June 2021 / GLOBAL ECONOMY

Surging Home Prices May Lead to Rate Hikes

The return of housing as an economic driver gives the Fed options.

Key Insights

- Booming U.S. house prices will likely give the post‑coronavirus recovery a very different complexion compared with that which followed the global financial crisis.

- The restoration of housing as a key economic driver may give the Federal Reserve more leeway to hike rates in the short to medium term.

- In the long term, overbuilding and slow population growth may keep the “natural” rate of interest low.

Home prices in the U.S. are booming and may continue to do so for a while yet. This will likely give the post‑coronavirus economic recovery a very different complexion compared with the recovery that followed the global financial crisis (GFC), when weak demand meant that growth was slow and interest rates continued to fall. The restoration of residential housing as a key economic driver may give the Federal Reserve more leeway to hike rates in the near to medium term—although its ability to raise rates over the longer term will likely be constrained by changing demographics.

The strength of the U.S. housing market is a matter of supply and demand. Following the GFC, the economy faced two major headwinds that kept activity in the American construction industries depressed for almost a decade. First, the crisis triggered broad‑based deleveraging by torpedoing both lenders’ and borrowers’ balance sheets: Lenders faced the dual headwind of increased regulatory scrutiny and stricter internal risk management requirements, which served to depress mortgage availability; borrowers, weighed down by poor employment prospects and negative equity in their houses, chose to repay their debts to reduce their leverage.

Second, there was a substantial overbuild of houses during the boom years prior to the GFC—an overbuild that would take almost a decade to digest.

In 2019, I argued that the clearing of the housing inventory overhang and improvement in household balance sheet meant that the era of household deleveraging had come to an end—and, therefore, that the belief among some economists that we had entered a period of “secular stagnation” was likely false. At the time, I expected activity in the construction sector to pick up quickly. The unexpected shock from the coronavirus affected the timing of that call, but it did not derail it: The construction sector is returning with a vengeance as, courtesy of fiscal transfers and rising savings rates, household balance sheets have improved further.

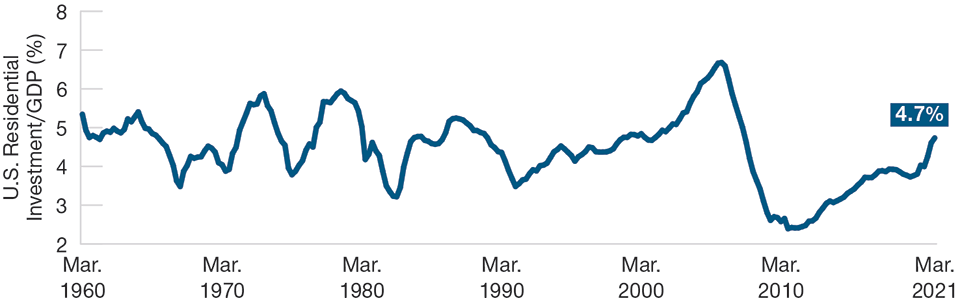

The Construction Industry Strikes Back

(Fig. 1) Residential investment has been rebounding strongly

As of March 31, 2021.Source: The Bureau of Economic Analysis.

The Coronavirus Has Fueled Demand for New Homes

The coronavirus has fueled demand for housing in two ways: First, because the pandemic‑induced fall in interest rates has made owner‑occupied housing more affordable; and second, because the lockdown has made many existing householders yearn for more space. Combined, these two factors have reinvigorated the demand side of the residential housing market.

On the financing side of the ledger, the combination of high cash balances and healthy bank balance sheets imply that the supply of mortgage financing is unimpaired: Banks have a lot of low‑yielding assets on their balance sheets in the form of cash and, consequently, are seeking to accumulate slightly higher‑yielding assets such as mortgages. While banks continue to operate under tighter regulatory scrutiny, they appear to be in a good position to support the recovery of the housing market.

For mortgage lending to accelerate further, economic uncertainty and unemployment have to fall—both of which facilitate risk‑taking by banks. We expect both to occur in tandem with the vaccine rollout and the economic reopening.

On the supply side of the housing market, after a decade of subdued construction, the housing inventory overhang had already cleared prior to the coronavirus recession. As the demand for additional living space accelerated during the pandemic, the number of unoccupied homes in the U.S. fell to a level that is low by historical standards.

Thus, construction should reengage as a strong cyclical driver, and in my view, the dynamics of the housing sector will be very different compared with the dynamics that followed the GFC. The restoration of construction as a key economic driver will likely add power to the post‑pandemic recovery and may pause—if not end—talk of “secular stagnation.”

Two Key Challenges to the Housing Recovery

There are two key challenges to the U.S. housing recovery story. The immediate near‑term challenge arises from the fact that the number of people per household in the U.S. fell markedly during the pandemic and currently sits close to its historic low—making it possible that some of the demand for housing has already been satisfied. Even if this is the case, however, the stock of vacant housing remains low, and construction will need to reestablish an appropriate inventory of vacant housing.

The second, and more significant, challenge arises from the changing demographics. While home construction should be strong for some time as inventories rebuild, it will eventually need to settle at a pace that is slower than that of the boom times of the mid‑2000s. As housing investment settles to reflect the demographic headwind, its potency as an economic driver will likely diminish.

Overall, I believe that improved demand for housing will continue to support home prices, and the low stock of vacant housing will keep construction activity buoyant. Altogether, this will raise inflationary pressures and may give the Fed more scope to hike rates.

Over the next couple of years, however, it is likely that the housing inventory restocking will be completed and there will be some overbuilding as the macro impact of demographics will be slow to register with households and construction companies. In turn, this may keep the natural rate of interest—also known as the r*—low relative to history.

IMPORTANT INFORMATION

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45-106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

© 2023 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

June 2021 / GLOBAL ECONOMY

Nikolaj Schmidt is a chief global economist in the Fixed Income Division of T. Rowe Price. Prior to joining the firm in 2015, he worked as a director of Economic Research at Pharo Management. Nikolaj also held a position at Goldman Sachs and the Danish Ministry of Finance. He earned a master's degree in finance and economics at the London School of Economics and a Ph.D. in finance at the London School of Economics and Political Science.