December 2021 / GLOBAL MARKET OUTLOOK

Asia ex‑Japan 2022 Market Outlook

Risk/reward looks attractive for Asia ex‑Japan equities.

Key Insights

- We remain constructive on the longer‑term economic outlook for Asia ex‑Japan. Fiscal and current account balances are supportive to equities and currencies.

- Our view on China is critical for Asia ex‑Japan. We are impressed by the depth and dynamism of a Chinese stock market that is too big for investors to ignore.

- We believe risk/reward looks attractive for Asia ex‑Japan equities relative to other regions. Regional growth stocks are once again attractively priced.

Asia ex‑Japan economies appear well positioned to rebound in 2022 following the contagious delta coronavirus outbreak and slower progress on vaccination in some countries, notably in Southeast Asia. Supply chain disruptions, which have proven a headwind to global economic recovery, are expected to be temporary. Some Asian countries—such as Singapore, Thailand, and South Korea—are currently easing restrictions and opening their borders. Asian tourism may be slow to catch up, with Chinese tourists absent due to travel restrictions and long‑haul visitors only returning gradually.

Inflation: Less of a Risk for Asia

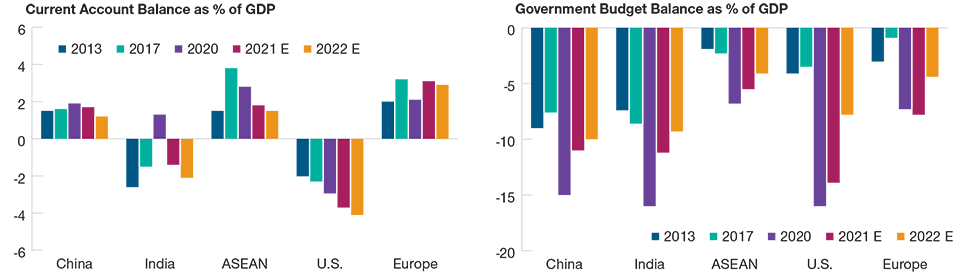

We remain constructive on the longer‑term economic outlook for Asia ex‑Japan. Fiscal and current account balances remain supportive to both equities and currencies (Figure 1). More stable currencies than in the past have contributed to the relatively benign regional inflation outlook for 2022. Current inflation pressures in many Asian countries are more driven by temporary supply shocks in food and energy than by strong domestic demand, which means regional central banks are less likely to respond with monetary tightening. The more benign inflation outlook for Asia ex‑Japan reflects less fiscal stimulus to fight the pandemic than in developed economies in 2020 and growth that fell further below trend, producing downward pressure on inflation.

Asia Ex-Japan in a Fundamentally Stronger Position Today

(Fig. 1) Asia ex-Japan fundamentals on a steady recovery path

As of September 30, 2021.

Source: Morgan Stanley. E=estimates.

China View Is Critical for Asia ex‑Japan

We believe we are nearing the end of the current regulatory cycle in China. We recognize that China undergoes cycles of policy changes and that the difficulty lies in predicting the timing and the means by which they will enforce policy shifts. The new regulations in 2021 fall within the broad policy framework that China has communicated clearly enough in recent years. Chinese President Xi Jinping’s social goals focus on three pillars: anticorruption, environmental protection, and social equality.

While the focus of many foreign investors has been on China’s unexpectedly severe regulatory clampdown and its near‑term negative impact, we remain impressed by the dynamism and depth of the large Chinese stock market that is too big to ignore. With a high rate of IPOs, new Chinese businesses continue to impress and climb the innovation curve, finding ways to compete with the established players. Change is really the only constant in China. It provides bottom‑up investors with a stream of good idiosyncratic investment ideas.

We think that the new regulations may trigger a “reset” or consolidation in the affected industries, potentially creating new opportunities. We do not believe the regulatory clampdown has rendered Chinese stocks “uninvestable.” Beijing does not wish to derail the future growth of the affected sectors but, rather, seeks to bring more balance to the ecosystem and with it greater social stability. Government policies to limit monopolistic behavior, improve labor rights and the quality of living, respond to demographic changes, and protect data privacy are hardly unique to China but are also pursued by governments in many other countries.

The problem for overseas investors is that the new regulations most heavily affected a relatively small number of “new economy” growth stocks. They had become overvalued, partly due to concentrated buying by many overseas funds that focus heavily on the benchmark index. The result was falls of bear market proportions in a relatively small number of expensive stocks, many of which were listed overseas in the U.S. or offshore in Hong Kong. A few months later and broad market stability has been restored, making the summer’s sharp but narrow correction appear less significant with the benefit of hindsight.

Investment Outlook for 2022

We believe that for Asia ex‑Japan, some emerging long‑term trends such as the greater focus on environmental protection or industrial infrastructure upgrading can help to provide guidance in seeking attractive bottom‑up investment opportunities.

In all, we have identified seven key long‑term trends to monitor:

- Trend 1: China’s greater focus on environmental protection

- Trend 2: Industrial infrastructure upgrading

- Trend 3: Demographic dividend (dual‑income no kids power of spending (DINKs))

- Trend 4: Chinese households diversifying their savings

- Trend 5: China’s changing internet ecosystem

- Trend 6: Import substitution

- Trend 7: Rising intraregional trade

Many of these trends are closely related to or intertwined with China’s big policy shift a few years ago to the “Dual Circulation” concept, which gives more emphasis to the domestic economy, with the need to stimulate innovation in all industries (not just the internet or “New Economy”), the potential to create higher‑earning employment, and using the vast domestic market to gain scale and global competitiveness.

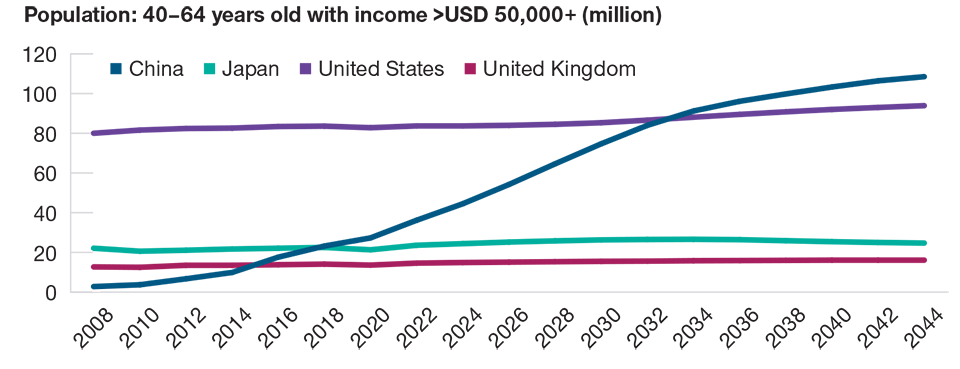

Trend 3 above is a positive demographic dividend for China and may come as a surprise (Figure 2). The number of DINKs in China is estimated to quadruple in the next decade, potentially reaching the U.S. level. We believe that the investment implications for consumption patterns are considerable, with increased spending on premium products and services, including on lifestyle, health, leisure, and wealth management services. This positive boost to consumption is expected to make itself felt before the negative impact of China’s aging demographics take over.

China Demographics Surprise—Dual Income, No Kids

(Fig. 2) China’s DINKs may quadruple by 2030, reaching the U.S. level

As of December 31, 2017. All subsequent data represents estimates.

Sources: HSBC/Haver Analytics, Morgan Stanley. Most recent data available. Actual outcomes may differ materially from estimates.

Turning to earnings, the third‑quarter earnings season in Asia has been rather mixed, with 50% of companies reporting that they beat consensus earnings estimates. Sustaining margins may be an issue for earnings in 2022. On a positive note, the analyst consensus projects a recovery in the contribution to regional earnings growth from China’s internet sector following a lackluster, regulation‑hit 2021. Over the past six months, all sectors except real estate, consumer discretionary, and communication services have seen positive growth in 12‑month forward earnings estimates.

Following the correction in China, we believe risk/reward is looking attractive for Asia ex‑Japan markets relative to other markets. Regional growth stocks, for example, are attractively priced once again. In terms of valuations, we believe that those of many high‑quality growth businesses in Asia ex‑Japan remain in line with their historical levels. However, we still see large valuation discrepancies in certain areas, such as stocks expected to benefit from the transition to “green” energy.

Technology‑heavy South Korea has recently underperformed as the global electronics cycle slowed and third‑quarter gross domestic product (GDP) data disappointed when the economy only grew 0.3% year‑on‑year, a much slower‑than‑expected pace. Weak private consumption, which accounts for one‑half of South Korea’s GDP, and a decline in construction and facility investments more than offset robust exports.

India, the best‑performing market in the first to third quarters of 2021, has retreated recently amid investor concerns about steep valuations and the central bank signaling liquidity normalization. Expectations that corporate profits will rebound in the coming quarters as the coronavirus situation improves may have already been priced in, while higher energy prices are expected to hurt Indian companies’ margins. India has pulled through the second wave of the coronavirus and corporate earnings projections appear decent, supported by the recovery in real estate, consumption, and information technology services. However, valuations are broadly demanding, and inflation will be a key risk to monitor in 2022.

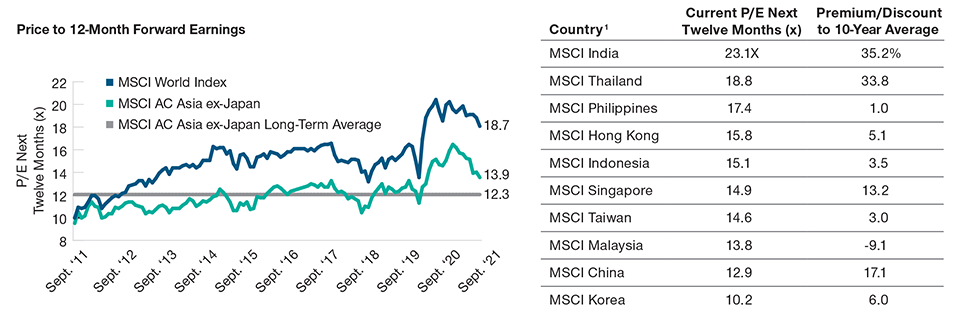

Asia ex-Japan Appears Cheap Relative to MSCI World (Developed Markets)

(Fig. 3) Global markets rerated relative to Asia ex-Japan on expected

earnings rebound

As of September 30, 2021.

1 Relevant MSCI country indices were used to represent each country.

Source: Financial data and analytics provider FactSet. Copyright 2021 FactSet. All Rights Reserved.

Please see Additional Disclosure for information about this MSCI information. Actual future outcomes may differ materially from expectations.

Apart from further unexpected policy shifts in China, other key regional risks for Asia ex‑Japan in 2022 include a new coronavirus variant that is not responsive to current vaccines, a mistake by the central banks that tighten monetary policy too soon, further geopolitical tensions between the U.S. and China, and a more severe‑than‑expected property‑led economic slowdown in China.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

December 2021 / INVESTMENT INSIGHTS