October 2023 / ENVIRONMENTAL, SOCIAL, AND GOVERNANCE

Counting the Cost of Biodiversity Loss

Addressing the challenge of integrating biodiversity into investment analysis

Key Insights

- Preserving biodiversity is essential to the long‑term social and economic development of humanity.

- Data on biodiversity impact remain scarce with the universe of issuers sharing measurable data points on biodiversity outcomes limited.

- In the absence of data that measure the biodiversity impact of investments, proprietary research and analysis is essential.

The natural world is undergoing unprecedented, exponential deterioration,1 with human activity being the principal driver.2 Consequently, the rates of species loss are unparalleled in human history. Research shows that one million species are now threatened with extinction within the next few decades,3 setting Earth on an alarming trajectory for what biologists warn could be the sixth mass extinction.4

The Importance of Preserving Biodiversity

We believe that preserving biodiversity is essential to the long‑term social and economic development of humanity, and also that biodiversity loss and climate change are fundamentally interlinked twin crises.

Natural carbon sinks (both on land and underwater) play a key role as they absorb significant amounts of human‑generated greenhouse gas (GHG) emissions. In turn, climate change, whether through changing rainfall patterns, extreme weather events, or ocean acidification, is having a materially negative impact on biodiversity. Furthermore, biodiversity is so vital to maintaining a sustainable future for humanity that its loss undermines 80% of the United Nations Sustainable Development Goals (SDG) targets relating to poverty (SDG 1), hunger (SDG 2), health (SDG 3), water (SDG 6), cities (SDG 11), climate (SDG 13), oceans (SDG 14), and land (SDG 15), whereas biodiversity preservation and restoration support the delivery of targets for the SDGs related to education (SDG 4), gender equality (SDG 5), reducing inequality (SDG 10), and peace and justice (SDG 16).

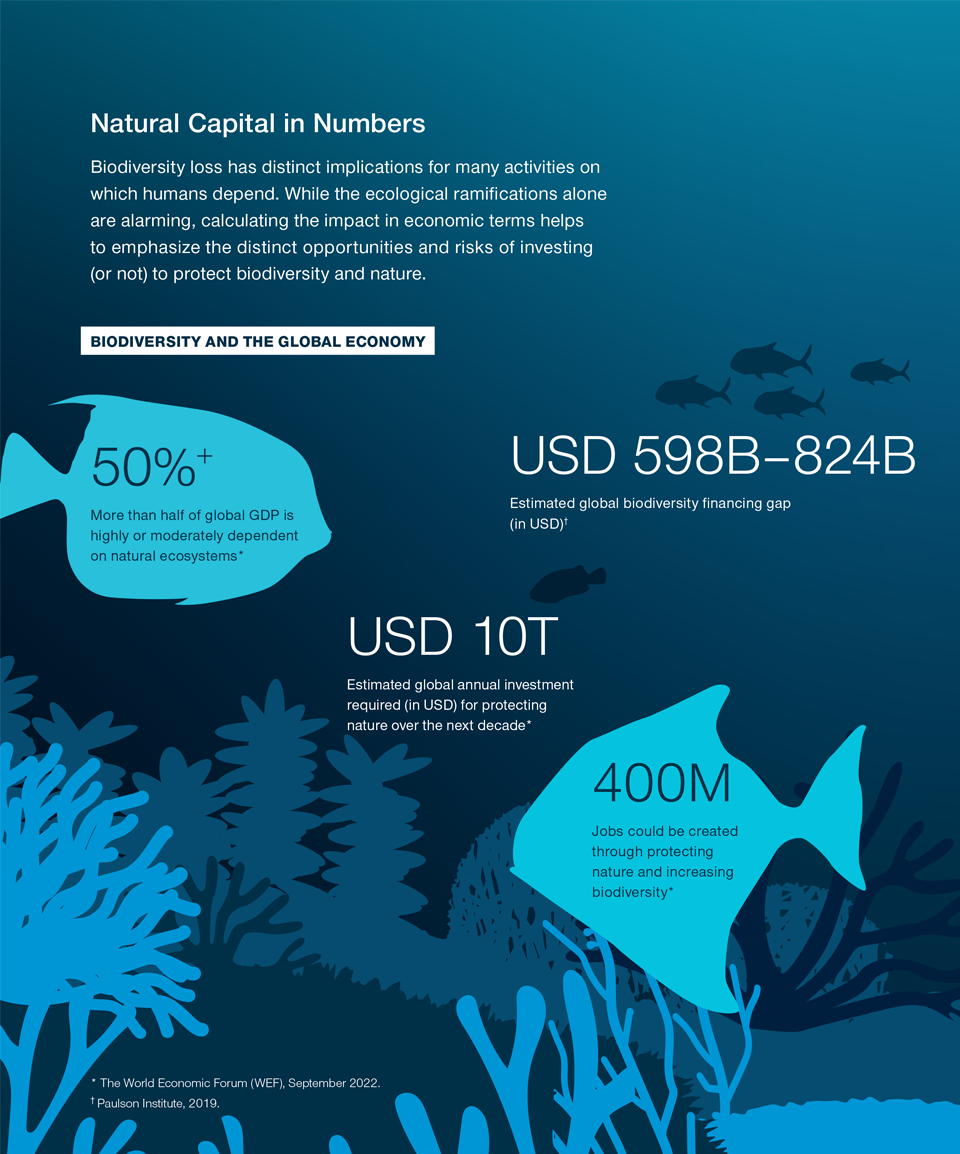

To contextualize the cost of biodiversity decline in economic terms, the World Economic Forum (WEF) states that over 50% of global gross domestic product is highly or moderately dependent on natural ecosystems.5 This is unsurprising since biodiversity is an implicit enabler asset that underpins many human activities.6 For example, pollination by bees and other pollinators is vital to global food security—75% of the world’s food crops rely on it.7 According to the WEF, investing in opportunities that directly address the threats to biodiversity has the potential to generate up to USD 10.1 trillion in annual business value and 395 million jobs by 2030.8

Integrating Biodiversity in Investment Analysis

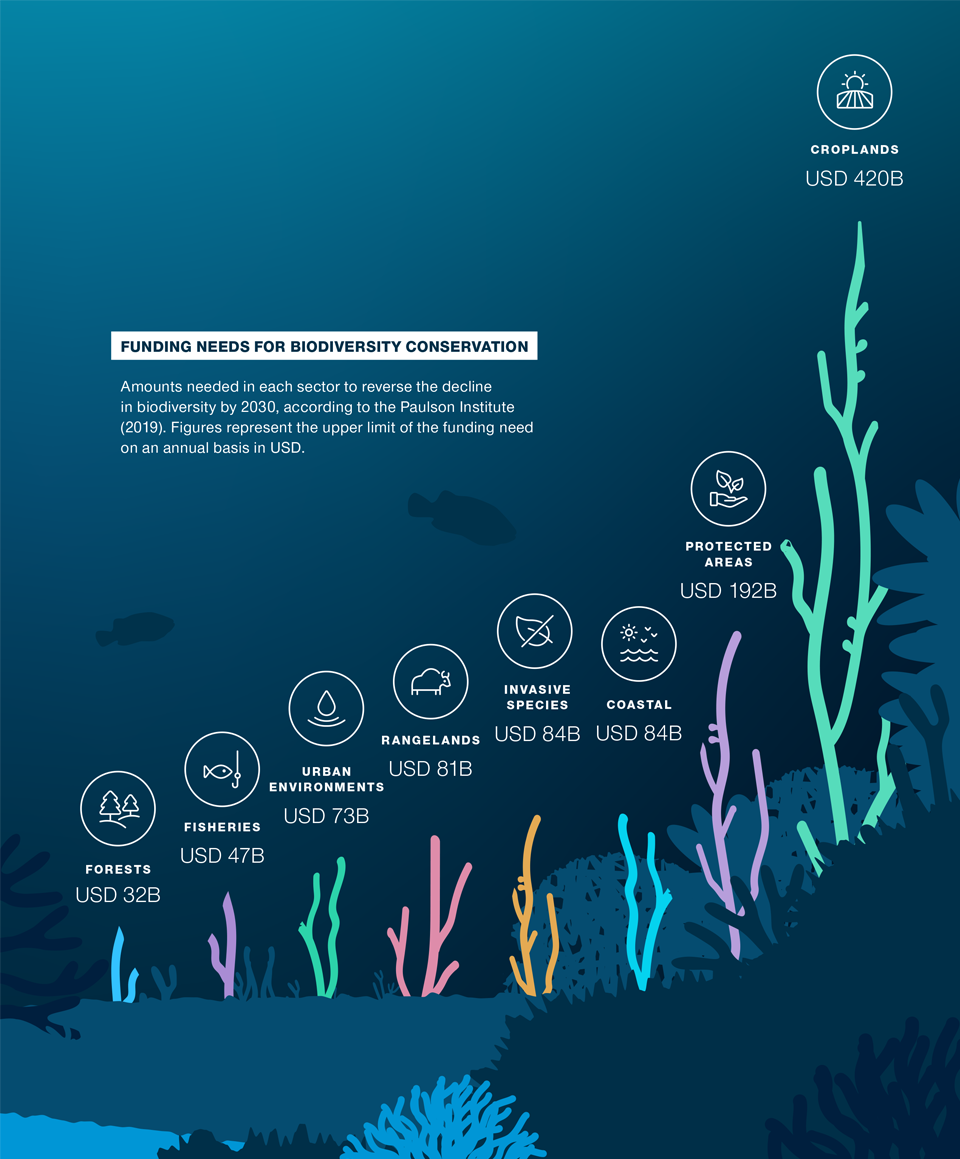

With this in mind, we believe that a diligent, long‑term investment strategy should consider biodiversity risks and opportunities. This does, however, present a variety of challenges to investors. For one, most investors are inherently reliant on quantitative data to inform the relative performance of corporate, sovereign, or municipal issuers. Data on biodiversity impact remain scarce, and while we are seeing a major uptick in corporate, sovereign, and municipal issuers setting goals concerning regenerative agriculture, climate, and deforestation (all factors that directly impact biodiversity), the universe of issuers sharing measurable data points on their actual biodiversity outcomes (such as Mean Species Abundance or Species Threat Abatement and Restoration) is limited. Moreover, third‑party data sets for biodiversity remain relatively nascent, and where available, they are often very reliant on significant assumptions to deal with data gaps. Like many of our investee companies, we are looking to the development of frameworks like the Taskforce on Nature‑Related Financial Disclosures (TNFD) for guidance to enhance our measurement of nature‑related risks, opportunities, and financial implications. Comparable and consistent reporting will be a cornerstone for engagement and accountability in the space.

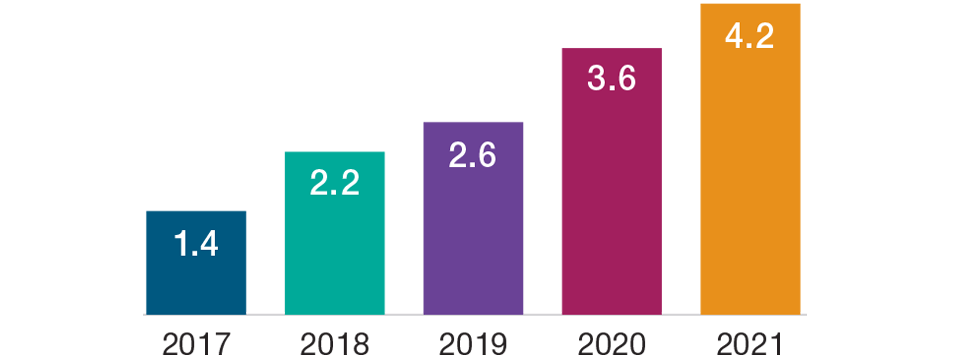

Indeed, we can look at the trend for climate disclosures for clues on how quickly we might expect more formalized nature‑related information from corporates (Figure 1).

Average Number of TNFD‑aligned Disclosures per Company by Fiscal Year

(Fig. 1) Average annual growth rate of 32%

As of October 2022.

Source: Taskforce on Climate‑related FinancialDisclosures 2022 Status Report, based on 1,370 companies surveyed.

With TNFD recommendations only released in 2023, it could be several years before investors have sufficient information on biodiversity impact for a wider investment universe—time that the natural world simply does not have.

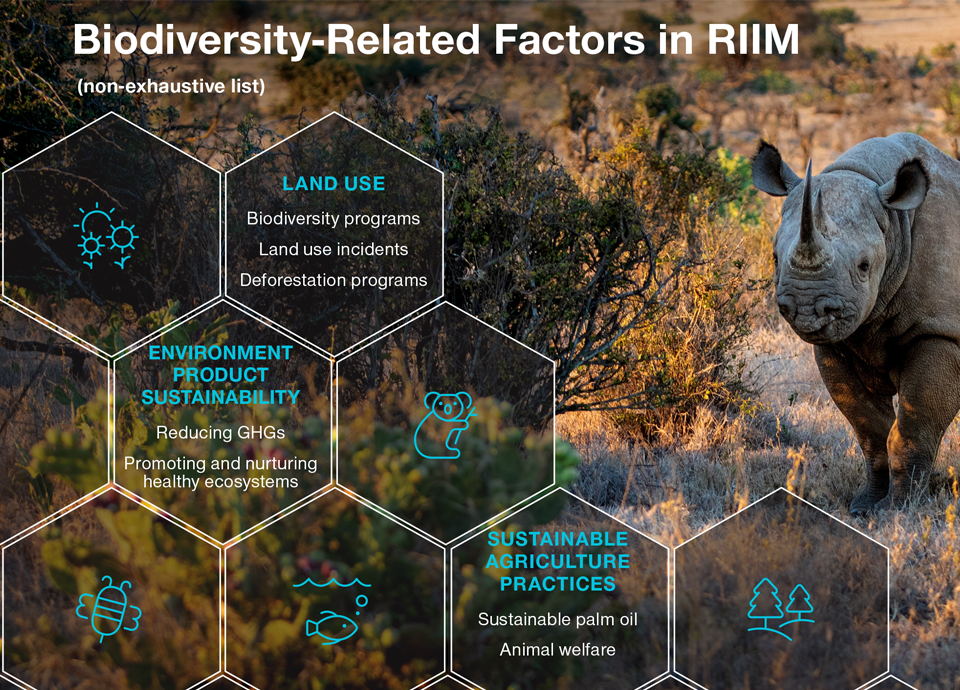

In the absence of data that measure the biodiversity impact of investments, what can investors do? We leverage quantitative and qualitative inputs that are drivers of biodiversity in our proprietary Responsible Investing Indicator Model (RIIM). Key parameters in sovereign RIIM include terrestrial biome protection, protected areas, and species habitat—all of which are inextricably linked to biodiversity outcomes. Our responsible investing analysts undertake in‑depth research into corporates, which includes consideration of sectors and business activities that are either highly dependent or heavily impactful on biodiversity. This evaluation, alongside a variety of other fundamental, technical, and ESG metrics, are inputs that may be used by our investment teams in their capital allocation decisions. Also, as part of our wide range of investment products, T. Rowe Price offers products with specific ESG objectives and/or characteristics.

During 2022, the TRPA responsible investment team undertook analysis at the corporate level that included assessments of biodiversity risks and opportunities. Among them was an analysis of Brazil’s listed meat producers and the impact they have on Amazonian deforestation. Further, we engaged with a variety of sovereign, supranational, and agency issuers and corporates on biodiversity.

Some securities we evaluate also feature specific biodiversity factors. In 2022, these included Uruguay sovereign bonds, which explicitly tie cost of capital to biodiversity targets, and International Bank for Reconstruction and Development/World Bank supranational bonds that promote wildlife conservation. The World Bank’s Wildlife Conservation Bond, often referred to as the Rhino Bond, is an innovative, outcome‑driven fixed income instrument that channels funds to biodiversity conservation.9

ENGAGING WITH THE WORLD BANK ON ITS RHINO BOND

In 2022 we undertook an evaluation of the World Bank’s Wildlife Conservation Bond, often referred to as the Rhino Bond. TRPA’s emerging market debt, global impact credit, and responsible investing teams collaborated on an ESG engagement with the World Bank to request and encourage continued impact reporting, with tangible and quantifiable metrics related to the security.

The objective of our engagement was to reiterate our support for nature‑based contingent capital instruments, as well as our desire to partner with the World Bank across its dual mandates of ending extreme poverty and promoting shared prosperity and greater equity.

We provided very specific feedback on impact metrics for the Rhino Bond, and the World Bank recommitted to reporting these, with credible third‑party verification. T. Rowe Price will look to track progress based on ongoing public disclosure.

T. Rowe Price communicated why we felt it was imperative that the World Bank set the tone with the Rhino Bond and similar issuance. Specifically, the credible, tangible quantification and third‑party verification elements of, in this instance, black rhino population growth were key for T. Rowe Price from a biodiversity perspective. Additionally, we believe there is a co‑benefit around employment creation and education.

The World Bank welcomed the feedback and recommitted to public disclosure of the impact metrics we asked for, which we aim to track.

Following the engagement, we will continue to evaluate the World Bank’s use of its capital market presence and activities to address its twin mandates.

URUGUAY’S SUSTAINABILITY‑LINKED BOND

In 2022, our responsible investing team partnered with our emerging market debt investment team to meet with representatives of the Uruguayan government regarding its inaugural Sustainability‑Linked Bond (SLB). The engagement focused on biodiversity and GHG reduction. We believe these twin crises are interlinked and that sovereigns are a key part of the solution.

In October 2022, Uruguay brought to market a first of its kind SLB, which had two key performance indicators focused on GHG reduction and native forestry.

We leveraged our engagement(s) and a variety of proprietary ESG integration tools, including our sovereign RIIM framework and separate ESG‑labelled bond assessment models, in assessing the SLB.

Our assessment of Uruguay’s credit and sustainability fundamentals; its ambition in setting stretching, yet impactful, sustainability targets; and elements of the post‑issuance reporting (which we believe enhance credibility and transparency) was favourable. In our opinion, actively tying a sovereign’s cost of capital to relevant sustainability metrics, which over time could impact creditworthiness, aids in promoting well‑functioning capital markets.

Information presented is that of T. Rowe Price Associates, Inc. only. The securities identified and described are for illustrative purposes only, do not represent recommendations, and do not necessarily represent securities purchased or sold by T. Rowe Price. No assumptions should be made that the security analysed, or other securities analysed, purchased, or sold, was or will be profitable. The material is not recommendation to buy or sell any security and is not indicative of a company’s potential profitability. Information is subject to change.

Biodiversity to Remain in the Spotlight

Looking ahead, we are encouraged by the outcome of the Kunming‑Montreal COP15, namely a new Global Biodiversity Framework (GBF) that includes objectives for conservation, sustainable use, access, and benefits sharing and covers all the main drivers of biodiversity loss (land and sea‑use change, exploitation of organisms, climate change, pollution, and invasive species). While it was notable that the framework did not ultimately include the term “nature positive,10” the headline “30 by 30” target11 aims to ensure that by 2030 at least 30% of areas of degraded terrestrial, inland water, and coastal and marine ecosystems are under effective restoration. Much of the GBF is open to interpretation and is by no means all‑encompassing, yet COP15 has certainly put biodiversity firmly in the spotlight—and has gone some way towards raising awareness of the issue among governments, corporates, municipal issuers, and investors alike.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Tongai Kunorubwe is the head of environmental, social, and governance in the Fixed Income Division.