August 2022 / INVESTMENT INSIGHTS

China Property: The Endgame

Policymakers could aim to stabilize rather than reflate the sector.

Key Insights

- The property sector could become less important to China’s economy and its growth is likely to slow.

- Better funded state-owned developers and strong private real estate firms are likely to survive.

- Mortgage boycott impact on the financial system is manageable and we believe restoring households’ confidence in housing is key to averting further escalation.

China's real estate landscape is undergoing profound structural shifts driven mainly by significant policy changes. During this time, President Xi Jinping has repeatedly reinforced his key policy message that “houses are for living in, not for speculation”, forcing property developers to adopt a more utilitarian model. The structural changes taking place are resulting in increasing market share for state-owned developers at the expense of private sector companies. We expect the latter to play a smaller role in China's residential property sector in the years ahead. As these trends play out, over time we expect to see healthier balance sheets emerge for those developers able to survive the current downturn, with more stable operations coupled with more modest profit margins.

The days of rapid, break-neck growth for the Chinese property sector are behind us. Although urbanization may continue to be a driver, as will upgrading, the consensus is that the overall pace of growth will slow. In relative terms, the property sector is expected to become less important to the Chinese economy over time. Moderation on the price appreciation front is also likely, confirming Beijing’s determination to eradicate property speculation and provide more affordable housing to a broader section of China's population. Affordability is increasingly a concern for the government - incomes for many households have declined in the wake of the pandemic and slowing economic growth has led to a rise in urban unemployment. It is estimated that only around 20% of fresh university graduates this year have been able to get jobs.

While these objectives may provide a ceiling to prices, the authorities clearly wish to avoid significant falls in home values since property accounts for a large proportion of household wealth. Sharp drops could have a significant negative wealth effect on consumer demand that could potentially threaten social stability. Managing property deleveraging without triggering a sharp fall in home prices and a macro- economic downturn is a very difficult balancing act. However, the Chinese government realizes there is no other choice, as putting off these painful yet necessary structural reforms can only make matters worse in the long run.

Short Term Headwinds

Short-term headwinds continue to impede the recovery of the residential property sector in 2022, led by a sharp fall in home sales and construction activity, tight liquidity conditions, mortgage repayment boycotts and the threat from renewed outbreaks of COVID-19. Reports about mortgage repayment suspensions by homebuyers emerged in July as a protest against the non-delivery of purchased apartments by cash- strapped developers. According to one study by Citi, in 24 cities, properties with delayed delivery as of end 2021 accounted for 9% of 2021 new home sales in these cities. If the mortgage strike continues, the same study estimated that in a worst-case scenario it could create CNY561 billion of new non-performing loans, or 1.4% of the total outstanding mortgage balance, creating a drag on GDP of around 0.3%.

Since there are significant costs borne by homebuyers who default on their mortgages, we believe their purpose is to pressure central and local governments and property developers to ensure the unfinished units are delivered. While the recent mortgage boycott is indicative of the severity of the downturn, we believe that the impact on the financial system is manageable. We think restoring households’ confidence in housing is the key to averting further escalation. But this will take time and a prerequisite to this is the completion of stalled projects for which homeowners have already paid.

Size Matters

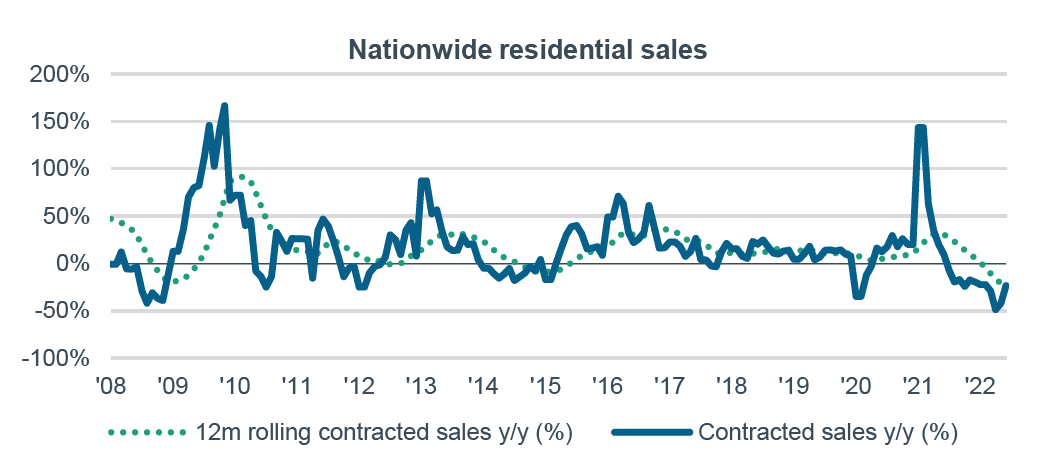

For China's listed property developers, liquidity and continued access to capital markets have become crucial since contracted sales, the biggest source of operational cash flows, have continued to shrink rapidly. Residential property gross floor area (GFA) sold in 1H 2022 slumped 26.6% year on year. The outlook for the second half of 2022 is less pessimistic as the base effect will wear off, while there are some early signs that the market is beginning to stabilize. Recovery in 2023, however, is expected to be weak and a sharp rebound in China’s residential property sector appears unlikely. Dropping the 5.5% economic growth target for 2022 is also a signal from policymakers that they aim to stabilize rather than reflate the housing market.

Weak Residential Property Numbers

(Fig. 1) Contracted sales have declined year on year

Source: NBS, Beike, BofA. data analysis by T. Rowe Price.

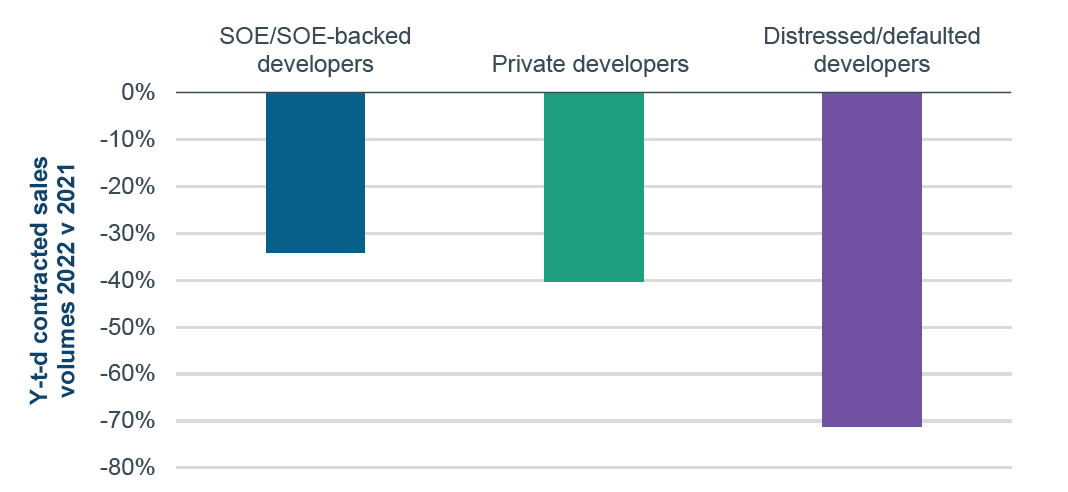

State-owned property companies with deeper pockets and better funding access are starting to dominate the sector, with only the better managed companies in the private sector expected to survive. It is estimated that only the top quarter of the privately owned developers will pull through, with the rest falling by the wayside as funding conditions become increasingly restrictive triggering a broad sector consolidation. The divergence in performance of strong versus weak developers is expected to continue to widen.

Divergence in Operating Performance among Developers

(Fig. 2) State-owned developers with deeper pockets and better funding access outperform

Sources: Bloomberg, CRIC, Company data, data analysis by T. Rowe Price. Numbers may not total due to rounding.

Much of the pain enroute to the long- term objectives of affordable housing and deleveraged balance sheets has been borne by the offshore bond market. As the pressure has started to broaden out, economic challenges have grown and spread to other areas, triggering a more decisive policy response from the government. For example, mortgage approvals have accelerated since late last year, local level restrictions have been eased, and recent reports say Beijing will launch a real estate fund potentially totaling CNY300 billion (USD44 billion) to help property developers complete unfinished units and to restore confidence among homebuyers. Reports that Chinese regulators plan to allow select developers to issue yuan-denominated bonds guaranteed and underwritten by state owned firms was welcomed by the markets. Names mentioned include Longfor, Gemdale, Country Garden, CIFI, Seazen, and Sino Ocean. This is a stronger policy support than in the previous round where high-quality POE developers issued CNY500 million to 1 billion of bonds with partial credit protection. However, we still need to monitor the actual issuance size. This is positive for the short-term financial liquidity of the selected developers, but a recovery of the physical market is more important for the sector.

China's regulators are mindful of adding to potential systemic risks by bailing out the weaker developers. At the same time, Chinese banks naturally remain wary of incurring higher non-performing loans by raising their exposure particularly to weaker players in the sector. Furthermore, local governments know they will be held accountable by Beijing for the completion of unfinished units locally, so they remain reluctant to loosen escrow account regulations that restrict the access of property developers to presale revenues. It therefore seems likely that only state-owned property developers and privately owned enterprises with strong balance sheets can survive as they continue to receive more favorable treatment from the regulators, lenders and investors.

Investment Implications

In the near term, we expect the Chinese property sector to remain volatile. Further out, we anticipate consolidation in the sector followed by a return to more stable conditions. The investment implications are that credit selection will be of particular significance in this bifurcated sector and deep fundamental research will be key to identifying the long- term survivors. The challenging environment suggests investors in China credit should favor a highly selective bottom-up investment style. A strong credit research team will be crucial for selecting property developers with adequate liquidity buffers, greater exposure to top tier cities that are still expanding, and low short-term refinancing needs.

The decline in issuance from the China property sector accompanied by sharp fall in prices has reduced its importance to the Asia USD credit asset class. Given the uncertain short- term outlook in China, there has also been a sharp reduction in the overall debt issuance from Chinese issuers at a time when the regional primary market has reported robust volume growth. We continue to see growth in the Asian credit markets, driven by more opportunities emerging in a regionally diversified way.

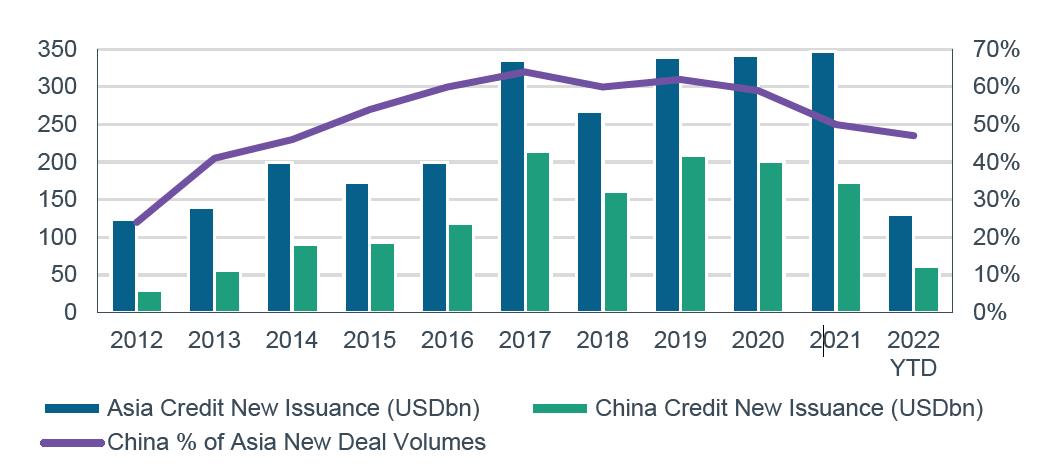

Non-China Issuance Building Momentum

(Fig. 3) Asian primary markets are more diversified as issuers outside China became more active

Sources: JP Morgan, Bloomberg, data analysis by T. Rowe Price.

We still consider Asian credit to be the higher quality segment of the emerging markets fixed income universe. The sector is comprised of diversified and high-quality markets with an average rating of BBB+ while 30% of the issuers belong to the developed market category. Asia has higher domestic savings and better current account surpluses relative to the rest of the emerging markets. Even if China’s short-term credit outlook remains clouded, we believe there are attractive investment opportunities within the region as the fallout from the Chinese property sector remains largely contained.

Important Information:

Where securities are mentioned, the specific securities identified and described are for informational purposes only and do not represent recommendations.

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

This material is only for investment professionals that are eligible to access the T. Rowe Price Asia Regional Institutional Website. Not for further distribution.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

August 2022 / INVESTMENT INSIGHTS