September 2021 / INVESTMENT INSIGHTS

Innovations in Sustainability Are Reshaping the Future of Plastic

Balancing health and environmental concerns with the material’s utility

Key Insights

- Increasing regulatory requirements, evolving consumer preferences, and corporate action are combining to compel plastic production and packaging companies to adapt.

- The quest for sustainability is much broader than targeting simple elimination—innovation is changing the way plastic is used, substituted, and, crucially, disposed of.

- Integrating these dynamics into investment analysis includes exploring their influence on company behavior and actions being taken to mitigate risks or create opportunities.

Over just a few short decades, plastic in its many forms has become a ubiquitous material in modern life. But its many uses and economic and practical benefits have not come without costs. The chemical composition, resource usage, and inherent durability of plastic are major sustainability and health problems that the world urgently needs to solve.

Understanding the magnitude of the problem, both in terms of the environmental impact, as well as concerns relating to human health, is crucial. Yet, solutions also need to balance the utility of the material. Plastic inextricably serves modern industries and benefits consumers globally. Paradoxically, it also remains the best solution to other sustainability‑related problems, such as reducing food waste, lowering packaging weight, enabling better hygiene, and improving the life span of building materials.

From an investment perspective, we believe the sustainability debate should focus on the reshaping of the sector—how innovation is changing the way plastic is used, substituted, and modified to be less damaging and, crucially, how it is ultimately disposed of. In the single‑use plastics space, innovation strategies promoting elimination, reuse, and circulation of plastic are key areas of the industry’s response to rising consumer and regulatory pressures.

An Overview of the Plastic Problem

Plastic use has grown rapidly since the 1970s as consumers and industry have capitalized on the material’s key attributes—malleable, lightweight, durable, and cheap. However, the production and use of plastic has long underestimated the core problem of its end‑of‑life burden.

Most plastics have a very short life span, often less than one year, with up to 95% of plastic packaging material lost to the economy after its first use (Ellen MacArthur Foundation). Nearly 13 million tons of plastic waste finds its way into the world’s oceans each year, while its complex nature and low margins for recycling see most single‑use plastic waste buried in a landfill or incinerated. Plastics pollute vital ecosystems and infiltrate human food chains. Research by the World Wildlife Fund and University of Newcastle in Australia in 2019 stated that the average person consumes about five grams of plastic per week (the equivalent of a credit card).

Taking up to 450 years to biodegrade, plastics’ environmental impact is therefore significant when not disposed of properly. It’s easy to understand how plastic packaging has become the scourge of the circular, reusable economy—placing it squarely in the crosshairs of increasingly environmentally conscious consumers and government regulators alike.

Catalysts of Change—Governments and Consumers Compel a Rethink

Unsurprisingly, regulators and consumers are demanding action. Many governments around the world are implementing new regulations and committing to actionable time frames to reduce the impact of single‑use plastics. This includes some of the world’s largest producers and consumers of plastic products. Regulatory action typically targets the reduction of single‑use plastics and promotes increased recycling or innovation toward alternative solutions. A summary of key regulatory initiatives is below.

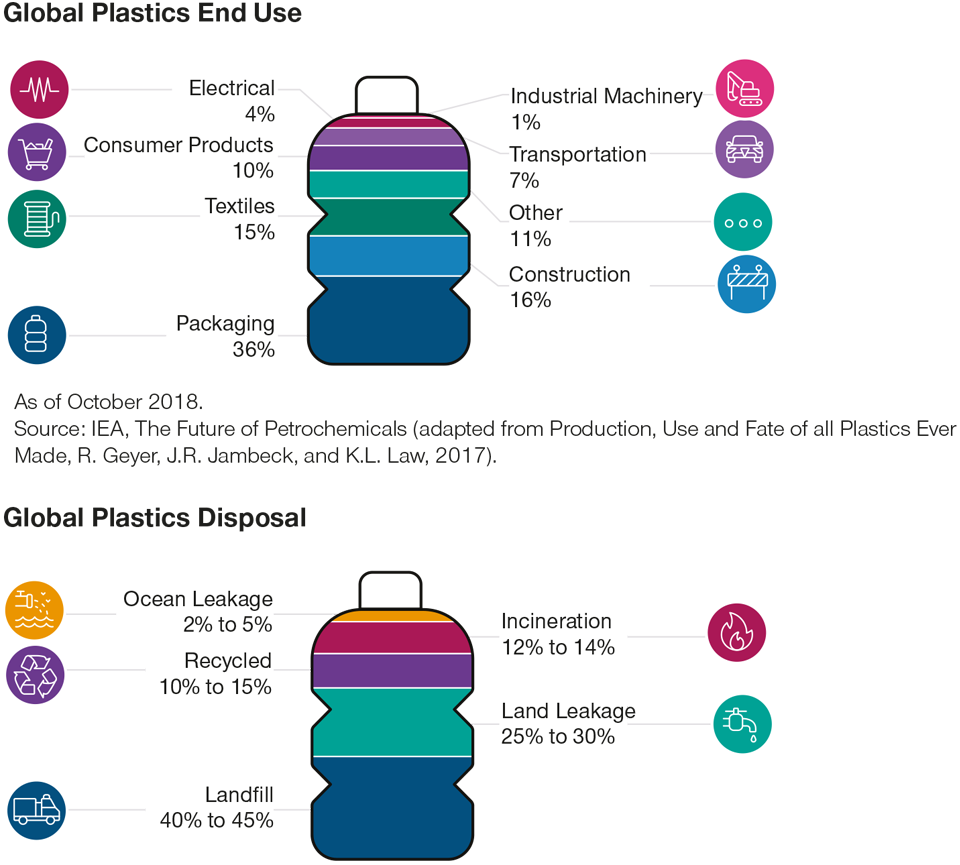

Global Plastics End Use and Ultimate Disposal

(Fig. 1) Most plastic continues to reflect a linear, single‑use economy

Global Plastics End Use

As of December 2018.

Source: The New Plastics Economy, Ellen MacArthur Foundation, 2018.

Consumers are another powerful impetus for change. Half of the Household and Personal Care (HPC) companies in the MSCI All Countries World Index (ACWI), for example, have indicated that consumer concern about the environmental footprint of their purchases has been a motivation to improve product sustainability. According to a Kantar Survey,1 global consumers rank plastic waste as their second biggest concern, after climate change (survey of over 80,000 individuals in 19 countries). Kantar also found that 20% of global consumers in 2020 were actively engaged in reducing their contribution to plastic waste, an increase of 4% from 2019.

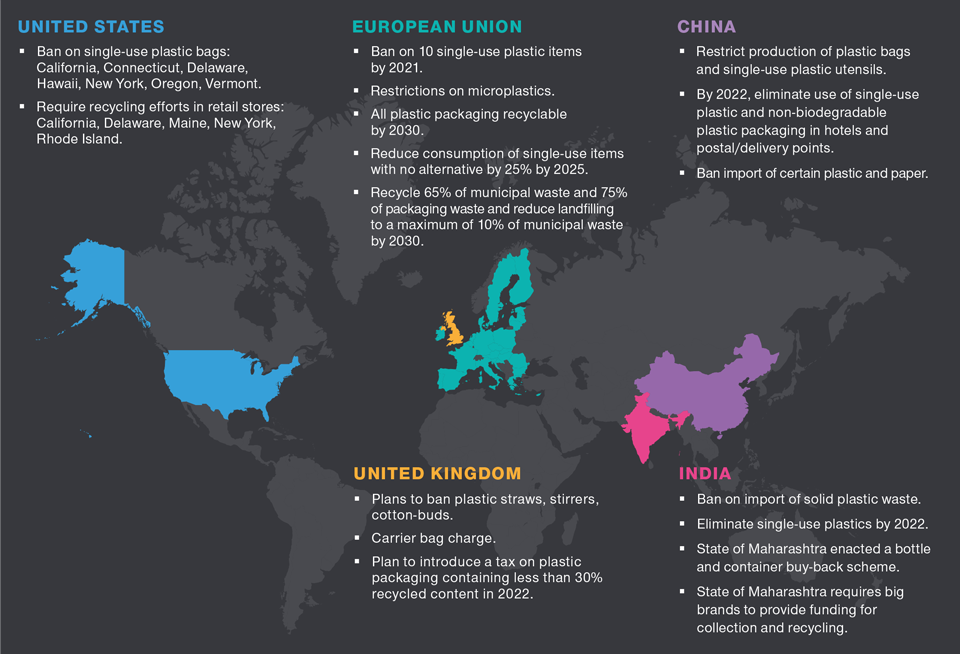

Global Governments Are Targeting Single‑Use Plastics

(Fig. 2) For their part, many governments around the world are taking action to reduce single‑use plastics, implementing new regulations and, importantly, committing to actionable time frames. Encouragingly, some of the world’s largest producers and consumers of plastic products are setting the example, putting in place essential regulatory actions and initiatives aimed at reducing the prevalence of single‑use plastics, while encouraging increased recycling or alternative products.

Data collection and analysis by T. Rowe Price. As of December 2020.

The Industry Response—How Innovation Is Reshaping the Future of Plastics

Given the various regulatory, consumer, and corporate pressures, environmental, social, and governance considerations are set to significantly reshape the packaging industry in developed countries over the coming years. Single‑use plastics are a principal area of focus, directly challenged by alternative substitutes (paper, aluminium, glass) as well as innovative new materials like bioplastics.

Since plastic offers many benefits and widespread practical applications, a focus on simple elimination as a response to regulatory and consumer pressures is unrealistic. A range of solutions are in play—and our research seeks to identify how companies are working to adapt to the risks and opportunities associated with the need for change. Within the HPC sector, historically a significant producer and user of single‑use plastics (particularly for packaging), we have identified three key classifications of industry response—with innovations that focus on elimination, reuse, or improved circulation.

Many leading companies within the HPC industry expect to complete full overhauls of their packaging between 2025 and 2030. Businesses have responded to changing consumer preferences and expectations by switching to alternative materials such as aluminum or paper. Meanwhile, others have adopted new policies, like eliminating plastic bags entirely, as they simultaneously make other changes to their products or supply chains.

Plastic elimination efforts typically involve removing packaging components that are not essential for containment or protection. Though most companies have not disclosed specific packaging elimination targets, many of those we analyzed offer examples of packaging optimization. For example, 15 of the 36 HPC companies in the MSCI ACWI have mentioned eliminating unnecessary tertiary packaging such as outer packaging, plastic film that encases an outer package, and secondary plastic wrapping in multipack items. Some companies are also finding innovative solutions that remove packaging components like plastic pour spouts, labels, and seals. Light weighting is another common trend; over 50% of HPC companies in the MSCI ACWI have significantly reduced plastic consumption by reducing the weight and volume of their products.

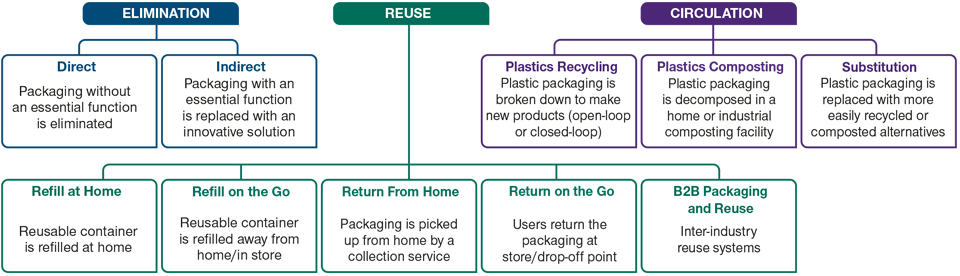

Plastic-Intensive Industries Are Responding in Different Ways

(Fig. 3) Within the HPC sector, innovations are broadly focused on three different outcomes

Source: Original diagram sourced from the Ellen MacArthur Foundation website, September 2021. The diagram is reproduced by T. Rowe Price specifically for inclusion in this article, and its use does not reflect the views of the Ellen MacArthur Foundation, nor does it reflect or imply the Foundation’s endorsement.

In terms of reuse strategies, 18 HPC companies in the MSCI ASCWI now offer refillable products, which can allow consumers to refill at home. Another common reuse strategy is a “return from home” subscription service that distributes and cleans reusable containers.

While some businesses can devise approaches to eliminate or reuse plastic, it is not possible for many others. In the grocery sector, for example, food supply chains are dependent on plastic packaging to maintain product freshness and prevent waste—in themselves, important components of sustainability efforts. The solution here is improved packaging circulation, which entails innovation in:

- Making packaging more reusable, recyclable, or compostable

- Incorporating recycled material in their packaging

- Reducing virgin plastic2 and fiber in packaging

Our analysis of the HPC sector indicates that, of the three innovation approaches, most progress has been made on improving material circulation. A high percentage of HPC companies are actively engaged in efforts to make packaging more reusable, recyclable, or compostable, with a view to achieving 100% circulation as the industry standard by 2025. It is encouraging that companies are beginning to understand the benefits that these practices can bring for the environment and the bottom line. Recycling more plastic can reduce material input costs, while environmentally conscious consumers are more likely to support companies making the shift.

It is not only the HPC companies where the potential benefits of reduced plastic production/usage can be observed. Suppliers that offer sustainable alternatives to virgin plastic packaging, such as paper/fiber‑based packaging companies and aluminum cans, will also likely see an increase in demand. Meanwhile, ongoing consumer pressure and government regulation to decrease plastic use should also lead to multiple business opportunities associated with the tasks of collecting, sorting, and recycling plastic.

In More Difficult Areas, Challenges Remain

Despite evidence of positive initiatives to better manage the plastic problem, companies can be less forthcoming when disclosing information on some “harder to achieve” objectives, such as the recycled content and virgin material reduction goals for their packaging. Including recycled plastic in product packaging is a more difficult task than simply making packaging reusable or compostable. The collection resources and infrastructure needed to recycle plastic more efficiently is currently lacking, while low oil prices also make recycled plastic less economically appealing.

These hurdles can also open companies up to potential “greenwashing” of their recycling credentials. For this reason, raw material inputs, and a specific focus on recycled material usage, are key data metrics that are included in our Responsible Investing Indicator Model (RIIM) company analysis, in aiming to ensure that corporate claims about the recycled content of products are accurate and up to date.

A Radical Reshaping Is Underway

How the world deals with the problem of plastic waste is of increasing concern for society, companies, our clients—and our investment teams. The imperative has never been greater. The key challenge is for industry to devise solutions to address the sustainability problem while balancing the practicality of plastic across vast areas of modern industry and society.

We expect the single‑use plastics space to be radically reshaped in the coming decade as companies increasingly develop and use alternative materials (paper, aluminum, glass, etc.); innovate toward better, less‑damaging plastics (bioplastics, etc.); and find ways to use less packaging material altogether. At a company level, many businesses are recognizing this imperative for change and are adjusting to a new and more sustainable paradigm. Industries and companies that address regulatory and consumer pressures through innovation should be best placed to prosper.

As investment professionals, we seek to integrate these dynamics into our analysis, working to evaluate how they are influencing company behavior, and what actions are being taken to mitigate risks or create opportunities. In doing so, we hope to identify those companies that are best placed to adapt to the necessity for long‑term, sustainable solutions to plastic use.

Factoring Plastics Sustainability Into T. Rowe Price’s Responsible Investing Indicator Model (RIIM)

T. Rowe Price’s RIIM incorporates a range of factors against which companies are scored and measured on their plastics sustainability. The model utilizes both internal and external data sources to help ensure a comprehensive and holistic assessment of each business. Key metrics include:

Raw Materials

- Recycled material usage

- Packaging targets

- Packaging performance data

Waste

- Waste recycled

General Operations

- Eco-design

- Green logistics programs

Product Sustainability

- Sustainable products and services

- Product stewardship programs

- Environmental impact of products

- Chemical safety of product

- Chemical “clean-tech” exposure

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

September 2021 / INVESTMENT INSIGHTS

September 2021 / INVESTMENT INSIGHTS