February 2022 / GLOBAL FIXED INCOME

Why Fixed Income Investors Should Think Differently in 2022

Higher rates and more volatility demand a flexible approach.

Key Insights

- Changing dynamics mean that the past decade is probably a poor guide as to how bond markets might perform in 2022.

- With governments and central banks simultaneously removing stimulus support, we expect a year marked by tighter global liquidity, higher interest rates, and bouts of volatility.

- While the environment is likely to be challenging, we also see potential for great buying opportunities to emerge, so a flexible approach to bond investing will be important.

Strap yourself in: 2022 could be a roller‑coaster ride for bond investors. After more than a decade of stimulus measures, major central banks are likely to step back from supporting markets. How this evolves will matter much more than forecasts of economic data, given that aggressive central bank actions helped to drive bond yields so low in the first place. The retreat of central banks, which are typically price‑insensitive buyers, could have major implications—including tighter liquidity conditions, bouts of volatility, and higher interest rates.

The withdrawal of central bank liquidity, along with rate hikes in some countries, will come at the same time that governments wind back levels of pandemic fiscal support. The confluence of these factors is likely to drive most developed government bond yields higher. In response, bond investors may need to adopt a broader, more flexible approach that emphasizes active duration management.

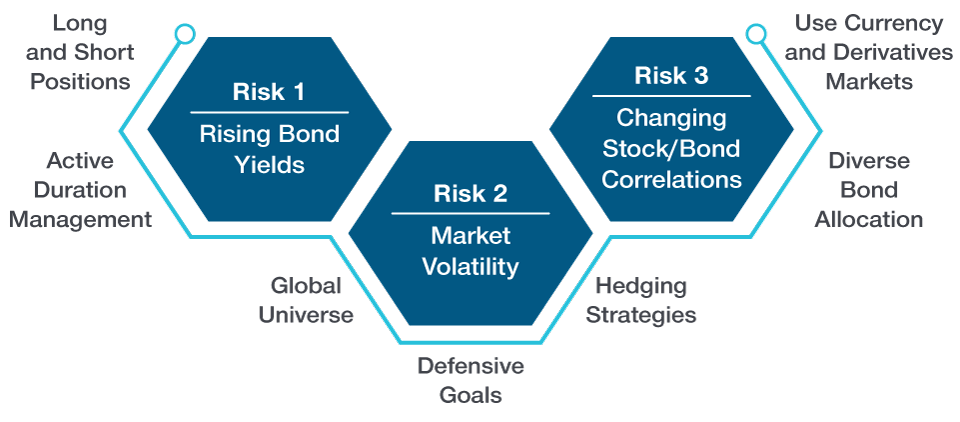

Managing Market Challenges in 2022

Three key risks and mitigation approaches

As of December 31, 2021.

Source: T. Rowe Price.

1. Key Risk—Get Ready for a Period of Tightening

Just as inflation reached unimaginable levels last year, so too may bond yields in 2022. An early hint of what might happen occurred during the autumn of 2021, when Poland’s central bank responded to inflationary pressures with three successive rate hikes in as many months. The yield on the country’s two‑year local currency bond rose by more than 250 basis points in just three months to end December around 3.36%.

The path to higher rates is likely to be volatile as there is uncertainty over the pace of tightening and exactly how many central banks will join in. For example, the European Central Bank appears reluctant to move this year, but if inflation forces its hand it could prove decisive for bond markets. Balance sheet reduction is also a possibility—the U.S. Federal Reserve, for example, has already revealed that it has held discussions about how it intends to manage this process. However, if multiple global central banks decide to shrink their balance sheets at the same time, it may have far‑reaching consequences as this type of scenario is untested in bond markets.

It’s important to remember that while the environment could be challenging ahead, at some point there’s likely to be an inflection point where valuations turn attractive and potential great buying opportunities emerge in rates markets.

Portfolio Approach—Active Duration Management Will Be Critical

We believe that managing duration actively will be critical to navigating this environment. This approach enables investors to tactically respond to different market environments and regime changes. It also gives investors flexibility and latitude to take potential advantage of any pricing anomalies and dislocations that might occur in a volatile environment.

A broad approach that brings the potential to invest in different bond markets across the globe may also be beneficial. It offers opportunities to take advantage of scenarios where policy is diverging. For example, in the current environment, we are finding potentially attractive opportunities in select emerging markets where central banks are further progressed in their hiking cycles. China’s local bonds are also appealing as the Bank of China is expected to continue easing to support growth, in stark contrast to most developed markets.

2. Key Risk—Credit Markets Are Not Immune From Volatility

With defaults expected to remain at very low levels, the fundamental environment for credit is likely to remain strong this year. However, despite this highly supportive backdrop, it’s unlikely to be enough to save credit markets from volatility—they remain vulnerable to possible spread widening through systematic risk. A key market risk factor, in our view, is the prospect of liquidity support waning as central banks wind down their quantitative easing programs. The latter is likely to lead to a tightening in financial conditions, a development that may cause bouts of turbulence in risk‑sensitive markets such as credit.

Furthermore, as valuations are tight, there is less of a cushion to absorb interest rate volatility. This matters because credit contains a duration component that exposes it to changes in the underlying risk‑free rate—a risk that is not always fully understood by investors. Over the past decade, the duration of corporate bonds has been extended, so investors may have become much more exposed to interest rate risks now than they have been in the past. Also keep in mind that duration has been a key driver of credit returns in recent years, which is not a problem when yields are trending lower. The climate is changing, though, and we may be entering a rising rate environment with the potential for duration losses for credit investors.

Similar to rates markets, however, at some point a potential great buying opportunity could emerge in the credit space. An example here is March 2020, when a huge sell‑off in credit opened up a good opportunity to add select exposures at cheap prices.

Portfolio Approach—Defensive Positioning and Active Duration Management

A defensive approach may work well in this environment as hedging strategies are often deployed to help navigate volatility. Managing duration actively is also critical given the duration risks to which credit portfolios may be exposed.

3. Key Risk—Stock/Bond Correlations Are Changing

Investors often assume that fixed income is a diversifying asset class that typically performs well when risk markets such as equities sell off. This has meant that government bonds have often been used as the primary source of risk mitigation to keep portfolios balanced. However, at current rates, we believe government bonds are expected to be much less effective as a diversifier than they have previously been.

Furthermore, investors should keep in mind that the stock/bond relationship is not always a constant. For much of the 1990s, for example, the correlation between the two was positive—we believe a return to this dynamic should not be ruled out in 2022. Markets are set to undergo significant change as monetary support is withdrawn, so it is plausible that both rates and stocks may sell off simultaneously at times this year.

Portfolio Approach—Go Broad Using Full Toolkit of Instruments

A broad approach that deploys the full toolkit, including currency and derivatives markets, may help to balance and mitigate risks in a portfolio.

How the Dynamic Global Bond Strategy May Help In This Environment

The changing market environment means that investors can no longer rely on the post‑Global Financial Crisis investment playbook and will need to think differently in 2022. We believe that our Dynamic Global Bond Strategy, which is index agnostic and deploys active duration management, is suited to precisely this environment. Specifically, we believe the strategy offers the following benefits:

Flexible: We manage duration actively within a wide latitude and have the ability to implement both long and short positions. This gives us the flexibility to adapt to different market cycles and environments, including rising rates. For example, when interest rates are rising, we should have the ability to quickly cut the portfolio’s overall duration to as low as minus one year to minimize potential losses, using instruments such as fixed income futures and interest rate swaps. By contrast, when rates are falling, we can increase overall duration to as high as six years to maximize gains. We believe this dynamic and tactical approach to managing duration will be critical in 2022 as central banks retreat, potentially causing bond yields to rise.

Broad: We benefit from a large global research platform that powers our investment ideas. Covering more than 80 countries, 40 currencies, and 15 sectors, our deep research capabilities enable us to uncover inefficiencies and exploit opportunities across the full fixed income investable base. Our broad approach is likely to be beneficial in 2022 as it should enable us to take advantage of scenarios where policy is diverging. Furthermore, with the potential for the stock/bond relationship to change, our ability to express views across a wide range of different currencies, bonds, and sectors should help with diversification efforts.

Volatility Management: Our strategy goals are to generate regular returns, manage downside risks for our clients, and provide them with genuine diversification away from equity markets. To help achieve the latter, we implement defensive hedging positions at all times, which may include short positions on emerging market currencies, allocations to markets displaying defensive characteristics, and/or long volatility positions via options. This gives us the potential to benefit from falls in the prices of risk assets during periods of market turbulence. As we expect volatility in 2022, our defensive approach could prove fruitful.

This year is shaping up to feature the potential risks of market volatility, higher interest rates, and tighter liquidity. Although the environment is likely to be challenging, we expect great buying opportunities to emerge at some stage in both rates and credit markets. So it’s not just a case of navigating the expected rise in volatility, but also identifying when there’s a potential inflection point. Overall, we believe this environment is conducive for our approach, which is flexible; emphasizes active duration management; and the implementation of defensive hedges to help provide diversification against risk assets.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Arif Husain is the head of Global Fixed Income and chief investment officer of the Fixed Income Division. He is chairman of the Fixed Income Steering Committee and a member of the firm’s Management Committee. Arif is lead portfolio manager for the Global Government Bond High Quality Strategy. He is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.