December 2020 / GLOBAL MARKET OUTLOOK

China Market Outlook 2021

Improving fundamentals are likely to be sustained

Key Insights

- China’s economic recovery from the coronavirus has not gone unnoticed. It is the first major economy where both supply and demand are close to normalizing.

- Though the U.S. and China may remain strategic competitors, more dialogue between them can better manage the risks, allowing economic relations to improve.

- We are positive on the outlook for the fundamentals for Chinese equities in 2021, when a more consumer-led recovery is expected to take hold.

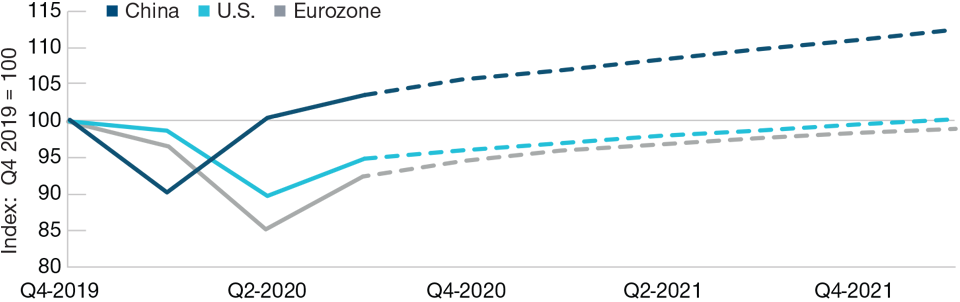

Thanks to its rapid control of the coronavirus, China is the only major economy that is expected to post positive economic growth this year, according to the Organization for Economic Cooperation and Development, which recently raised its 2020 gross domestic product (GDP) growth forecast for China to +1.8% from the -3.7% projected in June. Solid economic data since September suggest that an even higher growth number is feasible, closer to 3.0%. The second‑quarter GDP report in July distinguished China as the first major economy to return to positive growth, having encountered the pandemic three months earlier than elsewhere (Fig. 1).

Since the summer, the economic data confirm that China continues to lead the post-coronavirus global recovery. We attribute this to three factors: (i) after an early but brief national lockdown, China introduced significant fiscal stimulus via increased infrastructure spending, which began to boost growth significantly in the second half of 2020; (ii) after the lockdown, residential property recovered surprisingly quickly; and (iii) Chinese exports performed better than expected even as global trade continued to weaken.

China Leads the Global Recovery From Coronavirus

(Fig. 1) Bloomberg consensus real GDP (forecasted after Q3 2020)

As of October 6, 2020.

Sources: Refinitiv and Credit Suisse (see Additional Disclosures).

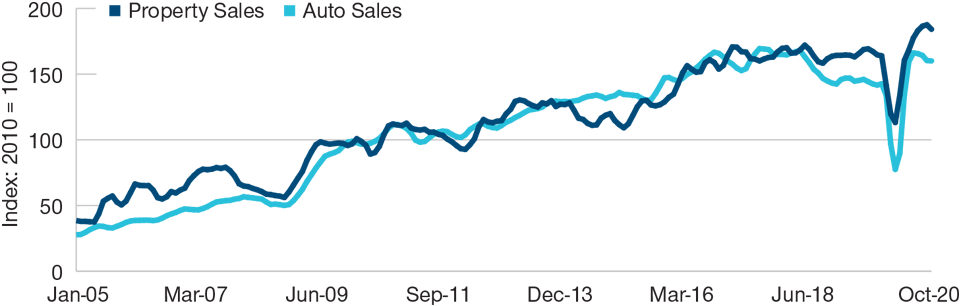

China’s Property and Auto Cycles Have Been Closely Linked

(Fig. 2) Property and auto sales

As of October 6, 2020.

Sources: Emerging Advisors Group, and CEIC.

Momentum continues to build as we approach 2021. Industrial output in September, for example, stood 7% above its pre-pandemic level. In our view, China has done enough to successfully reflate its own economy. One consequence of China’s early recovery is that expectations of fresh stimulus have been dampened. At the same time, there is no sign that the government will tighten policy prematurely. Rather, it appears to be taking a “wait and see” approach that could prevail for the next couple of quarters.

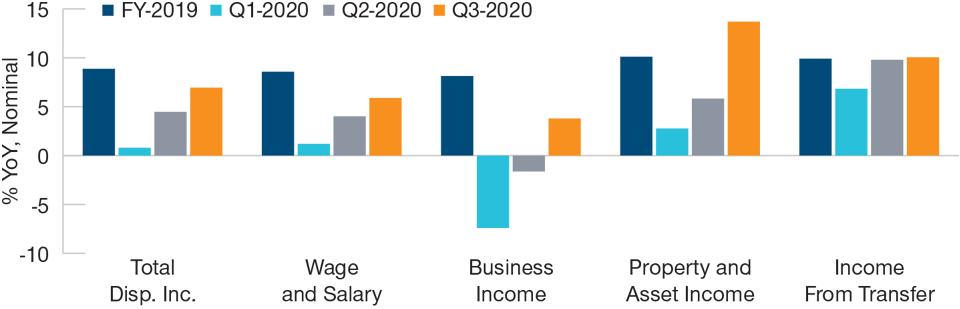

The durability of the recovery in 2021 will require a shift in the sources of growth toward the consumer, including those consumer services that suffered most from the pandemic. The prospects for consumer demand in 2021 look good. Auto sales, a key gauge of consumer confidence, are well above 2019 levels (Fig. 2). Successive holidays and consumer festivals saw improving consumer confidence and pent-up demand. Residential property has rebounded, supported by a recovery in household income (Fig. 3). We expect the consumer to play a bigger role in driving China’s economic growth next year.

Monetary Policy on Hold, Currency Firm

The People’s Bank of China (PBoC) has maintained a broadly neutral monetary policy during the economic recovery from the coronavirus. Many had expected more aggressive easing, including cuts in key lending rates. We think the central bank sought to keep some ammunition in reserve, which has so far not been needed. Bond yields have risen gradually since the summer and may be close to peaking. In October, index compiler FTSE Russell said it would include Chinese sovereign bonds in its World Government Bond Index. Index inclusion should draw more foreign assets into Chinese government bonds and also support the renminbi. We believe favorable conditions for sovereign bonds and the renminbi will continue in 2021, providing a supportive backdrop for equity markets.

Growth in Wages and Household Incomes

(Fig. 3) Growth in nominal disposable income versus fiscal year 2019

As of October 29, 2020.

Sources: CEIC and HSBC Global Research.

Fifth Plenum Plots China’s Course Over Next 15 Years

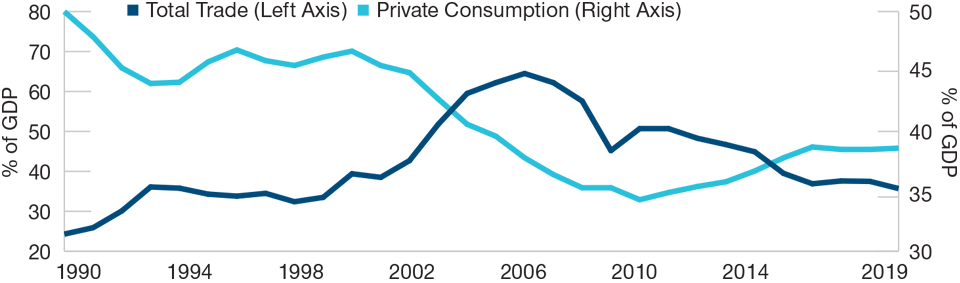

In October at the fifth plenum meetings in Beijing, China’s party leaders outlined their 14th five-year plan for economic and social development. Guidelines for the plan focused on President Xi Jinping’s “dual circulation” theory, sustaining higher‑quality growth through encouraging domestic markets, innovation, and reform. Beijing views boosting domestic demand, upgrading supply chains, and seeking self‑sufficiency in key technologies as ways to hedge against external uncertainties and challenges. As a large, continental economy, China must depend mainly on internal drivers for future growth, just like the U.S.

Dual circulation means China recognizes it is less vulnerable to the global economy and international trade cycle than before (Fig. 4). Access to China’s huge and relatively stable domestic markets remains highly desirable for overseas companies and is a priority objective for many. Political tensions alone are not going to keep them away. Dual circulation also implies the need for greater reliance on homegrown technology, and we expect a trend toward greater spending on research and development within capex budgets in the coming years. In the technology field, we believe China would prefer to cooperate than to engage in geopolitical strategic rivalry and may try harder in the future to achieve this.

China’s Economy Is Becoming Much Less Trade Dependent

(Fig. 4) Total trade and consumption as percentage of GDP

Data shown is as of December 31, 2019. Source as of August 27, 2020.

Sources: TS Lombard and CEIC.

In addition to the next five-year plan, President Xi also updated the longer‑term modernization targets for 2035 that were first introduced in 2017. China’s per capita GDP is to be raised to the level of “moderately developed countries” 15 years ahead of the original target set by Deng Xiaoping in the 1980s. This will require GDP growth to average around 4.8%, doubling the size of the economy. This will be no easy task given China’s well-known medium-term structural problems of an aging population, rising debt burden, and lower potential growth as resources shift into lower‑productivity services. But the 2035 target is not out of the question. Mainland economists expect China’s trend or potential growth to slow gradually from its current rate of 6%–7%, and a sharp collapse is a low‑probability scenario.

Ant Group IPO Delay Will Not Halt Rise of Chinese Fintech

In early November, Ant Group, owned by internet giant Alibaba, postponed its heavily oversubscribed initial public offering (IPO) just two days before launch. Investors were initially shocked, but some delay is a small price to pay if it means a better‑regulated fintech industry. Fintech has begun to evolve rapidly in China, and until now the regulators had adopted a liberal approach, first observing the behavior of the big private tech companies. China wants to avoid the mistakes of the peer-to-peer (P2P) lending platforms when domestic investors lost over USD 100 billion as many unregulated platforms collapsed.

The Ant deal’s heavy oversubscription revealed the strong attractions that leading Chinese tech/new economy companies hold for global investors. This is unlikely to be impacted by one delayed IPO, no matter how much inconvenience it caused to potential investors at the time. In the words of Vice President Wang Qishan, there needs to be “a fine balance between encouraging financial innovation, invigorating the market, opening up the financial sector and building regulatory capacity.” Given the importance of commercial banks to China’s financial and economic system, a degree of caution on the part of the regulators at this point may be in investors’ best interests.

Focus on Business Relations Not Government Relations in 2021

Chinese equities joined the global equity rally following the election of Joe Biden as the next U.S. president. This was despite the view widely held outside China that there would be no major reengagement between the two governments and that Biden would be forced by domestic politics to continue to take a tough line on China. In areas like national security, intellectual property copyright, industrial subsidies, and technology transfer, U.S. policies toward China may change little compared with those of the Trump administration. The consensus within China is that although the U.S. and China are expected to remain strategic competitors, more communication and dialogue between them can better manage the risks, while allowing economic relationships to normalize. The phase one trade deal reached in February is expected to survive in modified form. Over time, it may progress to phase two issues such as intellectual property copyright and technology transfer. There is likely to be less importance attached to the U.S.-China bilateral merchandise trade balance. A cooling off in government rhetoric may encourage business leaders in China and the U.S. to quietly resume normal operations. Left to businessmen alone, economic decoupling between the U.S. and China is unlikely to occur on a significant scale.

Looking Ahead: China Equity Markets in 2021

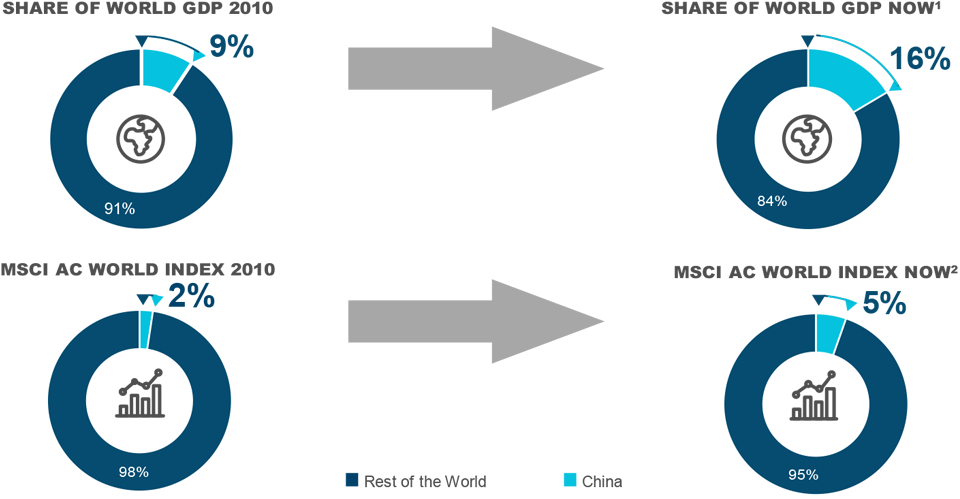

China’s strong economic recovery from the coronavirus has not gone unnoticed. It is the first major economy where both supply and demand are close to normalizing. A growing number of global equity strategists and asset allocators have made overweight China their top call for 2021. As foreign investors only own a small percentage of the market, they do not drive share prices directly—these are determined domestically. But growing foreign interest in Chinese equities helps to boost domestic investor sentiment. So far, foreign inflows have been moderate, held back by reduced global risk appetite. Equity mutual funds—Asian and global—are broadly neutral China versus popular benchmarks, with scope to increase positions. More important, over the longer term, we believe the global benchmark indices themselves do not reflect China’s current economic strength (Fig. 5). They are structurally underweight China, a divergence that we believe is likely to narrow over time.

China Market is Underrepresented in Global Equity Index

(Fig. 5) MSCI AC World Index weight versus world GDP share

As of September 30, 2020.

1 Latest data as of December 31, 2019.

2 As of September 30, 2020.

Sources: World Bank/Haver Analytics and MSCI (see Additional Disclosures).

Despite the large positive growth divergence in China’s favor, the external balance has remained in surplus, supporting the renminbi, i.e., China has been able to increase its global export share during the pandemic. In a quantitative easing (QE) world of zero yields, China’s bond markets continue to attract strong inflows from fixed income investors. With incomes growing faster than spending in 2020, households have increased savings, some of which may flow into equities. The positive fundamental outlook for Chinese equities in 2021 is even more attractive in relative terms given the still uncertain outlook for many other economies, both developed and emerging.

Pulling the above together, we are positive on the outlook for the fundamentals for Chinese equities in 2021 for three key reasons: (i) economic recovery is expected to continue, with consumption the main driver; (ii) vaccine approval and distribution should allow China to reopen its borders to the rest of the world at some point next year; and (iii) global investors are structurally underweight Chinese equities.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.