April 2022 / INVESTMENT INSIGHTS

High Yield Bonds Could Prove Resilient as Inflation Surges

Shorter durations, higher yields could provide a buffer as rates rise

Key Insights

- Below investment-grade bonds tend to be more resilient in rising rate environments because of their higher yields and shorter durations.

- High yield bonds have generated positive returns in periods of rising interest rates during the last 15 years.

- However, high yield bonds are not immune to the effects of inflation, so we actively try to manage inflation risk in the strategy.

Inflation and rising rates have left many investors wary of investing in bonds as traditional fixed income asset classes—which have relatively low yields and more sensitivity to interest rate risk—have historically not fared well in this type of climate. However, fixed income strategies that specialize in below investment-grade credit such as high yield bonds and bank loans tend to be more resilient in these environments. This stems, in part, from the higher yields and shorter durations1 of these segments.

Inflation and the Fed

Broad-based supply disruptions stemming from pandemic-related shutdowns and more recently from the Russian invasion of Ukraine have affected everything from transportation to labor to raw materials, which has resulted in higher prices for many goods and services. This, coupled with pent-up demand as economies reopen and consumers are flush with savings and eager to spend after prolonged lockdowns, has brought inflation rates to levels not seen since the early 1980s.

The Federal Reserve has two primary tools for managing inflation—increasing rates and tightening monetary supply by reducing the size of its balance sheet. Keeping inflation near a 2% target and maintaining full employment form the central bank’s mandate. After taking a patient approach throughout most of 2021, the Fed has recently pivoted to a much more hawkish tone, and markets now expect rate increases and balance sheet reductions to occur at a much quicker pace.

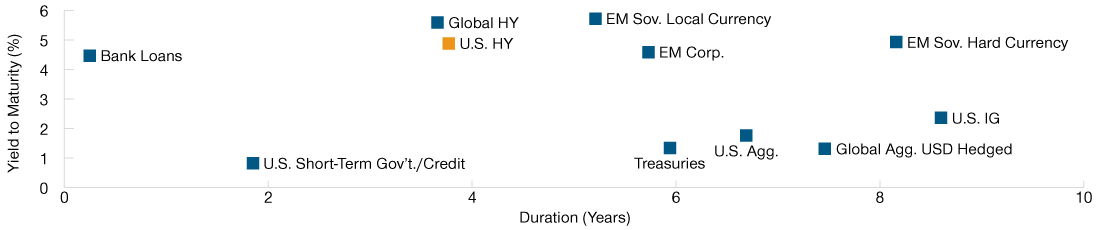

Attractive Yield Relative to Duration

(Fig. 1) Yield versus duration

Past performance is not a reliable indicator of future performance.

As of December 31, 2021.

Source: Data analysis by T. Rowe Price.

U.S. High Yield represented by ICE BofA U.S. High Yield Constrained Index; Bank Loans by S&P/LSTA Performing Loan Index; U.S. Short-Term Gov’t./Credit by Bloomberg 1–3 Year Government/Credit Index; Global High Yield by J.P. Morgan Global High Yield Index; EM Corporate by J.P. Morgan Corporate Emerging Market Bond Index Broad Diversified; EM Sovereign Local Currency by J.P. Morgan Global Bond Index–Emerging Markets Global Diversified; EM Sovereign Hard Currency by J.P. Morgan Emerging Markets Bond Global Index; U.S. Agg. by Bloomberg U.S. Aggregate Bond Index; Treasuries by Bloomberg U.S. Treasuries 4–10 Year Index; Global Agg. USD Hedged by Bloomberg Global Aggregate USD Hedged Index; U.S. Investment Grade by Bloomberg U.S. Corporate Investment Grade Index. Bloomberg Index Services Limited. See Additional Disclosures.

High Yield Bonds Tend to Be Less Affected by Rising Rates

In an environment of rising rates, a shorter duration means less downside risk because money can more quickly be reinvested into newer bonds at higher rates. Meanwhile, higher yields (coupons) provide an added level of income return potential, which can provide a meaningful cushion to help offset any price declines. Additionally, rising rates are typically the product of strong economic growth, and a robust economy tends to boost corporate earnings and revenues. This can make it easier for high yield issuers to service their debt, thereby reducing overall default risk.

As a result, returns of high yield bonds tend to be negatively correlated with U.S. Treasury returns. In fact, over the 15 years ended December 31, 2021, high yield bonds exhibited a -0.3 correlation2 with 10-year Treasuries. A negative correlation means that if U.S. Treasuries are expected to lose value when rates rise, then high yield bonds should actually increase in value.

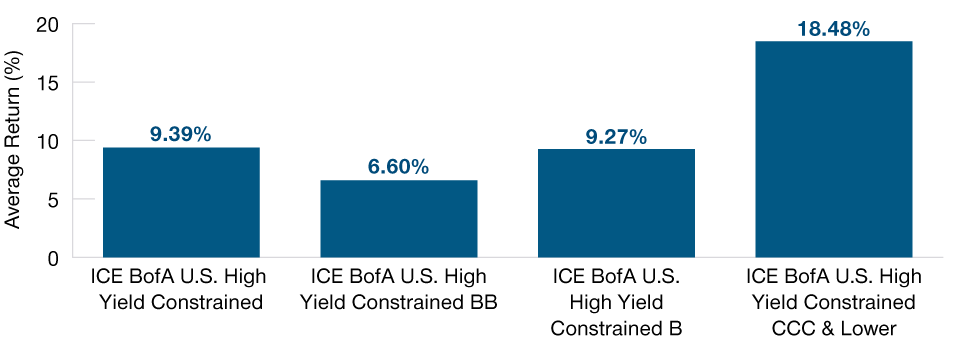

Looking back at historical periods of rising rates, this has indeed been the case. As Figure 2 shows, there have been six time periods where interest rates rose by 100 basis points3 or more over the last 15 years. High yield bonds produced positive performance results in each of those periods, with an average cumulative return of 9.39% (second only to their close relative, bank loans). It is worth noting that yields today are starting from a lower point than they have in the past; therefore, it may be important for investors to temper expectations for future returns.

High Yield Has Been Resilient in Rising Rates

(Fig. 2) Cumulative high yield returns when 10-year Treasury yield rose more than 100 bps

Past performance is not a reliable indicator of future performance.

As of December 31, 2021.

Source: T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.

U.S. High Yield represented by ICE BofA U.S. High Yield Constrained Index; Loans by S&P/LSTA Performing Loan Index; U.S. Agg. by Bloomberg U.S. Aggregate Bond Index; U.S. Short-Term Gov’t./Credit by Bloomberg 1–3 Year Government/Credit Index. Bloomberg Index Services Limited. See Additional Disclosures.

Taking a deeper look and breaking out these high yield bond returns by credit rating, it is evident that the lower quality tiers within the high yield market have tended to generate the strongest returns in these past rising rate environments. Though our portfolio is well positioned to benefit from this trend given our overweight to the lower quality tiers of the market, we are cognizant of the fact that this will reverse at some point in the credit cycle.

Yet Not Immune to the Effects of Inflation

Though high yield bonds tend to be somewhat insulated from the effects of inflation and rising rates relative to many other fixed income asset classes, they certainly are not immune. There are three primary ways that we seek to manage inflation and interest rate risk in the US High Yield Bond Strategy. First, we have maintained an underweight to BB rated bonds (the highest credit rating rung of the non-investment-grade universe), which tend to have the highest interest rate sensitivity in the high yield market. Second, the strategy typically has meaningful allocations to bank loans, which currently offer similar yield to below investment-grade bonds but with shorter duration given their floating rate coupons. The third way that we manage inflation risk is through sector allocation and security selection, which we discuss further below.

Lower-Rated High Yield Has Outperformed in Rising Rates

(Fig. 3) Returns by credit rating when 10-year Treasury yield rose more than 100 bps

Past performance is not a reliable indicator of future performance.

As of December 31, 2021.

Source: T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.

Analyzing the Impact of Inflation on Issuers and Sectors

Inflation has become so rampant and widespread that it is virtually impossible to name an industry or sector that has been untouched by its effects. As part of our bottom-up fundamental credit analysis, we assess the impacts of inflation as we evaluate both current and new investment opportunities. As part of this process, we find ourselves asking questions like:

1. Has inflation driven up the cost of key inputs (e.g., raw materials, transportation, labor, etc.) within this sector or for this issuer?

2. Are the effects of inflation transitory, or are they likely to be felt over the longer term? Why?

3. Does the issuer have the ability to pass higher input costs through to customers via higher prices? To what extent is customer demand for the issuer’s goods or services elastic or inelastic?

4. What supply chain issues exist? When and how do we expect those issues to be resolved?

5. What net impact will inflation have on the profitability of the issuer’s overall business?

Examining the Impact of Inflation

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

† Enterprise value is a company’s equity market capitalization plus its total debt minus its cash and cash equivalents.

As we develop answers to these questions, we naturally look to avoid areas of the market where we expect that inflation will serve as a greater headwind and add exposure to parts of the market that we believe will fare better, unless our broader fundamental and relative value analysis of the opportunity directs us otherwise. We show a few recent examples in the Examining the Impact of Inflation section.

Defaults Expected to Stay Low Through 2023

Overall, our outlook for high yield bonds remains constructive. Though credit spreads4 are tight, default rates remain near historic lows as many companies have taken advantage of low rates over the last 12 to 24 months to refinance and extend their debt. With no meaningful waves of maturing bonds on the near-term horizon, we expect defaults to remain low through 2023. Given that credit risk is the primary risk associated with high yield, we believe this backdrop should bode well for the asset class in the near to intermediate term.

Additionally, high yield bonds can offer an attractive risk/reward profile that combines much of the upside potential associated with equities with some of the downside protection and income associated with fixed income. We think this should be a compelling combination in the current environment of low but rising yields and equity valuations that started the year appearing stretched before encountering selling pressure.

Credit Selection to Remain Important Driver of Returns

As an active and concentrated U.S. high yield manager, we do not seek to make big macro calls on the direction of interest rates, nor do we seek to fully hedge out interest rate risk in our portfolio. With that said, we do strive to understand the impact that inflation and rising rates could have on the investment performance that we seek to deliver to clients and to position the portfolio accordingly. In doing this, we rely heavily on proprietary, bottom-up fundamental credit research, which we view as our competitive advantage.

Given the relatively tight credit spreads in the high yield market today, we believe credit selection will be an even more important driver of returns in the year ahead. We anticipate that periods of volatility could provide some windows of opportunity for active investors like ourselves to take advantage of temporary price dislocations in certain areas of the market.

1 Duration measures a bond’s sensitivity to changes in interest rates.

2 Correlation measures how one asset class, style, or individual group may be related to another. A perfect positive correlation means that the correlation coefficient is exactly 1. This implies that as one security moves, either up or down, the other security moves in lockstep, in the same direction. A perfect negative correlation means that two assets move in opposite directions, while a 0 correlation implies no relationship at all.

3A basis point is 0.01 percentage point.

4 Credit spreads measure the additional yield that investors demand for holding a bond with credit risk over a similar-maturity, high-quality government security.

General Fixed Income Risks

Capital risk—the value of your investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the portfolio and the currency in which you subscribed, if different.

Counterparty risk—an entity with which the portfolio transacts may not meet its obligations to the portfolio.

Environmental, social, and governance and sustainability risk—may result in a material negative impact on the value of an investment and performance of the portfolio.

Geographic concentration risk—to the extent that a portfolio invests a large portion of its assets in a particular geographic area, its performance will be more strongly affected by events within that area.

Hedging risk—a portfolio’s attempts to reduce or eliminate certain risks through hedging may not work as intended.

Investment portfolio risk—investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Management risk—the investment manager or its designees may at times find their obligations to a portfolio to be in conflict with their obligations to other investment portfolios they manage (although in such cases, all portfolios will be dealt with equitably).

Operational risk—operational failures could lead to disruptions of portfolio operations or financial losses.

Additional Disclosures

ICE Data Indices, LLC (“ICE DATA”), is used with permission. ICE DATA, ITS AFFILIATES AND THEIR RESPECTIVE THIRD-PARTY SUPPLIERS DISCLAIM ANY AND ALL WARRANTIES AND REPRESENTATIONS, EXPRESS AND/OR IMPLIED, INCLUDING ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, INCLUDING THE INDICES, INDEX DATA AND ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM. NEITHER ICE DATA, ITS AFFILIATES NOR THEIR RESPECTIVE THIRD-PARTY SUPPLIERS SHALL BE SUBJECT TO ANY DAMAGES OR LIABILITY WITH RESPECT TO THE ADEQUACY, ACCURACY, TIMELINESS OR COMPLETENESS OF THE INDICES OR THE INDEX DATA OR ANY COMPONENT THEREOF, AND THE INDICES AND INDEX DATA AND ALL COMPONENTS THEREOF ARE PROVIDED ON AN “AS IS” BASIS AND YOUR USE IS AT YOUR OWN RISK. ICE DATA, ITS AFFILIATES AND THEIR RESPECTIVE THIRD-PARTY SUPPLIERS DO NOT SPONSOR, ENDORSE, OR RECOMMEND T. ROWE PRICE OR ANY OF ITS PRODUCTS OR SERVICES.

Copyright © 2022, S&P Global Market Intelligence (and its affiliates, as applicable). Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statements of fact.

Bloomberg Finance L.P. Bloomberg®, Bloomberg 1-3 Year Government/Credit, Bloomberg U.S. Aggregate Bond, Bloomberg U.S. Treasuries 4-10 Year, Bloomberg Global Aggregate USD Hedged, and Bloomberg U.S. Corporate Investment Grade are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by T. Rowe Price. Bloomberg is not affiliated with T. Rowe Price, and Bloomberg does not approve, endorse, review, or recommend US High Yield Bond Strategy. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to US High Yield Bond Strategy.

Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright © 2022, J.P. Morgan Chase & Co. All rights reserved.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.