November 2020 / INVESTMENT INSIGHTS

The Eurozone’s Recovery Will Take a Break This Winter

The currency union faces four possible growth scenarios

Key Insights

- Targeted (intelligent) lockdowns mean that 0% eurozone growth this winter is increasingly plausible.

- Any deviation from the V‑shaped recovery projection should be met with further support from national governments and the European Central Bank.

- This would keep eurozone deficit levels elevated for longer and likely weaken the euro against the dollar but would keep spreads relatively stable.

The path of the eurozone’s economic recovery remains uncertain as a second wave of coronavirus cases is occurring in many countries. A number of scenarios for the recovery remain possible, including a damaging double‑dip recession. Which of these scenarios plays out will depend on the severity of any further outbreaks of the virus—and how governments choose to respond to them.

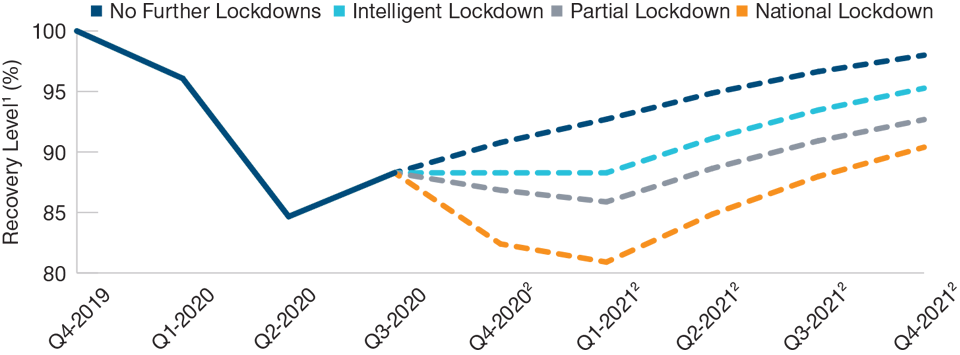

Further Lockdowns Would Hit the Recovery

(Fig. 1) Four scenarios for eurozone real GDP growth

As of September 30, 2020.

1 Percentage of recovery to pre-coronavirus pandemic level.

2 Estimate.

Source: European Commission/Haver Analytics; T. Rowe Price calculations.

Economists do not have the scientific expertise to credibly forecast virus spread and mortality, which means it is easier to come up with scenarios, but difficult to assign credible probabilities of these scenarios occurring. Our current view is that the highly-targeted (intelligent) lockdown approach could lead to 0% growth in the fourth quarter of 2020 and the first quarter of 2021, but the situation is fluid and forecasts may change. Past recessions also provide little guidance on what to expect. Historically, deep recessions have been followed by V-shaped recoveries—and the leanness of consumer balance sheets before this recession would perhaps suggest that this might occur this time. However, the main cause of the current recession—a contagious virus—cannot be addressed by economic policy alone. A second large shock in the form of more widespread government restrictions and/or major hits to economic confidence due to an outbreak of the virus is plausible.

If the virus spreads at an exponentially higher rate, the path of least resistance will be the intelligent lockdown approach. By imposing restrictions on certain activities, such as social consumption (restaurants and bars) and mixing of households, but leaving businesses open and avoiding stay-at-home orders, this approach should support some degree of virus control with the least economic hit. In Europe, Italy and Germany have applied this approach in response to renewed outbreaks. At the time of this writing, France, Spain, and the UK are also embarking on this approach.

What remains to be seen is whether the intelligent lockdown approach will be enough to bring virus cases back down once they reach high levels. While the total number of cases was rising slowly in August and September, the number of regions reporting significant outbreak rose to 60% in Germany. The intelligent lockdown approach helped to bring the fraction of regions reporting a large outbreak to 10% to 20%. However, it is unclear if this approach can reduce spread if coronavirus cases continue rising exponentially.

While the intelligent lockdown approach is the most probable approach to containment, given the strong possibility of further outbreaks and unpredictable responses from governments, businesses, and consumers, a double‑dip recession remains possible.

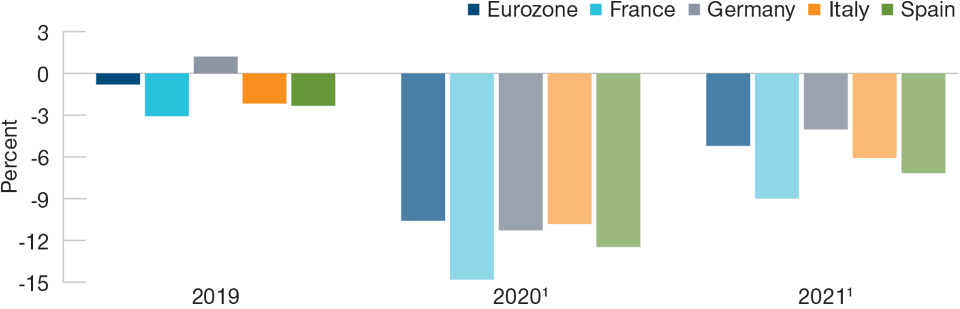

Deficits Expected to Shrink if Recovery Remains on Track

(Fig. 2) Germany is set to lead the return to balanced budgets

As of September 30, 2020.

Deficits are measured as a percentage of GDP.

1 Estimate.

Source: European Commission/Haver Analytics; and T. Rowe Price calculations.

Further ECB Support Is Very Likely if the Outlook Deteriorates

If there is any deviation from its baseline forecast of a V‑shaped recovery, the European Central Bank (ECB) will likely stick with what works: more monetary stimulus, most likely in the form of an expansion of the Pandemic Emergency Purchase Programme (PEPP). Based on their experiences in March, ECB policymakers know that acting fast works and that the flexibility embedded within the PEPP was effective in stabilizing financial markets. Even the least severe intelligent lockdown scenario is a significant deviation from the ECB’s baseline projection that would likely see an expansion of PEPP by EUR 500 billion; in the case of a double‑dip recession, the ECB would most likely expand PEPP by at least EUR 750 billion.

The ECB does, of course, have other tools at its disposal, including negative interest rates and yield curve control (YCC). However, it is likely to wait for markets to normalize and bank balance sheets to recover before deploying negative rates again. Implementing YCC in the eurozone would be a very politically charged move and, as such, is probably a last resort. Therefore, the ECB is likely to respond to any forecast changes by using a tool that it knows will work and extending the PEPP to the end of 2021.

The European Union (EU) may be more constrained in its ability to respond to a worsening outlook. In response to the first wave of the coronavirus, EU leaders approved a EUR 750 billion recovery fund, including EUR 390 billion in grants to countries that were most affected by the virus. The debt for this spending will be shared by all EU member states, and as such, this will be the first time that some members have benefited more than others from commonly borrowed funds—a possible first step toward fiscal integration for the bloc.

However, the political bar to additional aid is high. The recovery fund was made possible by the size of the unexpected pandemic shock, Angela Merkel’s EU presidency, the need to demonstrate solidarity with the worst‑affected countries, and budget rebates for northern European countries. At present, countries are working on the challenging task to pass the relevant legislation in all 27 EU member state national Parliaments. Unless deaths across Europe begin to rise at the same pace as in March 2020, high‑level political agreement for more stimulus is probably unlikely for now.

It is possible that the European Commission would seek to increase loans available for furlough schemes via the Support to mitigate Unemployment Risks in an Emergency (SURE) program. Among European countries, there is a widespread consensus that furloughing employees where possible is very beneficial in the long run. Before the recovery fund was agreed, the EU provided EUR 100 billion for the SURE program, much of which has already been distributed to countries, including Italy, Spain, Poland, and Romania. It is plausible that the program will be increased in size to help protect more jobs.

Fiscal Deficits to Rise Before Stabilizing

Worsening economic projections invariably translate into bigger deficits: A combination of increased fiscal support and lost tax revenues would likely push fiscal deficits to beyond 10% of GDP in all major eurozone countries, even if economies continued to recover uninterruptedly, as in the quick‑recovery scenario. We expect France to be the worst‑hit eurozone economy this year with a deficit of around 15% of GDP, followed by Spain. Italy and Germany should fare better with deficits of around 11% of GDP, largely due to better‑than‑expected tax receipts to date.

As economies should bounce back next year, we expect fiscal deficits to moderate but remain higher than normal. In the intelligent lockdown scenario, we would expect deficits to shrink significantly, from EUR 1.1 trillion to around EUR 700 billion. Germany’s deficit would likely fall the most, potentially to around 5% of GDP. France and Spain are likely to be laggards, with deficits of around 11% and 8%, respectively, given the limited appetite in both countries to bring public finances in order quickly because of domestic political concerns.

If another wave of national lockdowns occurs, most countries’ deficits will remain as high in 2021 as they are this year and will potentially rise if more direct support is required. If overall 2021 deficits stay at around EUR 1 trillion before falling to EUR 500 billion in 2022, the ECB’s PEPP program will be at least EUR 1 trillion short of the amount required to absorb all government bond issuance. Financing deficits of that size without central bank support will be very difficult for the majority of eurozone countries. Given the potential repercussions of countries being forced to restructure their debt, we would expect the ECB to extend quantitative easing purchases by as much as necessary to purchase all net issuance of government bonds.

The partial lockdown scenario would also strain public finances, albeit to a lesser degree than the national lockdown scenario. Both would result in high deficits and rising debt ratios in 2021, leaving the PEPP around EUR 500 billion short of the amount required to purchase all government bonds.

ECB Support Likely to Keep Spreads Stable

Ratings agencies are unlikely to downgrade any eurozone sovereign debt until late this year or early next year. When they do, France and Spain will be subject to bigger downgrade risk than Italy. Italian debt is already rated BBB‑ and is unlikely to be downgraded further given ECB support and fiscal transfers via the EU recovery fund. French and Spanish debt are both rated several notches above Italian debt, giving ratings agencies the space to downgrade them if they fail to deliver medium‑term consolidation plans.

The ECB’s support programs have provided a major boost to peripheral eurozone countries, which will likely keep spreads relatively stable over the medium term. The ECB is technically sucking in all net new issuance, leaving market debt stock largely unchanged, while increased banking system liquidity has probably increased demand for sovereign bonds among residents. French and Spanish bonds may underperform if the debt of either country is downgraded, but the overall impact would unlikely be large.

Strict new lockdowns and the prospect of a double‑dip recession would likely cause some initial spread widening, although this would probably be short‑lived as we would expect the ECB to step in quickly in that scenario. An extension of the PEPP should then result in similar spread compression to that which occurred in May.

The euro will likely hold against the dollar in the intelligent lockdown scenario, as Europe continues to manage the virus better than the U.S. and benefits from stronger consumer and business confidence. In either a national or partial lockdown scenario, the euro may come under pressure, depending on the severity of the lockdown, and could fall back to a EUR/USD rate of 1.10 to 1.15.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

November 2020 / INVESTMENT INSIGHTS

February 2020 / Overview

Is There Going to Be a Eurozone Recession in 2020?