June 2021 / INTERNATIONAL EQUITIES

Gains Still to Be Found in Chinese Equities

Corporate earnings will likely be the focus after a post‑pandemic recovery.

Key Insights

- 2021 can be viewed as a year of normalization for China’s gross domestic product (GDP), earnings growth, financial markets, and policy after the preceding pandemic disruption.

- The U.S.‑China relationship remains competitive in nature, though increased dialogue and a more predictable approach may lower tail risk and uncertainty.

- A broader economic recovery is expected to take hold in 2021 that could potentially lead to divergent sector performance from Chinese equities.

China’s economy is on the right track to recovery in 2021. We expect the Chinese consumer to play a bigger role this year, thanks to pent‑up demand. Successive holidays and festivals have been accompanied by improving consumer confidence. Residential property, one of the first sectors to recover, remains well supported. Sectors exposed to developed markets economic recoveries might also benefit, as well as export manufacturers leveraged to global trade.

We believe the COVID‑19 vaccination rollout should facilitate a further rebound in those business and consumer services that have been lagging, such as food, hotels, entertainment, and personal services. Though the country’s international borders remain shut, domestic air travel and tourism have rebounded strongly. During the Labor Day holidays in early May, the number of domestic tourist trips reached a record 230 million, 3.0% more than in 2019.1 As China ramps up its vaccination program, we should see a more visible path for opening international borders in 2022.

By contrast, COVID‑19 beneficiaries— including some technology companies as well as companies related to China’s infrastructure spending, such as construction machinery—may face a tougher time as earnings comparisons are made with the previous year. 2021 can be viewed as a year of normalization for GDP, earnings, markets, and policy.

A Correction and Consolidation in Equities

China’s early and sustained economic recovery from the coronavirus pandemic was reflected in a strong performance by the CSI 300 Index last year, which rose 27% in 20202 compared with 16.3% for the S&P 500. The broader A‑share market, represented by the Shanghai Composite Index, only rose 13.9%,2 however, close to the return of the average developed economy stock market. There was clearly a big gap in 2020 performance between China’s mega‑cap growth stocks and internet giants and A‑shares generally. And while the A‑share market overall still did well, 50% of stocks actually fell last year. In particular, large‑cap stocks (as represented by the MSCI China All Shares Large Cap Index) outperformed small‑caps (as represented by MSCI China All Shares Small Cap Index) by 7.33% last year.3

This year, we have seen Chinese equities correct from their mid‑February peak, as markets have pulled back on higher U.S. bond yields, risk‑off sentiment due to news flow around U.S.‑China competition, and renewed travel and quarantine restrictions during the Chinese New Year.

Looking ahead, we see China’s stock market becoming more earnings‑driven this year after a solid post‑pandemic economic recovery. With liquidity no longer lifting all boats, we believe stock selection will be paramount moving forward. Importantly, earnings estimates are looking favorable. Consensus corporate earnings for 2021 are expected to increase 24% for companies in the MSCI China Index and 23% for those in the large‑cap CSI 300 Index, with further gains of 14% and 13%, respectively, in 2022, according to analyst estimates compiled by I/B/E/S.

Overall, 2021 is likely to be a year of normalization. As the economic recovery broadens out, more sectors are likely to see stronger earnings growth. This, combined with tighter liquidity, means that the wide valuation divergence we saw last year could potentially reverse. We are already seeing part of that reversal happen, especially for some of the more crowded growth names and thematic stocks.

Economic Policy on Hold

China’s leaders announced more prudent monetary and fiscal policies at the annual National People’s Congress (NPC) in March. A conservative GDP growth target of “over 6%” was set for 2021, which should be easily achievable given the low pandemic base. Beijing believes it has done enough to reflate the economy, and policymakers may adopt a “wait‑and‑see” approach in the coming quarters. Investors, however, were disappointed by the lack of new stimulus. Some worry that policy might be tightened prematurely, as the government seeks to balance supporting economic recovery with the longer‑term need to contain financial risks. The chance of aggressive tightening is quite low, however.

Importantly, China has ample fiscal and monetary space to reverse course quickly should the economy falter. The People’s Bank of China (PBoC), China’s central bank, kept monetary policy broadly neutral during the recovery from the coronavirus, with no change in interest rates for 12 months. It, therefore, has policy ammunition in reserve.

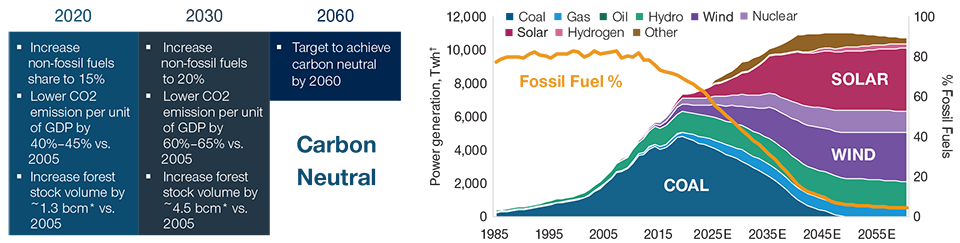

China’s Planned Move Away From Carbon

(Fig. 1) Fossil fuels as a percentage of primary energy is falling

As of September 30, 2020.

*bcm: Billion cubic metres.

† twh: TeraWatt Hour(s).

Source: Alliance Bernstein.

China’s Long‑Term Targets

A key focus of the NPC’s five‑year economic plan (2021–2026) is President Xi Jinping’s “dual circulation” theory. This seeks higher‑quality growth through supporting domestic markets, innovation, and reform. Beijing views boosting domestic demand, upgrading supply chains, and achieving greater self‑sufficiency in key technologies as the best ways to hedge against external uncertainties and challenges.

Innovation is becoming the key driving force for policymakers. Beijing is looking to actively shift its competitive advantage away from a labor-intensive model to one more focused on engineering abilities. This is being helped by an increasingly educated workforce. While China’s demographic dividend is coming to an end, education is taking up the slack with approximately 1 million college students graduating every year.

Under dual circulation, China may also have better protection against global economic shocks and the international trade cycle. In terms of geopolitics, we believe Beijing would prefer to cooperate with other countries rather than engage in geopolitical rivalry. We expect China to continue to open up its economy to overseas companies while at the same time pursuing economic and financial reform. The U.S.‑China relationship will likely remain competitive in nature, though increased dialogue and a more predictable approach may lower risk and uncertainty.

President Xi also announced more details of the plan to transition to clean energy and reduce net carbon emissions to zero by 2060 (Figure 1). China accounts for 30% of global industrial output, and its efforts will likely contribute meaningfully to global carbon reduction, with a sharp focus on renewable sources of energy.

China is taking the lead in the global transition away from carbon, producing 70% of the world’s solar panels, 50% of its electric vehicles, and one‑third of all wind turbines. China has also established a prominent position in the global supply chain for the raw materials essential to electrification, such as rare earth elements, cobalt, lithium, and copper.

In our view, China is well positioned to be a leader in renewables and green energy (Figure 2). Being an importer of traditional energy today, a future that is driven by renewable sources of energy could allow China to become more self‑sufficient and, thus, serve an economic goal as well as a social goal—by improving living standards for Chinese people who have been subjected to high levels of pollution in their history. China’s aim to achieve carbon neutrality by 2060 will potentially achieve a key social outcome and allow China to be less dependent on energy imports.

China Leads the World in Green Energy Investment

(Fig. 2) Share of green energy investment in new capacity 2020–2050E

As of December 31, 2020.

Source: Bloomberg Finance L.P.

Focusing on Inefficiencies to Uncover Future Beneficiaries

Given the speed of change and the inefficiencies that present themselves in the market, we believe China remains a fertile ground for good stock selection. There are pockets of speculative bubbles, such as in some thematic stocks, but we are still able to find very attractive opportunities in the supply chains that support these industries. The transition away from a carbon‑intensive economy to a more sustainable economy offers a tailwind to industrialization, and we are finding very attractive value in some industrial businesses.

We see consumption as another important pillar of growth, from the government’s perspective, with a focus on quality growth. These tend to be companies that offer compounding growth opportunities as well as some companies that are undergoing a positive product cycle. The shift of domestic demand from foreign brands to local brands provides another tailwind. With this favorable backdrop, we believe homegrown businesses can take a step further and potentially expand to become global leaders.

We believe our greatest advantage is that many investors are focused on mega‑cap stocks and have a very short‑term view of the market. While the top 100 mega‑cap stocks (roughly 70% of the MSCI China Index) are widely owned by local and foreign investors, that only represents 2% of the total Chinese universe.4 We believe there is a real advantage in going beyond the mega‑caps. Since 2016, large‑caps have generated strong relative return versus the market, but that has mostly been driven by multiple expansion. With large‑caps now trading at historically high premiums (versus small‑caps), we believe that a reversal is justified and investors should not rely on the same playbook going forward in this new environment.

Importantly, with China having over 5,200 listed companies, there is a huge opportunity set available to investors. But many investors are focused on stocks with a market cap of USD 30 billion+. On average, 60% of active Chinese funds are invested in those 2% of stocks, while the remaining 98% remain under‑explored. We believe this is where you may find mispriced opportunities and potential hidden gems.

IMPORTANT INFORMATION

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45-106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

© 2023 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

23 June 2021 / GLOBAL FIXED INCOME

Wenli Zheng is the portfolio manager of the China Evolution Equity Strategy in the International Equity Division. He also co-manages the Greater China portfolio of the International Small-Cap Equity Strategy. Wenli is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Hong Kong Limited.