March 2021 / MARKETS & ECONOMY

Vaccine Progress Hands UK Economic Boost Over EU

Sterling looks set to strengthen against the euro

Key Insights

- The UK’s rapid progress in vaccinating against the coronavirus may help its economy to outperform the European Union’s (EU) for at least the first half of this year.

- Central and Eastern European (CEE) countries are likely to outperform the EU due to larger hospital capacity and greater herd immunity owing to less restrictions.

- We expect the sterling and the Czech koruna to strengthen against the euro this year, while UK and CEE bond yields may come under upward pressure.

The UK’s rapid progress in vaccinating its citizens against the coronavirus may help its economy to outperform the European Union’s (EU) for at least the first half of this year. Central and Eastern European (CEE) countries are likely to outperform the bloc over the same period due to larger hospital capacity and greater herd immunity owing to less strict lockdowns.

We assessed the speed at which European countries are likely to exit current lockdown regimes based on four factors: first, the supply schedule of vaccine in the next couple of months; second, the take‑up by the local population; third, the R rate of the predominant COVID‑19 variant in the population; and fourth, the speed of building natural immunity via past infections.

These relationships are nonlinear, meaning that once the number of people who have gained immunity from either a previous infection or a vaccine crosses a certain threshold, infections fall rapidly. At a certain point, infected persons cannot spread the virus to more than one other person, which means virus spread is contained without restrictions on people’s movements—this is typically referred to as “herd immunity.” In our analysis, we estimated the number of people with immunity from past infection and added that to the number of people who had received vaccines, taking into account potential double‑counting. We also accounted for the imperfect protection provided by both natural infection and vaccines (we believe the protection from both is around 80%).

The UK and EU: A Tale of Two Vaccination Schemes

Lockdowns in most European countries are a function of hospital capacity and coronavirus deaths. Although most coronavirus deaths recorded have been among the elderly, the stress on the hospital system comes from middle‑aged adults with the coronavirus staying in hospitals for several weeks at a time. Therefore, while vaccinating the elderly will help to reduce deaths, mass vaccination is necessary to avoid future outbreaks and reduce the stress on the hospital system. Achieving a high degree of vaccination quickly, and hence the ability to exit lockdown faster in the spring, is a function of both vaccine supply and demand.

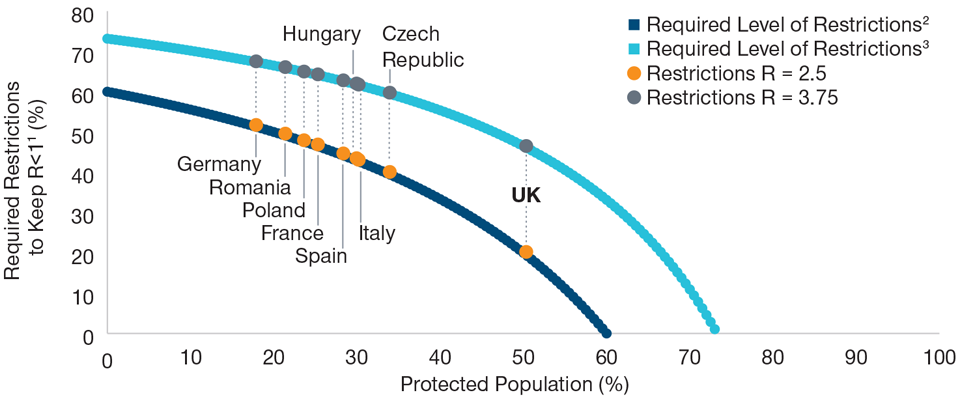

The UK Is Furthest Along the Path Toward Opening Its Economy

(Fig. 1) Germany and France are lagging significantly behind

As of February 28, 2021.

R = reproduction rate—the average number of secondary infections produced by a single infected person.

1 A higher percentage of required restrictions means that more restrictions are required to keep the R rate below 1.

2 R = 2.5.

3 R = 3.75, “new strain.”

Source: Our World in Data and estimates based on T. Rowe Price calculations.

The UK and EU have had very different experiences of procuring and administering coronavirus vaccines. The UK invested heavily in procuring a large portfolio of different types of vaccines, helped to develop the Oxford‑AstraZeneca vaccine, and established a domestic infrastructure to manage the delivery of vaccines around the country. This investment has paid off: By February 15, the UK had vaccinated 23% of its population with at least one dose of the vaccine—the best performance by far of any large country in the world.

EU countries took a different approach. To prevent vaccine nationalism within the bloc, it was agreed that procurement would be handled at the EU‑wide level. Unfortunately, negotiation delays meant that the EU only ordered the Pfizer/BioNTech vaccine after the first results were released in November, which likely resulted in an eventual delay in their delivery. Production problems in designated AstraZeneca production facilities in the EU meant that the firm had to drastically reduce vaccine supply to the EU in the first half of 2021. In addition, the EU decided to stick to the three‑week period between the first and second doses for Pfizer and Moderna vaccines rather than extending them out as the UK has done, which has meant that less people have received the first shot. This has created a vaccine supply shortage: The largest four EU countries have only been able to vaccinate around 3.3% of their populations. Vaccine supply problems should become less of an issue from April onwards, but that will be reliant upon the successful administration of the Oxford‑AstraZeneca and Johnson & Johnson vaccines, with the latter yet to be approved by the European Medicines Agency. The EU will eventually receive greater supplies of the Pfizer and Moderna vaccines, but this is unlikely to occur before June.

Confusing Messages Likely Hindering Progress in EU

Vaccine supply is only one side of a successful vaccination program, however. To achieve a high degree of national immunity, people need to be willing to take the vaccine. Historically, voluntary vaccine take‑up in the UK has been higher than in other European countries: European Centre for Disease Prevention and Control data show that the UK had 75% flu vaccine take‑up in 2014–2015, compared with around 50% in the larger eurozone countries. Recent survey data on voluntary vaccine take‑up across countries suggest similar take‑up rates for the new COVID‑19 vaccines. This suggests that authorities in most EU countries will need to work hard to convince citizens to get the new COVID‑19 vaccine.

Clear communication by credible health authorities can help to convince more people to get vaccinated. There have been conflicting messages in Europe, however, where a number of countries only approved the Oxford‑AstraZeneca vaccine for those under age 65 due to lack of data—despite the fact that the European Medicines Agency had already approved it for all ages. As a result, reports suggest, people in several European countries are refusing to receive the Oxford‑AstraZeneca vaccine because of what appears to be unfounded fears over its safety and efficacy.

Unlike the UK, therefore, most EU countries will likely experience vaccine demand issues for the forseeable future. Other vaccines will be approved in the coming months, but these demand issues might exacerbate current supply issues to the extent that it becomes practically difficult to vaccinate all adults in the EU ahead of the next coronavirus season.

The third key factor in the success of the vaccination program is the contagiousness of the virus. The higher the natural reproduction number of the virus, the greater the proportion of the population that requires vaccination to avoid future coronavirus outbreaks. The new coronavirus strain first detected in the UK is 50% to 70% more contagious than the initial strain and is becoming the predominant strain in the EU, making up 35% of all new cases in France and 20% in Germany in February 2021. Ongoing mutations in the virus in the EU will mean that a higher proportion of the population will need to be vaccinated, and low demand might make the goal of vaccinating a sufficiently large number of people to prevent outbreaks before winter 2021 challenging.

The UK Is Set for a Summer Reopening

The goal of any mass vaccination program is to prevent further outbreaks and allow life to return to normal. There is an important nonlinear relationship here: Once a certain threshold of natural immunity from existing antibodies and vaccines has been crossed, COVID‑19 cases will likely decline very rapidly, and the need for restrictions on social consumption should completely disappear. Our models, based on assumptions about current antibody levels, vaccine supply and take‑up, as well as the degree of virus contagion, can help to answer when individual European countries might reach the stage at which future outbreaks are unlikely.

Our analysis shows how vaccine take‑up and the degree of coronavirus vaccination interact to help provide a date at which outbreaks are less likely. For the UK, which has strong projected vaccine supply and demand, our models show that the required level of restrictions to prevent future outbreaks will likely fall to zero between late May and July, despite the more infectious B.1.17 variant as the predominant variant in the UK now.1

On the other hand, if the infectious B.1.17 variant becomes the dominant strain in France (as is likely given the spread this year so far), slower vaccination progress (80% of population vaccinated by the end of 2021) means that France may only reach the point at which restrictions can be relaxed in September if vaccine supply falls short of expectations. This also applies to Germany. For Italy and Spain, this point could be reached between July and August. Overall, our models show that the UK will likely be able to lift all restrictions between May and June, two to three months earlier than most large eurozone countries.

Central and Eastern Europe to Reopen Quicker Thanks to Greater Hospital Capacity

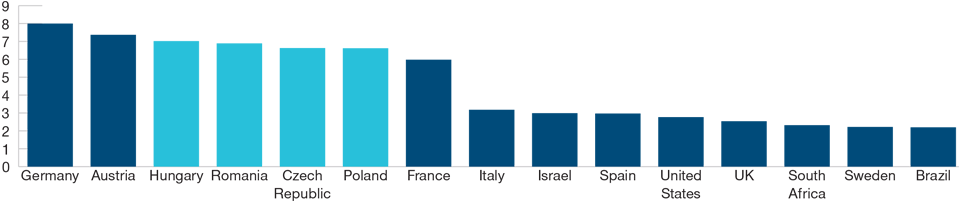

CEE countries took a different approach to tackling the coronavirus than either the UK or the EU. The initial strategies of many countries was to impose few restrictions in the hope that hospital capacity—where central and Eastern Europe surprisingly fares better than many of its Western European peers— would be able to cope with high levels of infections (see Figure 2). That strategy worked until about mid‑October, when mortality rates began to rise and tougher restrictions were required to avoid overwhelming health care systems. The main restrictions imposed were on the hospitality sector, which has remained broadly shut since then. However, the manufacturing sector—which accounts for a relatively larger proportion of the economies of CEE countries than it does those of Western Europe (with the exception of Germany)—has continued to operate close to pre‑coronavirus levels. This has given CEE economies a major boost.

We expect CEE countries to continue following the existing approach, meaning the manufacturing sector will be kept open unless there is a total collapse of the health care system, which seems unlikely given the degree of herd immunity already achieved through past infections. As such, we expect CEE economies to reopen by about midsummer, potentially one to two months earlier than their Western European peers.

Sterling and Czech Koruna Likely to Continue Appreciating vs. the Euro

In our view, the UK’s ability to fully lift restrictions two to three months earlier than most eurozone countries may help its economy to outperform most of its European neighbors from the second quarter of 2021 onward. Hotter weather in the summer will likely help some eurozone countries to open up as well, but—unlike the UK—the risk of restrictions being reimposed in Europe will remain in the autumn if the current vaccination plans are not accelerated.

Central and Eastern Europe Has Comparatively High Hospital Capacity

(Fig. 2) Hungary and Romania have more beds than France, Italy, and Spain

As of February 28, 2021.

Source: Our World in Data and T. Rowe Price calculations.

Although the coronavirus will likely not be the UK’s only economic challenge in the medium term, it is the most important challenge in the immediate term, and financial markets have already begun to price a stronger sterling against the euro. We believe the sterling will continue to strengthen against the euro well into the second quarter of 2021, at which point seasonality from summer weather should also support a strong bounceback in eurozone activity.

Looking further ahead, there is a risk that coronavirus mutations will mean that annual top‑up vaccinations are necessary. The UK has invested heavily into domestic vaccine supply chains, with four candidate vaccines (AZN, Curevac, Novovax, and Valnovo) to be manufactured in the UK from 2021 onward. This, together with the development of widespread vaccine delivery infrastructure, will likely help the UK to successfully develop and deliver booster shots in response to coronavirus mutations if necessary. It remains to be seen whether EU countries will be able to make as much progress in the future proofing vaccine development and delivery.

Further east, stronger economic performance and the Czech National Bank’s willingness to raise interest rates should support the koruna. We expect the Czech economy to accelerate massively starting from the second quarter of the year and then return to pre‑coronavirus levels by the end of 2022. The Czech National Bank indicated that the recovery pace is consistent with the policy rate rising to above 1% by the end of 2022 versus expected unchanged policy rates in the eurozone, supporting the Czech koruna strengthening versus the euro.

For other regional currencies, the situation is more mixed. Although we expect CEE economies to perform better overall than the eurozone, CEE central banks are likely to keep monetary conditions very accommodative, preventing meaningful currency appreciations. We therefore expect relative stability in the Polish zloty and the Hungarian forint despite the likely earlier reopening of the Polish and Hungarian economies.

Yields to Rise on Recovery Story

We believe that bond yields may rise at the prospect of lockdowns being eased. The liberation of economies that have been artificially suppressed for an extended period should unleash a burst of economic activity, fueling inflation expectations. We believe the majority of European central banks will regard inflation as a transitory shock and are therefore likely to maintain their current accommodative policy stances and focus more on employment and supporting government fiscal policies. In this environment, we believe the yields on longer‑term government bonds, in particular those of the UK and central and Eastern Europe, may come under upward pressure.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

March 2021 / INVESTMENT INSIGHTS

March 2021 / MARKETS & ECONOMY