March 2021 / INVESTMENT INSIGHTS

For or Against? The Year in Shareholder Resolutions

With environmental and social proposals in the spotlight, case-by-case insights were key to our decision-making.

Key Insights

- Many proposals, in particular those relating to environmental and social issues, demanded a nuanced approach to our voting rationale.

- In relation to environmental proposals in particular, improving the level and quality of disclosures by companies continues to be our primary objective.

- Distinct classifications of proposals provide a useful framework for understanding how we arrived at our voting decisions.

Within the context of growing demands on the private sector to constructively address the world’s environmental, social, and governance (ESG) challenges, shareholder resolutions can be an important tool to persuade companies to increase their focus on key societal challenges. The year 2020 presented a range of themes for consideration, and our approach to each was guided by careful attention to the end result within our well‑tested framework.

The Role of Proxy Voting in Stewardship

We see proxy voting as a crucial link in the chain of stewardship responsibilities that we execute on behalf of our clients. From our perspective, the vote represents both the privileges and the responsibilities that come with owning a company’s equity instruments. We take our responsibility to vote our clients’ shares in a thoughtful, investment‑centered way very seriously, considering both high‑level principles of corporate governance and company‑specific circumstances. Our overarching objective is to cast votes in support of the path most likely to foster long‑term, sustainable success for the company and its investors.

Our view is that the proxy vote is an asset belonging to the underlying clients of each T. Rowe Price investment strategy. This means that our portfolio managers are ultimately responsible for making the voting decisions within the strategies they manage. To fulfill this responsibility, they receive recommendations and support from a range of internal and external resources, including:

- The T. Rowe Price ESG Committee

- Our global industry analysts

- Our specialists in corporate governance and responsible investment

- Insights generated from our proprietary Responsible Investment Indicator Model (RIIM)

- Institutional Shareholder Services (ISS), our external proxy advisory firm

Prudent Use of Our Influence

Our proxy voting program is one element of our overall relationship with corporate issuers. We use our voting power in a way that complements the other aspects of our relationship with these companies. For example, other contexts in which we might use our influence include:

- Regular, ongoing investment diligence

- Engagement with management on ESG issues

- Meetings with senior management, offering our candid feedback

- Meetings with members of the Board of Directors

- Decisions to increase or decrease the weight of an investment in a portfolio

- Decisions to initiate or eliminate an investment

- On rare occasions, issuing a public statement about a company—either to support the management team or to encourage it to change course in the long‑term best interests of the company

However, in an environment where large institutional shareholders are often rated by third parties according to how frequently they vote against board recommendations, we wish to be clear—it is not our objective to use our vote to create conflict with the companies our clients are invested in.

Instead, our objective is to use our influence—through the various avenues listed above—to increase the probability that the company will outperform its peers, helping enable our clients to achieve their investment goals.

A proxy vote is an important shareholder right, but its power is limited to the one day per year when a company convenes its annual meeting. Influence—earned over time and applied thoughtfully—is a tool we use every day.

Varying Degrees of Regulation and Qualification

In various markets around the world, company shareholders are afforded the right to present items to be voted upon at the annual general meeting. However, these shareholder proposals are subject to varying degrees of regulation and qualification. In some markets, such as Japan, North America, and the Nordic region, filing requirements are minimal. As a result, it is common to see many resolutions submitted by individual and institutional investors in these markets. In other markets, where sponsors are required to have large, long‑term holdings to be eligible to submit proposals, shareholder resolutions are relatively infrequent.

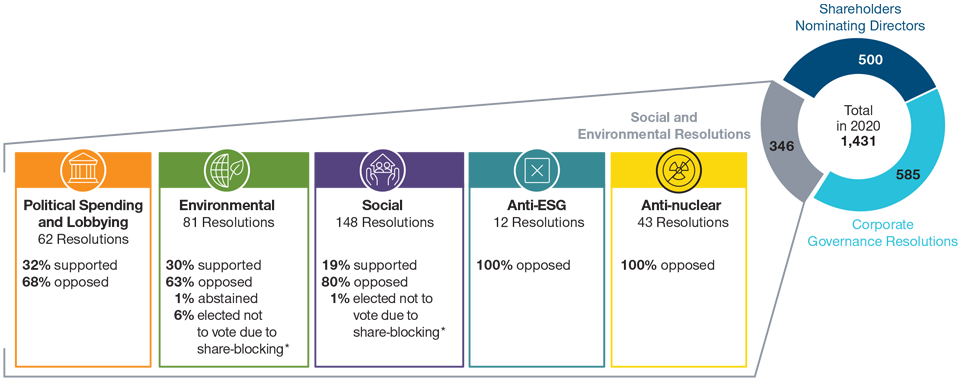

In 2020, the T. Rowe Price portfolios voted on 1,431 shareholder resolutions across all markets. Of those, 500 were situations where shareholders were nominating directors to a company’s board. Another 585 were resolutions asking companies to adopt a specific corporate governance practice. Here, we focus on the 346 remaining proposals that specifically addressed environmental and social (E&S) issues. We classify these proposals into five distinct categories as illustrated in Figure 1.

Shareholder Resolutions Voted on in 2020

(Fig. 1) Looking deeper into resolutions focusing on environmental and social issues

*Share‑blocking is a requirement in certain markets that impose liquidity constraints in order to exercise voting rights.

We generally do not vote in these markets.

Figures may not total 100% due to rounding.

As of December 31, 2020.

Source: T. Rowe Price.

Voting Framework: Principles‑Based or Case by Case?

When it comes to proxy voting issues, there is some debate as to the best approach: Is it best to look at each issue individually and consider the company’s circumstances or to apply a set of principles evenly across all companies? In our view, the answer is both.

There are many areas within proxy voting where a principles‑based approach can be implemented effectively. For example, our proxy voting guidelines are generally designed to promote an appropriate level of board independence, robust shareholder rights, and strong linkage over time between executives’ compensation and company performance. However, there are other areas where a case‑by‑case approach is necessary in order to achieve full alignment between our guidelines and our voting outcomes. One area where this is very much the case is shareholder resolutions.

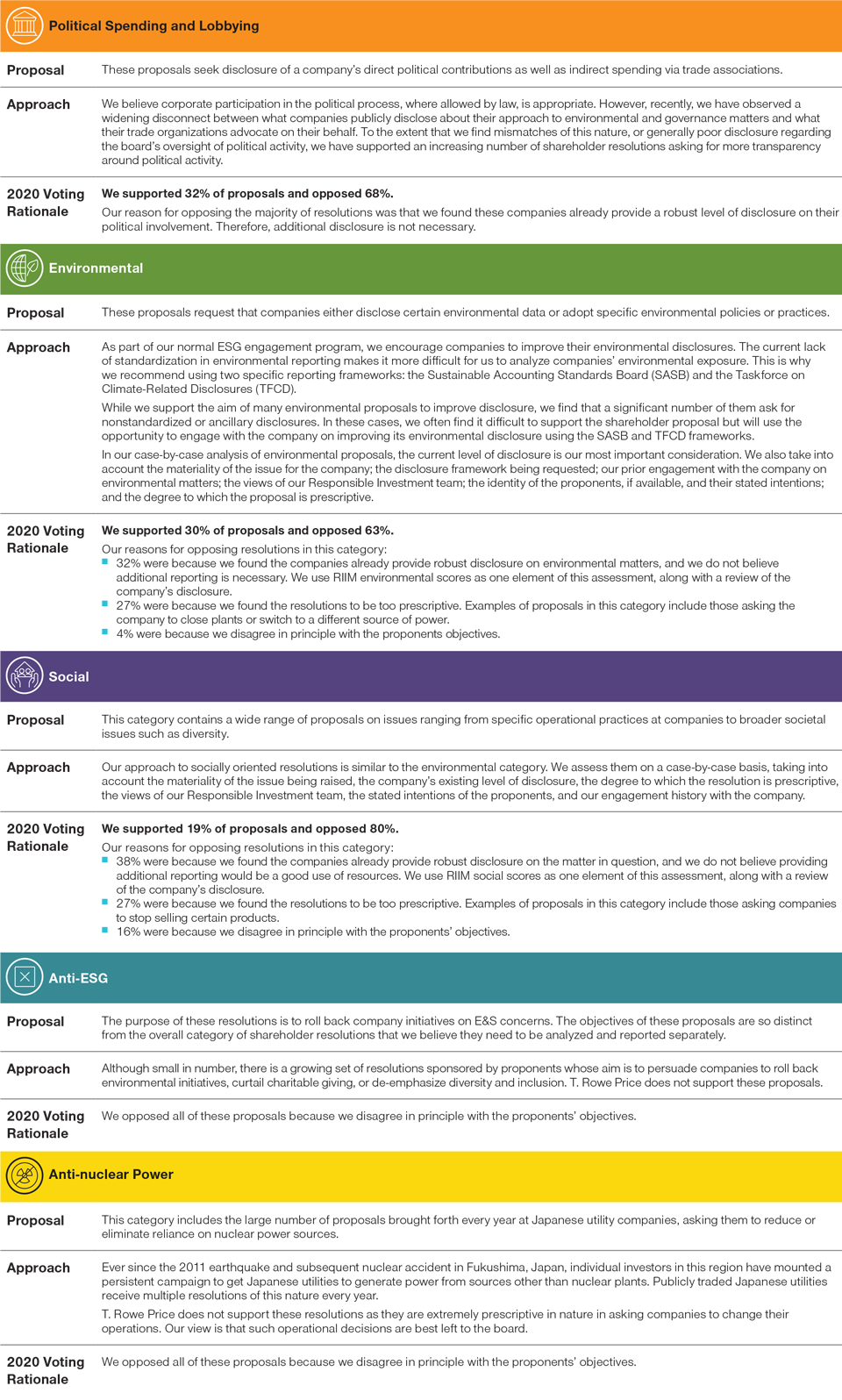

The main reason why shareholder resolutions are hard to implement with a principles‑based voting approach is because they are more nuanced than other proxy voting categories. For example, we employ an objective set of indicators to determine a director’s independence. It is a straightforward decision to vote against existing directors and indicate to the company that they should be replaced with independent board members. In the case of many shareholder proposals, the message to the company is not only does it need to make a change, but it also needs to employ a prescriptive method to do so. We often find ourselves agreeing with a proponent that a company’s environmental or social disclosure is inadequate. However, we do not always agree with the prescriptive remedy put forth by that proponent.

Understanding Our Voting Rationale

We classify environmental and social resolutions into five distinct categories

It is important to note that our overall framework for integrating ESG factors into the T. Rowe Price investment process—which includes proxy voting—is a research‑centered framework. Its purpose is to produce investment insights for our internal teams of analysts and portfolio managers. As a global asset manager serving as a fiduciary for clients with different perspectives, beliefs, time horizons, and investment goals, it is not our objective to build our investment strategies around a specific set of values. Instead, our objective is to use different lenses (environmental, social, ethical, and governance) to deepen our understanding of the investments held in our clients’ portfolios.

The Policy Formation Process at T. Rowe Price

Our approach to voting on social and environmental shareholder resolutions is one small part of our overall responsibilities related to proxy voting. This approach continuously evolves along with the overall corporate backdrop; it is informed by changes in regulation, improvements in corporate disclosure, campaigns by stakeholders, company‑specific events, and our investment professionals’ views on these matters.

The T. Rowe Price ESG Committee is made up of experienced investment professionals, including analysts and portfolio managers from both our Equity and Fixed Income divisions and our co‑heads of Global Equity. In addition, the membership includes cross‑functional expertise from internal legal counsel, business unit management, and investment operations. The committee is cochaired by our head of Corporate Governance and our director of Research for Responsible Investment. The ESG Committee meets in the first quarter of every year to review proxy voting activity from the year before, to reassess the suitability of our voting guidelines, and to consider adding to or amending the guidelines.

The tools we use to reassess the suitability of our voting guidelines each year include (a) a review of the previous year’s voting patterns, including an analysis of the cases where we decided to override our policies, and (b) an analysis of up‑and‑coming ESG issues, informed by our internal research and data from a variety of external sources, such as our proxy advisory service, our trade associations, and proponents of shareholder resolutions.

The robust discussions held each year by this committee ensure that the T. Rowe Price Proxy Voting Guidelines remain fit for purpose, incorporating changes in the global ESG landscape as they happen.

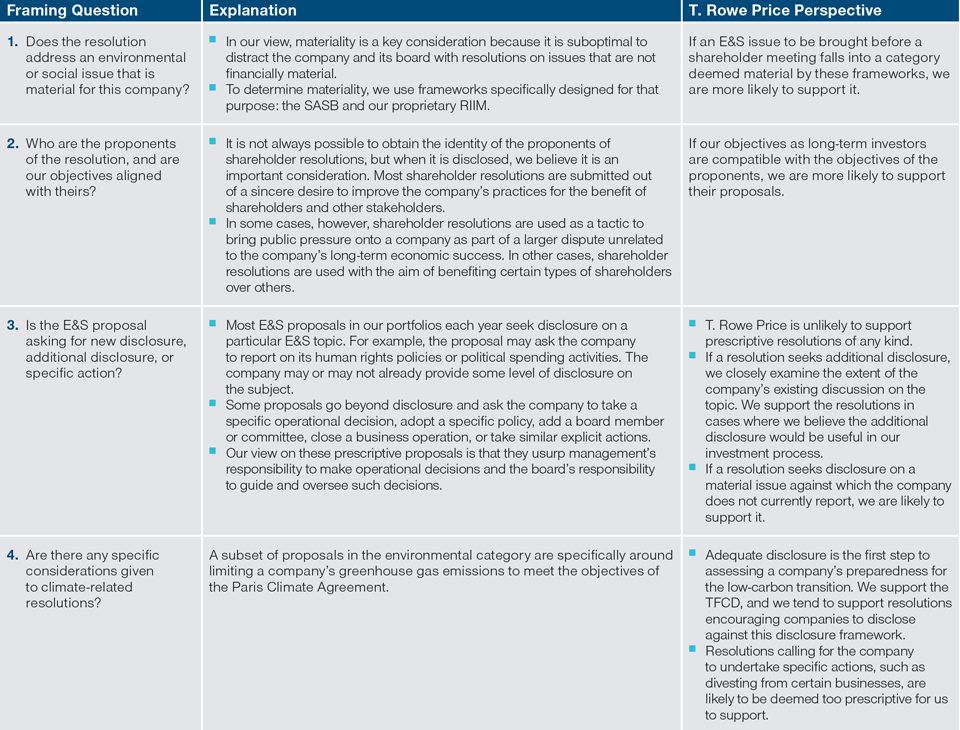

Voting Decision Elements

The following table details the specific considerations that we take into account when assessing E&S resolutions

Oversight of Proxy Voting and ESG at T. Rowe Price

Proxy voting is an investment function within T. Rowe Price. This is part of our service offering as investment advisers, and it is subject to the oversight of the Boards of Directors of the various T. Rowe Price investment advisers. The T. Rowe Price advisers have fiduciary responsibilities. It is the duty of the advisers to vote shares in portfolio companies solely in the interests of their clients, taking into account factors relevant to a long‑term investor.

The ESG Committee reports annually to the funds’ Boards of Directors. We provide a detailed overview of year‑over‑year changes in voting patterns, amendments to the voting guidelines, and a discussion of the management of potential conflicts of interest. We also provide a detailed analysis of our votes on social and environmental matters.

In addition to the funds’ Boards, which exercise direct oversight over the T. Rowe Price advisers, T. Rowe Price Group is a publicly traded corporation with a separate Board of Directors. The Group Board also has an interest in ESG matters in that it oversees the corporation’s ESG strategy, environmental footprint, human capital management, risk management, and other related functions. The ESG capability of the T. Rowe Price advisers is a strategic issue of interest to the Group Board. For this reason, the director of research for Responsible Investment and the head of Corporate Governance provide annual updates to the Group Board. This presentation focuses on our firm’s investment in our ESG capability: technology resources, talent, tools, training, and products managed under an ESG framework. (Our proxy voting activity is generally not part of the discussion, because oversight for such investment activities is the responsibility of the funds’ Boards.)

Conclusion

T. Rowe Price has dedicated significant resources toward building ESG expertise and insight. Consistent with our strategic investing approach, voting decisions on these matters are made using case‑by‑case analysis, taking into account the company’s particular ESG risks, opportunities, and disclosure.

The quality, intent, and utility of shareholder resolutions on ESG matters are highly variable at this time. Some well‑targeted resolutions are extremely helpful in persuading companies to strengthen their management of certain risks, leading to improved outcomes for investors. Other resolutions are not helpful—we would even call them harmful—if the objectives of the proponent do not align with economically oriented long‑term investors. This is why we believe the most responsible approach to voting such resolutions is to apply the thoughtful, investment‑focused framework we have discussed in this report.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

March 2021 / PODCAST

March 2021 / INVESTMENT INSIGHTS