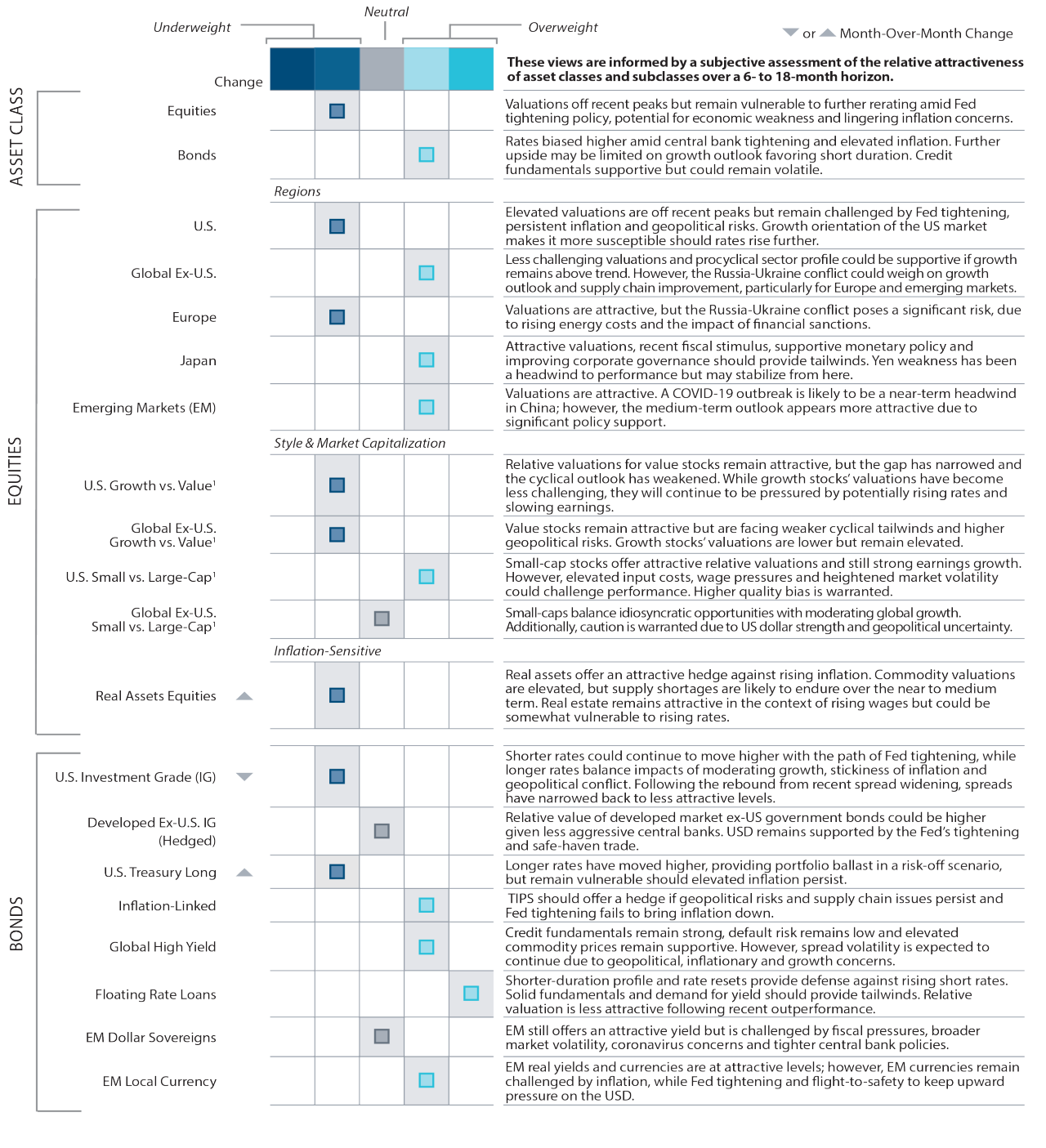

- While valuations are off recent peaks, we remain underweight equities given a moderating growth and earnings outlook amid an active Fed and lingering inflation concerns. Within fixed income, we remain overweight cash.

- Within equities, we added to real assets-related equities from global equities to provide a hedge should inflationary pressures persist longer than expected given heightened uncertainty.

- Within fixed income, we moderated our underweight to long-term US Treasuries following recent moves higher in rates to provide portfolio ballast in a risk-off scenario.

- We continue to favor shorter-duration and higher-yielding sectors through overweights to short-term TIPS, floating rate loans and high yield bonds supported by our still supportive outlook on fundamentals while keeping a cautious eye on liquidity amid higher volatility.

Market Themes

As of 31 March 2022

Beginning of the End?

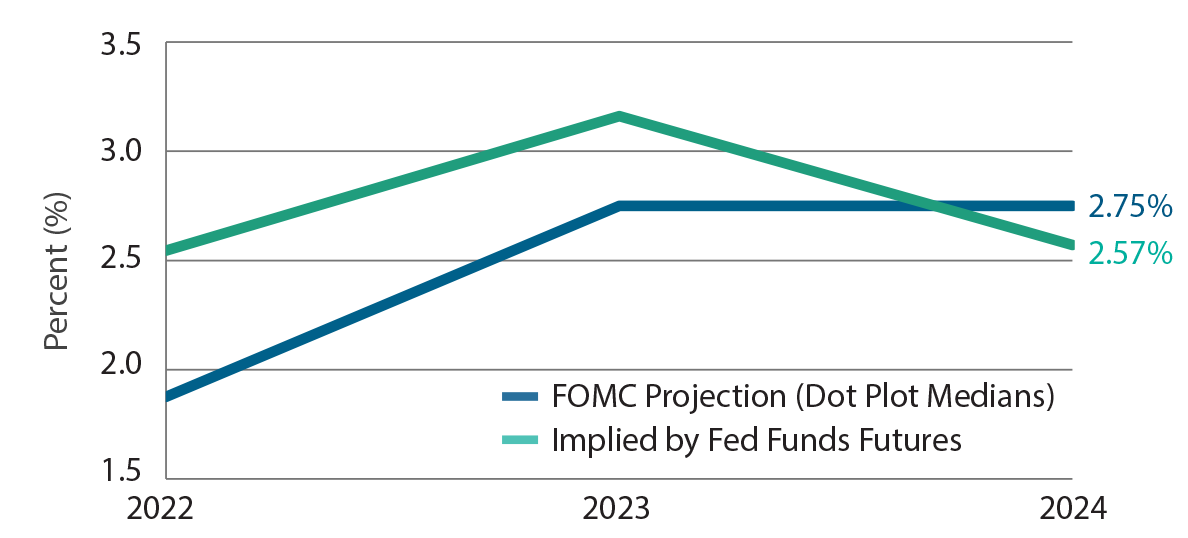

The more than four-decade bull market for bonds, supported by low inflation and declining rates, that provided a tailwind of price appreciation on top of income, may finally be coming to an end. For bond investors, this is a particularly precarious time given heightened rate sensitivity through extended duration levels and still low yields, providing little income to offset capital losses as rates rise. For the US Federal Reserve, which had enjoyed the luxury of acting aggressively when needed amid multiple crises while not stoking inflation, the tables have turned. Now due to exogenous factors impacting supply—the pandemic and the conflict in Ukraine—inflation has spiked higher, forcing the Fed into a battle that it hasn’t had to fight in decades. The market seems to agree that the Fed will remain steadfast, for now, in its battle against inflation over the course of the year. However, the market is saying the Fed could be lowering rates as soon as the end of next year, meaning bonds may not be out of favor for long.

Fed Funds Rate Projections

As of 31 March 2022

Source: Bloomberg Finance L.P.

For illustrative purposes only. Actual future outcomes may differ materially.

History Lessons

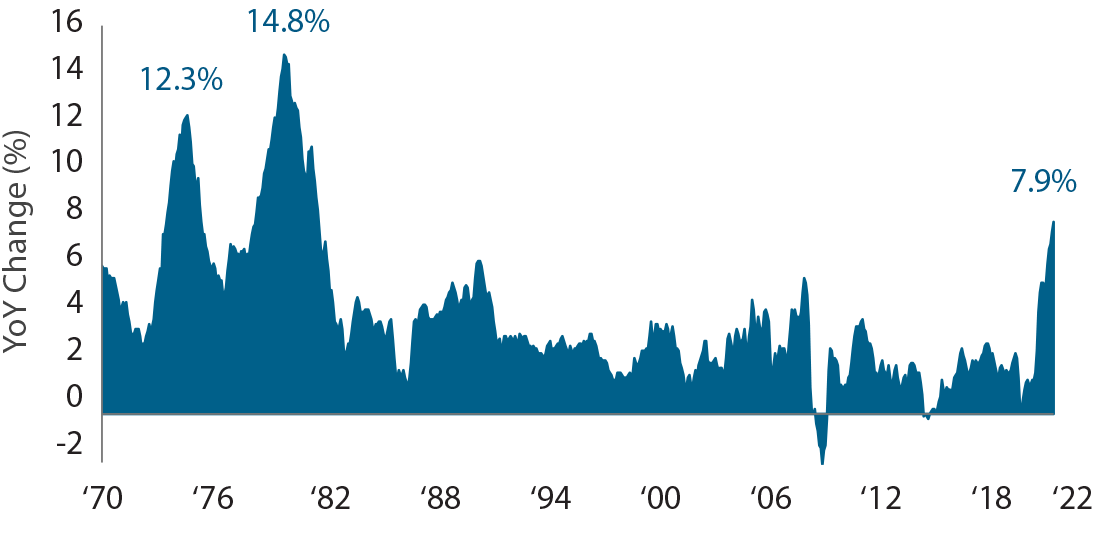

While the world has been battling to overcome the impacts of a global pandemic not seen in decades, we now face new, heightened challenges that may similarly have precedence with other periods in history. While coronavirus variants have extended supply chain issues and stoked higher inflation, expectations just a few months ago were that these issues would be transient. Unfortunately, the invasion of Ukraine in Europe, the likes not seen since the start of World War II in 1939, have exacerbated inflation risks and economic uncertainty. The narrative today has quickly turned to fears of “stagflation” with comparisons being made to the oil embargo of 1973 in the US that served as a catalyst for runaway inflation, unprecedented rate hikes and a recession. While the world is very different today and some of the challenges are distinct, history can repeat itself. So while stagflation is not our base case, the potential for tail risk events is heightened and warrants caution.

US Consumer Price Index (CPI) YoY

As of 31 March 2022

Source: Bloomberg Finance L.P.

For illustrative purposes only. Actual future outcomes may differ materially.

Regional Backdrop

As of 31 March 2022

| March | Positives | Negatives |

|---|---|---|

| United States |

|

|

| Europe |

|

|

| Developed Asia/Pacific |

|

|

| Emerging Markets |

|

|

Asset Allocation Committee Positioning

As of 31 March 2022

1For pairwise decisions in style & market capitalization, positioning within boxes represent positioning in the first mentioned asset class relative to the second asset class.

The asset classes across the equity and fixed income markets shown are represented in our Multi-Asset portfolios. Certain style & market capitalization asset classes are represented as pairwise decisions as part of our tactical asset allocation framework.

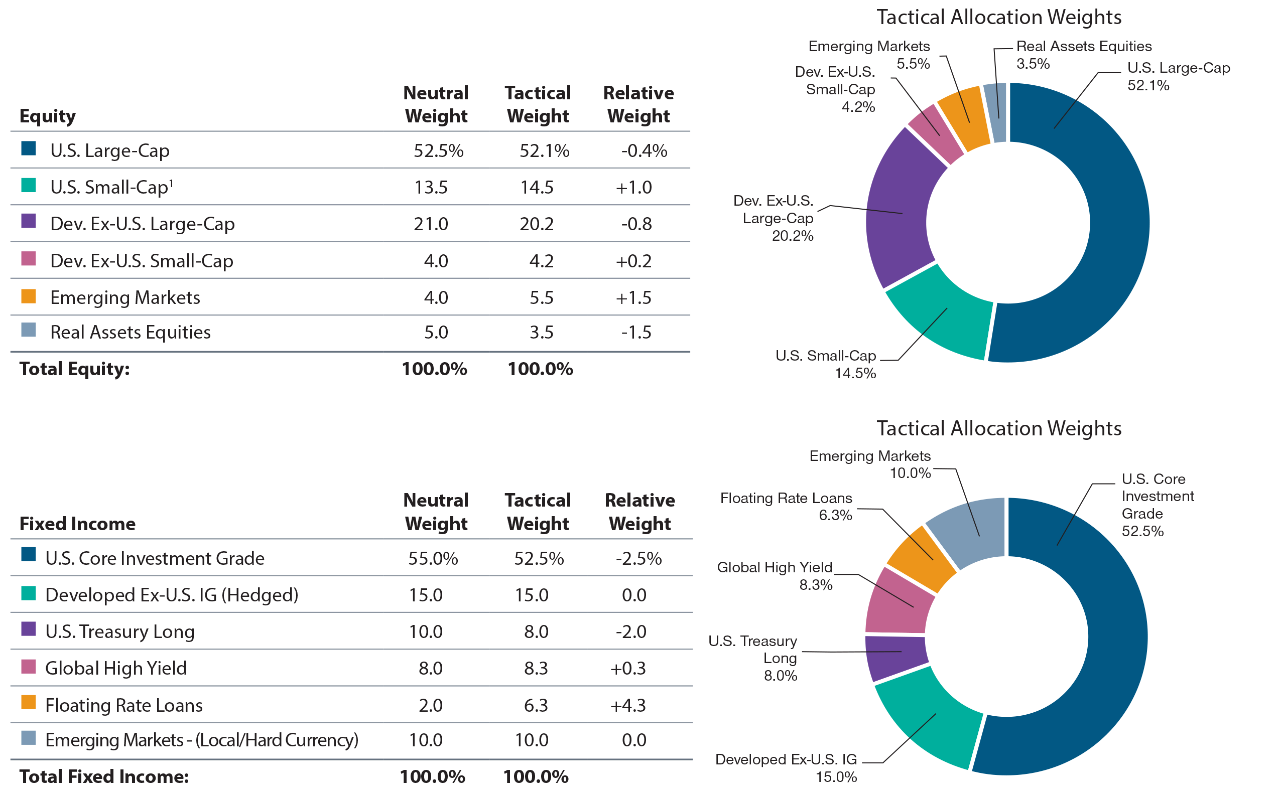

Portfolio Implementation

As of 31 March 2022

1 U.S. small-cap includes both small- and mid-cap allocations.

Source: T. Rowe Price. Unless otherwise stated, all market data are sourced from FactSet. Copyright 2022 FactSet. All Rights Reserved. These are subject to change without further notice. Figures may not total due to rounding.

Neutral equity portfolio weights representative of a U.S.-biased portfolio with a 70% U.S. and 30% international allocation; includes allocation to real assets equities. Core fixed income allocation representative of U.S.-biased portfolio with 55% allocation to U.S. investment grade.

Source: MSCI. MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendstion to make (or refrain from making) any kind of investment decision and may not be relied on as such.

“Bloomberg®” and Bloomberg Indices are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by T. Rowe Price. Bloomberg is not affiliated with T. Rowe Price, and Bloomberg does not approve, endorse, review, or recommend Global Asset Allocation Viewpoints. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to Global Asset Allocation Viewpoints.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is no guarantee or a reliable indicator of future results.. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.