May 2022 / SEARCH FOR YIELD

Not All Currencies Are Made Equal, So Don’t Treat Them as Such

Selective currency hedging may boost yields and add stability.

Investors in global fixed income markets typically hedge their currency exposure to reduce volatility. In some cases, however, selected unhedged currency exposures can bring additional yield and even help to anchor a portfolio during volatile periods. This suggests that investors may benefit from adopting a more nuanced approach to currency hedging than is typically practiced.

In this paper, the third in a series of articles on the search for yield, we focus on how a selective approach to hedging overseas bond exposure may help to boost yields while also reducing portfolio volatility.

As we noted in an earlier blog post, home‑country government bonds are often seen as the least risky building block for multi‑asset portfolios. As the yields on many government bonds have increased sharply in recent months, investors looking for income are again finding a place for such assets in their portfolios. However, heavy exposure to home‑country bonds brings risks, particularly if the sovereign creditworthiness of the home country comes under scrutiny—as has happened numerous times this century, including some large developed eurozone countries. Investing in overseas sovereign bond markets can, therefore, improve diversification and boost the “shock absorption” qualities in a portfolio.

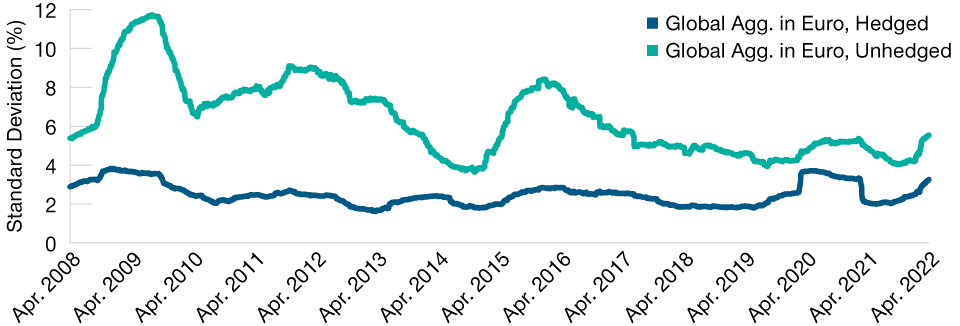

Holding overseas bonds on an unhedged basis can add significantly to the volatility of fixed income exposures, however. This can be seen by observing the one-year rolling volatility of the Bloomberg Global Aggregate Index for a euro investor, on both a hedged and unhedged basis, over the last 15 years (Figure 1).

Hedging Overseas Bond Exposure Typically Reduces Volatility

(Fig. 1) Comparing hedged and unhedged allocations to the Global Agg.

As of April 22, 2022.

Past performance is not a reliable indicator of future performance.

Rolling 1-year annualized volatility, based on daily observations.

Source: Bloomberg Finance L.P. Analysis by T. Rowe Price. Global Aggregate: Bloomberg Global Aggregate Index hedged to euro and Bloomberg Global Aggregate Index in EUR, unhedged to euro.

The more volatile nature of an unhedged holding of even such high‑quality bonds can be clearly seen, with particular spikes in periods of turbulence such as the global financial crisis and the eurozone crisis. Over the entire period, the average one‑year rolling volatility was 2.5% p.a. for a hedged investor but well over double that, at 6.4% p.a., for an unhedged investor.

This appears to suggest that the decision to hedge such fixed income exposure is a straightforward one. Yet, while foreign currency exposure generally adds to a portfolio’s expected volatility, selected unhedged exposures to overseas assets can, in some instances, act as an additional anchor for portfolios in periods of turbulence. During three of the most volatile episodes in markets over the past 15 years, for example, eurozone investors who allocated to the Bloomberg Global Aggregate Index would have generated stronger returns if they left their currency exposure unhedged (Figure 2).

In Volatile Times, Hedging Can Be Less Effective

(Fig. 2) Unhedged currencies can outperform during turbulent periods

As of March 31, 2022.

Past performance is not a reliable indicator of future performance.

Source: Bloomberg Finance L.P. Analysis by T. Rowe Price. The table shows the performance of the Bloomberg Global Aggregate Index for a euro investor on a hedged and an unhedged basis.

What drove this pattern of returns? Well, not all currencies are created equal. Some, such as the U.S. dollar, are often seen as a bolthole in times of market stress (this has again been very evident during the events of recent months). When investors are very fearful about the return outlook for a wide range of markets, U.S. assets are frequently viewed as the safest place to be. This drives up demand for U.S. dollars from investors worldwide. Other currencies, including the Japanese yen and Swiss franc, have played a similar role historically, although in some cases their efficacy can vary from crisis to crisis (Figure 3).

Major Currencies Can Serve as a Bolthole During Periods of Stress

(Fig. 3) The U.S. dollar has been the leading “safe‑haven” currency

As of March 31, 2022.

Past performance is not a reliable indicator of future performance.

Sources: Bloomberg Finance L.P. Shows the performance of Deutsche Bank Trade Weighted Index for each respective currency. Analysis by T. Rowe Price.

An additional benefit for euro investors investing for income is that yields on overseas government bonds may be higher on an unhedged basis, especially as the European Central Bank moves more slowly to unwind easy monetary policy than other key central banks such as the U.S. Federal Reserve, the Bank of England, and the Bank of Canada. We believe that fixed income investors should review their hedging approach to major overseas currencies within their allocations on a case‑by‑case basis. This will allow them to judge where potential diversification benefits from “safe havens” will offset the additional portfolio volatility such exposures bring.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is no guarantee or a reliable indicator of future results.. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.