March 2023 / INVESTMENT INSIGHTS

A new perspective on the LDI fallout and the importance of asset liquidity

Why an actively managed, high quality fixed income strategy can help pension funds manage their liquidity waterfall

Key Insights

- Last year’s liability-driven investment (LDI) crisis caused funding problems for many UK defined benefit pension schemes, with some forced to liquidate assets at disadvantageous prices.

- For fund sponsors, a clear takeaway from the crisis is to look carefully at the liquidity of their pension schemes’ asset holdings.

- The T. Rowe Price Funds SICAV - Dynamic Global Bond Fund enjoys the flexibility to go long or short across countries, currencies and sectors.

- A highly liquid fund, aiming to achieve consistent returns above cash and offering diversification in turbulent markets, can form part of the typical pension scheme’s defensive portfolio.

The crisis in longer-dated UK government debt in the autumn of 2022 exposed shortcomings in the resilience of liability-driven investment (LDI) and the operational processes of the pension schemes using this approach.

The inability of some schemes to meet margin calls in a timely manner raised serious questions about the effectiveness of their interest rate and inflation hedges. The crisis is likely to have a longrun impact on the way defined benefit (DB) pension funds manage the liquidity of their assets.

Yield rises and strains on LDI

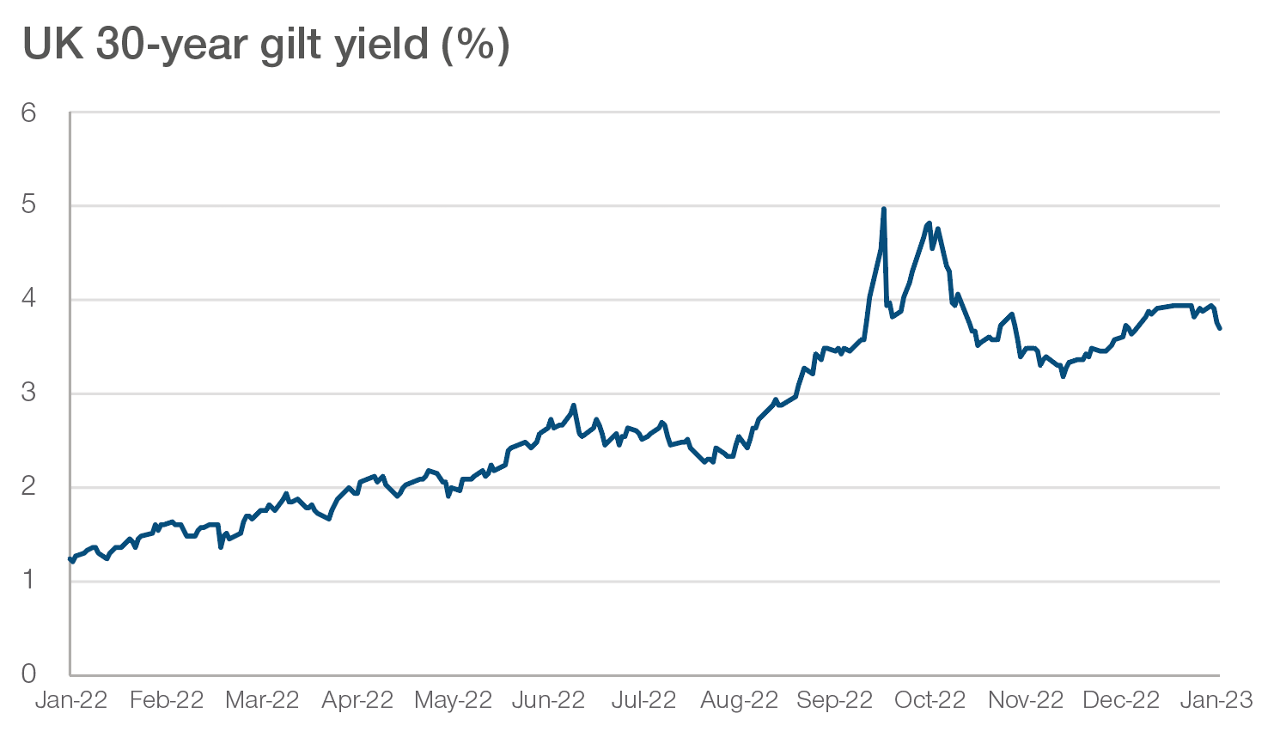

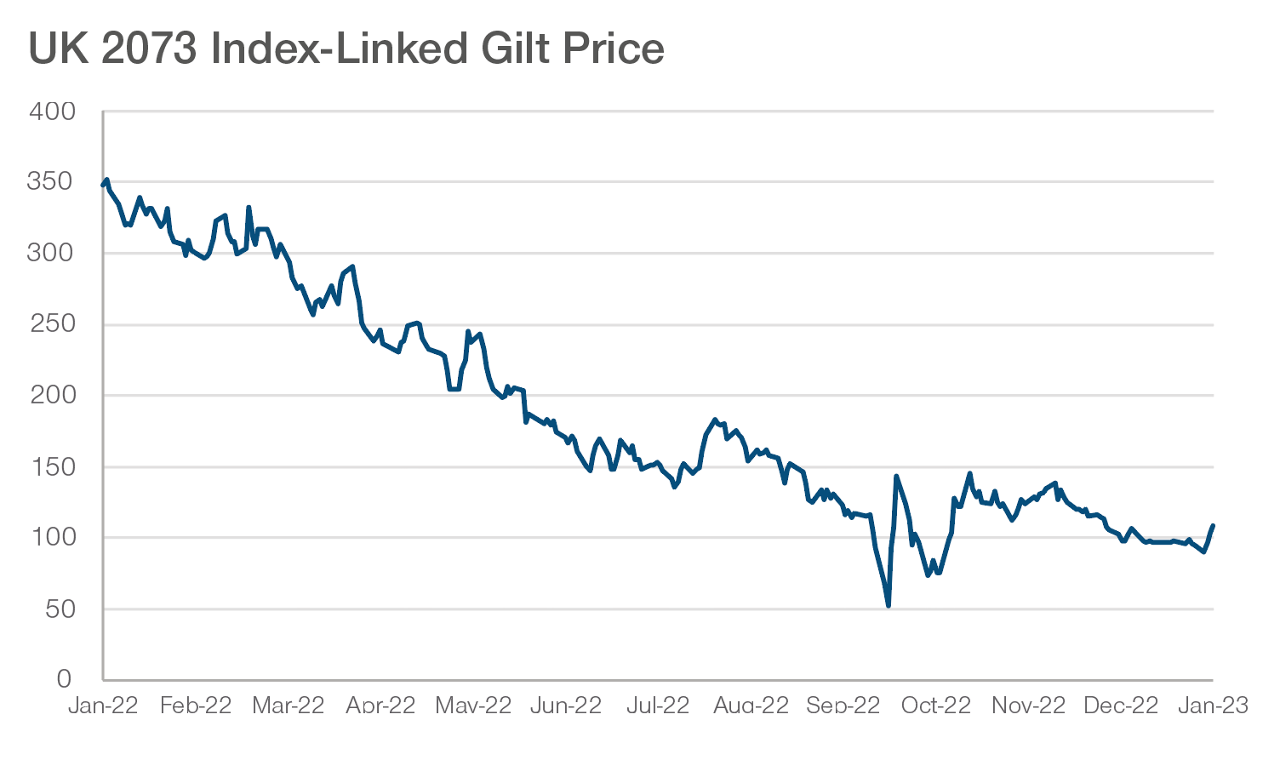

The dramatic autumn sell-off in UK government bonds drove 30- year conventional yields to over 5 percent and caused the one-year decline in the price of the long-dated (2073) index-linked gilt to exceed 90 percent—a performance worthier of a failed dot.com stock or a cryptocurrency than a notionally “gilt-edged” security.

An intervention by the Bank of England, involving temporary purchases of long-dated gilts, helped bring down yields and stabilise the market.

However, the dramatic interest rate moves caused unprecedented strains on the defined benefit pension schemes involved in LDI.

By using LDI, pension schemes can manage the funding risk caused by changes in interest rates and inflation. The leverage embedded in LDI means pension schemes do not have to pay the full upfront cost of the fixed income portfolio required to hedge these interest rate and inflation risks (this is because LDI causes the schemes’ assets to move in a similar direction and magnitude to the present value of future pensions obligations).

Past performance is not a reliable indicator of future performance.Source: Bloomberg Finance L.P. Data as at 23/01/2023.

However, as LDI involves investing in derivatives, September’s adverse move in the value of the hedging portfolio (the bond bear market caused it to plummet) required LDI pension schemes to post extra collateral to dealers to maintain margin levels. These sudden collateral demands caused funding problems for many schemes, with the risk of subsequent sales of gilts to raise cash threatening a wider, self-fulfilling liquidity crisis.

A crisis, but in the short term

As a result of their forced gilt sales, some pension schemes involved in LDI will have ended up closing their hedges at disadvantageous rates, leaving them underfunded and requiring extra funds from parent company sponsors.

Overall, however, the impact of the 2022 bond bear market was positive for UK DB pension schemes, whose solvency improved.

Although pension schemes’ fixed income assets have fallen in value, their future pension liabilities (which are discounted by long-dated bond yields) will have fallen even faster.

The vast majority of DB schemes will therefore have moved closer to their ultimate goal of buy-out, risk transfer or self-sufficiency.

Managing the waterfall

For DB fund sponsors, a clear takeaway from the 2022 gilt crisis is to look carefully at the liquidity of their asset holdings and, where appropriate, to make changes.

Many of those DB pension schemes will have ended the year with an asset portfolio consisting of the remaining LDI assets, cash and investments in less liquid private markets.

Some are likely to now be looking to rebuild allocations, but by taking a more cautious approach to managing the overall portfolio liquidity “waterfall” (the order of sale of assets in any future call for collateral).

The improved DB pension scheme funding levels are also likely to have brought forward the timeline for possible future buy-in or buy-out arrangements.

Buy-ins and buy-outs are insurance policies that can be bought by pension scheme trustees to remove some or all of the risks associated with the scheme.

A large proportion of illiquid assets can limit a pension scheme’s room for manoeuvre if such assets are not acceptable to an insurer and they cannot be easily disposed of via a secondary market.

Improved DB scheme funding positions also reduce the pressure on trustees to seek assets that can outperform gilts, if the promised extra returns come at the expense of illiquidity—as may be the case with private assets.

Prioritise liquidity

2022 has illustrated how collateral crises can happen when both equity and fixed income assets fall in value at the same time.

A highly liquid fund, aiming to achieve consistent returns above cash and offering diversification in turbulent markets, can form part of the typical pension scheme’s defensive portfolio.

The T. Rowe Price Dynamic Global Bond Fund offers daily liquidity and enjoys the flexibility to go long or short across countries, currencies and sectors.

The fund has been a recent stand-out performer in its peer group, generating a healthy positive return in 2022, despite the global bond market rout. The fund’s low correlation to risk assets, particularly to credit, equities and emerging market debt, means its return profile is not dependent on market beta.

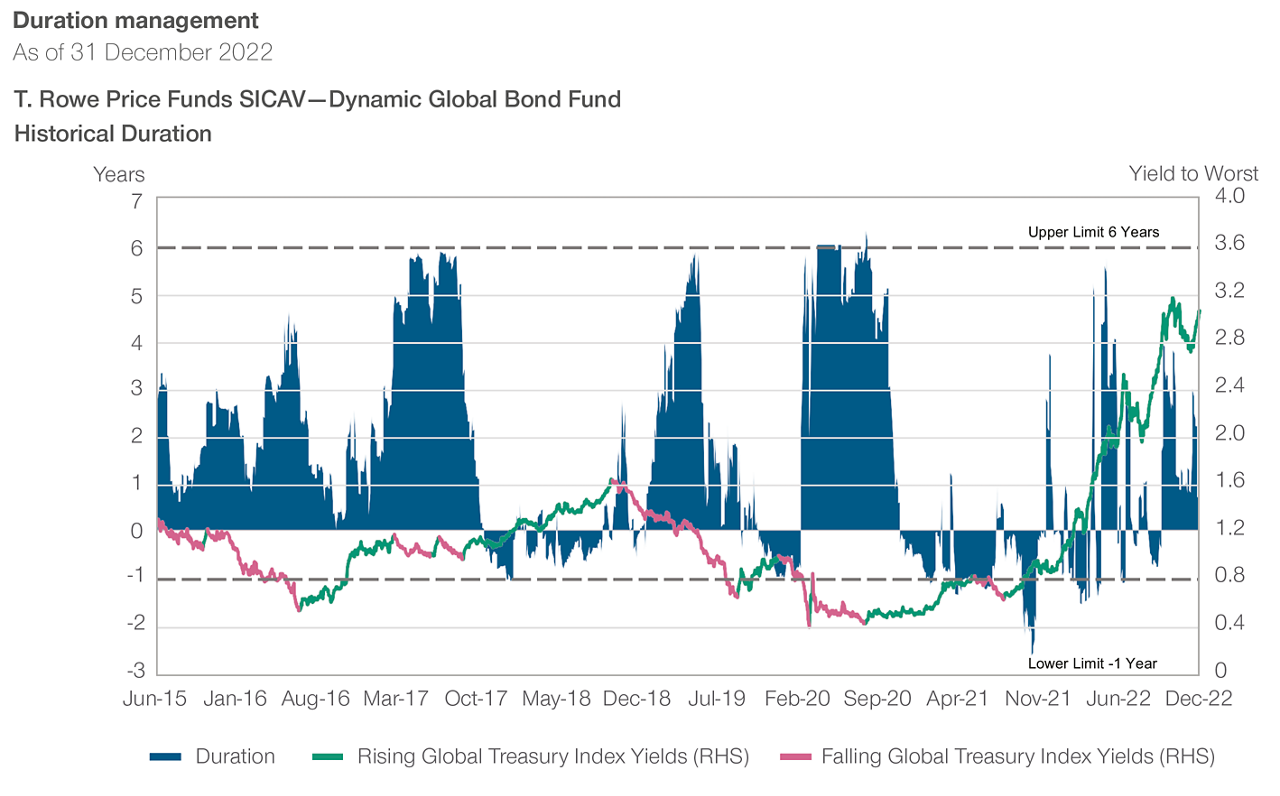

The duration times spread (DTS) of the Dynamic Global Bond Fund has oscillated between +/-5 in 2016-2022, showing the fund managers’ willingness to take on both positive and negative exposure to credit risk during the period (see the chart). The negative DTS maintained from September 2021 onwards helped generate positive returns during last year’s bond market rout.

Past performance is not a reliable indicator of future performance.

Analysis by T. Rowe Price. Source: Bloomberg Finance L.P. Index yield shown is for the Bloomberg Global Treasuries Index. Periods of rising / falling yields havebeen determined as periods of changes in yields of 15 bps or greater.

During the LDI crisis, the reliance on gilts as a “safe” asset contributed to the forced selling seen when pension schemes faced collateral calls. By contrast, almost 80 percent of the Dynamic Global Bond Fund’s portfolio is invested in government bonds across 40 countries and over 20 currencies. This ensures high liquidity and healthy levels of diversification across global bond markets, reducing the possibility of a repeat of last year’s fire sales in long-maturity conventional and index-linked gilts.

The Dynamic Global Bond Fund’s portfolio has been stress-tested in the past. In March 2020, despite market panic surrounding the outbreak of coronavirus, the fund’s portfolio managers were able to return over $1bn in cash within a week to a client looking to change asset allocation.

And in line with regulatory requirements, the SICAV version of the Dynamic Global Bond Fund has undergone a test showing that, in normal market conditions, it can return more than three-quarters of fund assets to investors in cash in under five days.

Don’t play the blame game

Some of the fallout from the LDI crisis has been relatively unconstructive. Under parliamentary scrutiny and forced to account for themselves on the record, certain pension funds and pension consultants have been pointing the finger at each other, aiming to apportion blame for September’s dramatic market events.

But savvier investors will be drawing a wider, strategic lesson from the crisis: an active asset manager, skilled in navigating changing market conditions, can help clients meet the two-fold objective of generating returns and managing liquidity risk.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

March 2023 / INVESTMENT INSIGHTS