March 2021 / MARKET OUTLOOK

Global Asset Allocation: March Insights

Discover the latest global market themes

MARKET INSIGHTS

As of 28 February 2021

Your Move, Mr. Powell?

After years of muted inflation, investors are becoming concerned as a massive amount of pent-up demand is expected to be unleashed as the economy reemerges in the coming months, bringing higher price pressures. The excess savings that consumers have accumulated over the past year, plus an additional near USD 1.9 trillion fiscal package on the way, could also lead to demand outstripping existing supply, placing upward pressure on prices. As inflation expectations have already breached the 2% threshold, investors are beginning to question the resolve of the Fed to hold monetary stimulus at current levels. So far, Fed Chairman Jerome Powell has repeatedly reiterated a dovish stance, stating that price pressures are likely to be mild and temporary. Until unemployment levels make significant strides toward the Fed’s goals, an easy monetary policy appears to be staying in place. Currently, the bond market’s recent rise in yields may already be containing inflation for the Fed; however, if rates continue to increase, the Fed may need to step in and take action to rein in longer-term rates.

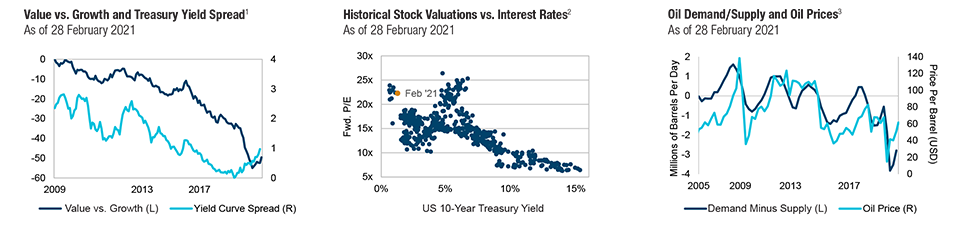

Yield Scare

The recent sharp spike in yields is scaring equity investors, who, this time last year, saw the 10-year Treasury yield dip below 1% for the first time. Although rising rates are often a sign of healthy economic growth and should benefit cyclical sectors, such as financials, energy and industrials, they may spell trouble for higher-growth sectors, like technology, that have benefited in an environment of scarce growth and low rates. The high-flying technology sector’s extended valuations may become harder to justify amid rising rates. More broadly higher rates could impact borrowing costs for companies and weigh on certain sectors, such as housing, that have benefited from low rates. While historically we are far from yield levels that have negatively impacted stocks, what is unique today is that we are starting from a level of zero policy rates, high-equity valuation levels and the market dominance of technology and related sectors. A further rate rise could challenge broad markets as investors continue to rotate away from higher‑growth stocks, such as technology, into more cyclically oriented sectors.

Pedal to the Metal

Commodity markets have climbed to their highest level since 2018 on hopes for a rebound in demand as the global economy reopens and travel resumes later this year. After collapsing in 2020 amid the pandemic-driven shock, oil prices have reached recent highs as demand has gradually recovered, and supply has not kept pace, partially due to supply cut agreements from OPEC+. Industrial metals such as copper have also been on a tear, further supported by a shift in focus toward renewable energy and electric vehicle technology. Some investors are suggesting that the commodity rally may have more durability as the worldwide push for cleaner, greener energy could keep upward pressure on commodities such as copper, platinum and lithium for years to come, many with limited supply. After years of underperformance, a new commodity supercycle could be emerging with cyclical and secular trends finally in their favour, particularly among industrial metals. As inflation expectations continue to rise amid evidence of increasing demand, real assets equities could be poised to outperform broader markets.

Past performance is not a reliable indicator of future performance.

1 Value represented by Russell 3000 Value Index. Growth represented by Russell 3000 Growth Index. Treasury yield spread represents the difference between the US 10-year and 2-year Treasury yields.

2 Chart represented by monthly data from 31 December 1978 to 28 February 2021. Fwd. P/E represented by the Russell 1000 Index.

3 Demand Minus Supply is based on 12‑month averages. Oil price is represented by brent crude oil prices.Sources: OECD/Haver Analytics, London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”) (see Additional Disclosure). T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

For a region-by-region overview, see the full report (PDF).

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.