February 2021 / MARKETS & ECONOMY

The EU-UK Trade Deal Leaves Open Questions

But the exclusion of some areas brings opportunity for reform

The wait is finally over. Four‑and‑a‑half years after the Brexit referendum, the UK has exited the European Union’s single market and customs union, leaving behind a political and economic arrangement that had been in place since 1973. However, while the trade deal agreed between the two sides provides clarity in some areas, a great deal of uncertainty remains about what Brexit will mean in practice.

In the 10th of a series of updates, Quentin Fitzsimmons and Tomasz Wieladek, T. Rowe Price’s resident Brexit experts, provide an overview of the current state of play.

What Has Happened Since Our Last Update?

After months of demanding negotiations, on Christmas Eve, the UK and the EU finally agreed to the Trade and Cooperation Agreement (TCA) covering their post‑Brexit trading and security relationship. It was a hard‑won achievement: Since the UK formally left the EU on January 31, 2020, talks to determine the future relationship between the two had stuttered badly against the backdrop of a global pandemic, with both sides accusing the other of recalcitrance and inflexibility. While a deal of some kind was always the most likely outcome, the potential for failure kept markets guessing right until the end. A no‑deal Brexit was always possible.

What we have instead would have been referred to as a “hard Brexit” at the time of the referendum. The agreement on tariff‑ and quota‑free goods trade means there will be no new taxes to pay on goods wholly made within the UK or EU. However, the TCA’s “rules of origin” clause means that UK firms selling goods that contain components made outside the UK or EU may be subject to value-added tax and import duties. Non‑tariff barriers will also rise as trade between the UK and EU is subject to a raft of new regulations, checks, and red tape. The UK government has estimated that there will be an extra 215 million customs declaration forms for British businesses importing or exporting goods, potentially resulting in delays at ports such as Dover.

Although some of these frictions will have a permanent impact on goods trading, the brunt of adjustment costs should be short term and temporary in nature as businesses on both sides of the channel adapt to the new trade regime. More of a concern is the TCA’s thin coverage of services, the UK’s main export. Although some services, such as the legal industry, are covered in the agreement, many others are not. The UK financial service industry, for example, will need to rely on being granted “equivalence” from Brussels to provide the same services in the EU as it did before (an equivalence agreement recognizes that the regulations of a third country are equivalent to the EU’s own, allowing firms from both territories to operate in each other’s jurisdictions).

The UK and the EU are due to sign a memorandum of understanding on financial services regulation and cooperation by March, but this will probably only establish a process for how to engage on these issues going forward. The European Commission will likely only grant equivalence after it has assessed regulatory divergence, and it has a great economic self‑interest to only grant equivalence to those areas in which London has a strong competitive advantage and which can’t be easily replicated in the EU. It therefore seems unlikely that the financial services sector will enjoy the same level of access as it did prior to Brexit.

In the interim, the current arrangement is closer to a “no deal” for financial services, which is a concern given that, according to the Corporation of London, financial services contribute 10.5% of all UK tax receipts, and around 40% of the sector’s exports go to the EU. However, in areas where equivalence is not granted, a “no deal” state of the agreement means that the UK will be free to diverge from the EU and increase its competitiveness without any tariff consequences from the bloc.

What Happens Now?

Trade in many areas will remain muted while coronavirus lockdowns are in place, and many British businesses stockpiled goods from the EU before December 31. At the same time, the UK Border Force has said it will only apply the new customs regime after June 2021. These factors will obscure the initial impact of the UK’s departure from the single market and customs union; it will only be when the pandemic is comfortably behind us that the longer‑term regulatory implications of the TCA will become clear.

As things stand, then, there is probably 70% clarity on how goods trade will operate long term. When full clarity is reached, some businesses may eventually decide that cross‑border trade is prohibitively costly.

On services, market access negotiations will likely continue for some time. It remains to be seen how far March’s memorandum of understanding between the EU and UK—if agreed—will go, but it is likely that Brussels will take a “wait and see” approach to any future equivalence agreements, in which case it will be a while before a meaningful EU‑UK agreement on financial services is reached.

A Once‑in-a‑Generation Regime Shift—and Opportunity

In the short term, the UK’s economic prospects depend on both the Brexit trade adjustment costs and the evolution of the pandemic. While stocking up, limited traffic due to the coronavirus, and looser UK Border Force control will all mitigate the disruption, it is likely that the impact of Brexit adjustment costs to manufacturing will become apparent during the first quarter of this year. This will probably weigh on UK gilt yields and lower sterling.

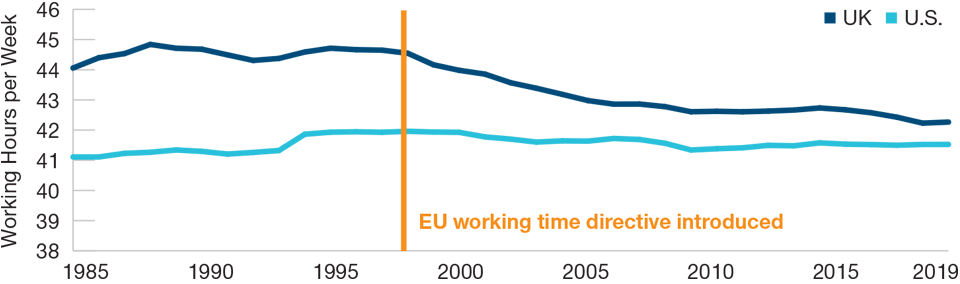

Scrapping EU Law Could Boost UK Working Hours

Working time directive caused weekly hours to fall

As of December 31, 2019.

Source: OCED/Haver Analytics.

However, the UK is currently vaccinating its population at a significantly faster rate than eurozone countries. This means that, in the absence of new vaccine‑resistant strains of the virus, the UK should be able to emerge more quickly than the eurozone from the current lockdown. If the UK can begin to relax restrictions three to four weeks earlier than the eurozone, this will likely strengthen sterling against the dollar and lead to a rise in gilt yields by the spring as investors turn to riskier assets.

The UK’s departure from the EU represents a major regime shift, and it will take time for a new economic equilibrium to be established. The trade frictions discussed above will likely have some negative medium‑term effects on UK gross domestic product (GDP), but the UK can offset this if it uses its new regulatory freedom smartly. This can be done in three main ways.

First, it could deregulate parts of the economy that are not covered in the agreement, such as the financial services sector. For example, the UK government could scrap the EU’s bank bonus cap. Allowing firms, rather than the law, to award much larger variable pay on top of smaller fixed pay would allow a much larger reduction in variable pay in a crisis, reducing the need for tax‑funded bailouts. As with any financial reform, excessive deregulation could lead to greater boom‑bust cycles. However, the UK regulatory apparatus established after the global financial crisis, with great focus on stress‑testing financial system resilience in response to any reform, will help to mitigate these risks.

A second option would be to reduce the UK implementation of EU regulation to the “bare bones” EU standard. This would increase competitiveness without triggering any retaliatory tariffs relating to the level playing field. For example, the EU’s working time directive requires a minimum of four weeks paid annual leave for full‑time employees, but in the UK implementation, it is 5.6 weeks (four weeks and all UK holidays). A reduction of holiday time by one week a year, perhaps by allowing employees to sell back some of their leave entitlement to their employer or raising working hours by one hour a week, could boost UK potential GDP by 2% (average UK weekly working hours fell when the reform was implemented in 1998). Clearly, there will be political resistance to such changes in the labor market, but it is precisely these types of reforms that have the largest economic gain medium term.

Finally, the UK government could use the political momentum behind Brexit to push for economic reform in areas unrelated to Brexit and the EU, such as reforming the British planning system. This would raise the amount of housing construction and lower costs at the same time, which would be an economically significant and positive supply shock to the UK economy. At the same time, the demand for building labor would rise, which would likely support wage growth in the construction sector across the UK.

An Uncertain Future

The longer‑term effects of Brexit and economic reforms on potential UK GDP growth are highly uncertain. The impact of trade frictions on UK GDP growth will depend on several important factors that have yet to be resolved, such as the new framework for the provision of financial services in the EU. Similarly, the impact of reforms on productivity growth will be highly dependent on the depth, breadth, and political acceptance of those reforms.

Trade frictions will certainly weigh on UK GDP for some time, even after the pandemic is over. On the other hand, if the government fully exploits the regulatory autonomy granted by leaving the EU and also uses the political momentum to reform unrelated economic sectors, the positive effects on potential GDP growth could be economically significant and visible in the data within two to three years. Any indication that this is the path the UK is heading toward will likely result in a steeper gilt yield curve and sterling strengthening against the euro, relative to current levels, over the medium term.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

February 2021 / INVESTMENT INSIGHTS