April 2021 / MULTI-ASSET SOLUTIONS

Three Reasons Why Pent-Up Demand Is Not a Growth Panacea

The recovery in European asset prices is likely to be nonlinear

Key Insights

- Although a backlog of demand has built up during the lockdown, this is unlikely to result in a sustained rebound in growth.

- The recovery is likely to be a complex affair, resulting in a wide dispersion of returns across asset classes.

- We believe active management is better placed to benefit from the nonlinear repricing that will likely occur once we enter a more stable post-coronavirus environment.

Investors hoping that pent‑up demand will fuel a sustained post‑coronavirus economic recovery in Europe may end up disappointed. Although a backlog of demand has built up during the lockdown, its potency is likely to be reduced by the withdrawal of government stimulus, growing wealth disparities, and shifting consumption patterns. Accordingly, the European post‑coronavirus recovery will likely be a complex affair—one that is likely to result in a wide dispersion of returns across assets.

Three Challenges to the Recovery

Why pent-up demand may not be enough

It is easy to understand why many investors are hoping for a cyclical recovery. Although the economic fallout from the coronavirus caused unemployment to rise across Europe, fiscal stimulus packages kept businesses afloat, workers in jobs, and financial gaps plugged through loans, grants, furlough schemes, and unemployment benefit funding.

In fact, the pandemic‑induced recession led to the largest rise in household savings since World War II. This was largely because household spending dropped sharply as lockdowns prevented people from consuming in line with their habitual expenditure basket and size. As household consumption comprises around two‑thirds of gross domestic product in advanced economies, even a partial release of these savings once lockdown restrictions are eased should, theoretically, result in an immediate and persistent rebound in growth.

This time is likely to be different, however. Here, we provide three reasons why.

Risk of Premature Policy Withdrawal

Last year’s equity rally was partly due to generous government coronavirus support programs, but it also owed something to the expectation that consumers, once permitted, will quickly revert to pre‑pandemic spending patterns or—even better—compensate for consumption they missed out on because of lockdowns. This is a fair assumption for many services. Private medical and dental practices, for example, will likely face a large increase in demand when previously delayed treatments can finally take place. In other areas, however, pent‑up demand will have far less of an impact. Somebody who has been denied a haircut during lockdown, for example, is not going to get two haircuts in a row to compensate for that.

These two examples show how differently pent‑up demand will manifest itself in different areas. It is likely that the biggest economic sectors, food and accommodations (including travel), fall somewhere between the two, depending on consumer behavior. The “social consumption” nature of these sectors means that a large rise in demand would also be reflective of the deprived social interaction during lockdown. In Australia, restaurant bookings doubled compared with pre‑pandemic levels after lockdowns ended during the summer in the Southern Hemisphere. This suggests that consumers replaced consumption they had missed out on during the lockdown with overconsumption once the lockdown was lifted. There is another way of interpreting this, though: If consumers anticipate another lockdown in the event of a new wave of the virus, they may increase their consumption to take advantage of the freedom to eat out or go on vacation while they can.

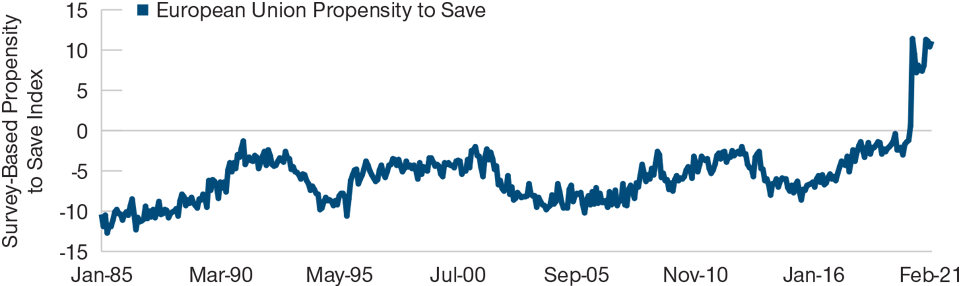

COVID‑19 Turned Europeans Into Savers

(Fig. 1) Consumers’ propensity to save hit record levels

As of February 28, 2021.

Propensity indicator computed as the difference between the answers to the survey question about households’ expected savings and the answers to the question about their expected financial situation (Question 11 minus Question 2). Data exclude the United Kingdom from January 2021 onward.

Sources: T. Rowe Price analysis and European Commission Consumer Survey, February 2021.

In either case, the result would be an initially strong recovery. However, if it turns out that people have merely brought their winter consumption forward to the summer, then the rapid pace of the services recovery is unlikely to last. The risk here is that authorities see an initial strong summer recovery, assume it will be maintained, and then reduce monetary and fiscal policy support, including a withdrawal of furlough schemes. Some degree of creative destruction would be inevitable during a withdrawal of support, meaning that some businesses will fail and furloughed workers will move into unemployment. Yet, any premature withdrawal of policy support may make this adjustment more economically painful and the recovery significantly longer.

Bond investors may be able to take advantage of this potential policy flip flop. As lockdowns are lifted, we expect an initial bond sell‑off, fueled by a strong consumer‑led recovery. In the medium term, however, we see risks for policy errors as the persistence of the strong consumer demand recovery is misjudged. This is likely to result in a drag on growth, leading to lower bond yields. Investors can try to protect their portfolios against a potential policy mistake by steadily adding to their defensive fixed income allocations as yields should initially rise when coronavirus restrictions are gradually lifted.

Exacerbated Wealth Disparities

As discussed previously, household savings expanded firmly through the crisis at the aggregate level. However, this accumulation of wealth has not been enjoyed equally across all households. Survey data by the European Central Bank and the Bank of England suggest that high‑income households saw their savings rise far more than those of their lower‑income peers. Throughout the crisis, lower‑income households were more likely to become unemployed or furloughed, were less likely to perform a job that could be done remotely, and were less likely to hold substantial financial assets that benefited from the market rally that followed the sell‑off.

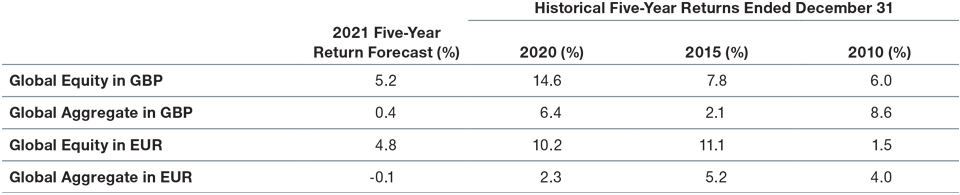

Weak Demand Should Suppress Bond Yields

(Fig. 2) Fixed income has a role as a defensive asset

As of January 31, 2021.

MSCI ACWI for Global Equity, Bloomberg Barclays Global Aggregate Index for Global Fixed Income.

This information is not intended to be investment advice or a recommendation to take any particular investment action. The forecasts contained herein are for illustrative purposes only and are not indicative of future results. This material does not reflect the actual returns of any portfolio/strategy. Forecasts are based on subjective estimates about market environments that may never occur. Returns and volatility of a portfolio may differ from those of the index. Management fees, transaction costs, taxes, and potential expenses are not considered and would reduce returns. Expected returns for the asset classes shown can be conditional on economic scenarios; in the event a particular scenario comes to pass, actual returns could be significantly higher or lower than forecast. Historical returns shown represent past performance. Past performance is not indicative of future performance.

Source: T. Rowe Price.

The relative increase in savings among high‑income households during the pandemic exacerbated preexisting wealth inequalities. Given that working‑age households are more comfortable spending out of their recurring income than their accumulated wealth, high‑income households are less likely to spend their savings. This way the elevated wealth dispersion threatens to drag on the recovery.

Finally, real estate and financial assets became effectively more expensive during 2020 as this is where most savings likely went. Compared with pre‑coronavirus times, households that are saving for retirement today will consequently need to assume lower rates of return on their investments and raise pension savings to expect the same standard of living, all else being equal. This applies particularly to lower‑income households, which are earlier in their life cycle and have the highest marginal propensity to consume. Higher‑income households, which are later in their life cycle and have a low propensity to consume, will likely continue to benefit from an uplift in asset prices.

Overall, these developments mean that aggregate consumption growth could be weaker than expected in the medium term. We therefore expect the long‑run trend consumption growth rate to establish itself below pre‑pandemic levels. This would translate into a lower natural rate of interest, R*, and lower bond yields. Coupled with our earlier remarks on the possibility of a policy misstep, the likelihood of this outlook presents another headwind for fixed income yields in the medium to long term.

Thus, we believe investors should continue to hold defensive fixed income building blocks within their portfolios. Although overweighting risk assets may prove to be advantageous as consumption snaps back, investors should also include some conservative assets that may provide some risk mitigation in case of a transition toward a lower consumption growth environment.

Shifting Consumption Patterns

Secular shifts in consumer preferences are likely to bring a source of additional creative destruction in several sectors of the economy. Early signs of trend reversals can already be observed in the real estate market, where rents of centrally located apartments in large metropolitan areas have been more adversely affected by the crisis than their rural counterparts. Work‑from‑home technology enablement has allowed renters to reevaluate their preferential housing conditions, and the expectation is that consumers will continue to place increased importance on their living environment. Businesses that rely on customer foot travel will have to fight hard to compete with newly acquired consumer habits.

Similarly, online and mobile distribution channels have further entrenched themselves into consumption patterns. Sectors such as retail and entertainment saw a pickup in adoption from already elevated levels. More interestingly, however, remote distribution established strong footholds in previously underrepresented sectors such as education and medicine. Technology companies that profit from or enable these trends have been the major beneficiaries of this new reality. Once these changes in consumer behavior have manifested themselves, it is hard to imagine a reversal to pre‑coronavirus patterns.

Investors should also pay close attention to producers’ capacity to cope with lasting changes in consumer preferences. The coronavirus‑induced demand spike for electronics, for example, resulted in a supply shortage of semiconductors at the beginning of 2021, resulting in wide‑ranging production issues affecting many sectors, from automotive to home entertainment.

Therefore, investors need to be nimble in identifying where consumer demand will recover strongly, where it meets supply chains that can accommodate persistently elevated demand levels, and whether consumption will revert back to pre‑crisis patterns or follow new rules. We believe that a broad rotation into small‑cap, value, and emerging market stocks would miss the dispersions that linger beneath the headline “pent‑up demand” story.

Lockdowns have forced consumers to adopt new technologies and habits that have permanently changed consumption patterns. As such, we favor an active management approach within these market segments. Active management is better placed, we believe, to benefit from the nonlinear repricing that will likely occur once we enter a more stable post‑coronavirus environment.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

April 2021 / INVESTMENT INSIGHTS

April 2021 / INVESTMENT INSIGHTS