June 2022 / INVESTMENT INSIGHTS

The Case for China Remains Strong

A more complex environment does not necessarily mean a less rewarding one

Key Insights

- Investing in China has become more complex in recent years as Beijing has introduced tighter legislation focused on key sectors including internet and property.

- Despite China’s apparent lurch toward authoritarianism, the authorities will not allow their “common prosperity” program to derail the economy.

- Compelling opportunities exist in areas such as electric vehicles, renewable energy, and mature sectors undergoing consolidation.

Caution over investing in China is higher than it has been in decades—and not without reason. An uncertain regulatory environment, concerns over the country’s strict COVID‑19 regulations, and growing geopolitical tensions have left many foreign investors feeling jittery about putting their money into the country. But has China really become “uninvestable,” as some have claimed?

In a recent call, I asked several T. Rowe Price investment professionals for their views on the current state of China—from the likely direction the country will take under President Xi Jinping to the impact of the “zero‑COVID” policy and the threat of external headwinds. Their responses confirm that Beijing’s frequent, often unpredictable, policy swerves have made investing in China more complicated in recent years—but they also suggest that compelling opportunities remain for those willing to look for them.

COVID‑19 Continues to Drag on the Chinese Economy

To begin, we focused on the challenges the Chinese economy faces. Chris Kushlis, chief of China and emerging markets macro strategy, pinpointed China’s ongoing difficulties in tackling COVID‑19 as a key determinant of the country’s near‑term economic prospects. “China simply hasn’t gotten on top of the omicron variant in the way that it hoped,” he said. “The restrictions needed to keep the virus under control will weigh on both local and global markets via supply chain disruptions and reduced demand for commodities. If there are continued outbreaks, it will be a persistent drag on the Chinese economy.”

Despite rumors that China might abandon its zero‑COVID policy as early as this summer, Kushlis believes that is unlikely. “Our base case is that the zero‑COVID policy remains for the time being,” he said. “It would probably be too politically risky to drop it before the Communist Party’s National Congress in November. However, we may see it phased out after that.”

Policymakers remain committed to China’s 5.5% growth target for 2022, but Kushlis is skeptical that this will be achieved. In addition to the threat from further COVID‑19 outbreaks, he cited the ongoing challenges the housing sector faces and a negative outlook for exports as headwinds for growth. “China’s exports boomed during the initial COVID‑19 outbreak, but they have now become a hostage to foreign goods demand,” Kushlis said. “If that demand falls, exports—which have been an engine of growth for China—will become a headwind.”

These headwinds will likely be offset to some degree by other factors, however. “China is in a different place from most other large economies in that it has very little underlying inflationary pressure,” said Kushlis. “This gives the People’s Bank of China a bit more latitude than it would have if it were locked into a hiking cycle.

“Other positives for China include its strong balance of payments and the fact that limitations on travel have made it very difficult to take money out of the country, enabling state banks to accumulate reserves,” he added.

Putting “Common Prosperity” Into Context

China’s economic uncertainty also owes a great deal to policy uncertainty. Under the “common prosperity” policy drive that it launched last year, Beijing introduced new regulations covering sectors ranging from real estate and education to technology and entertainment. In the process, it wiped more than USD 1 trillion off the value of some of the country’s largest companies, including Alibaba Group, Tencent Holdings, and New Oriental Education.1 This bout of regulatory zeal—and a fear that it may not yet be over—is another key reason why investors are cautious about investing in China today.

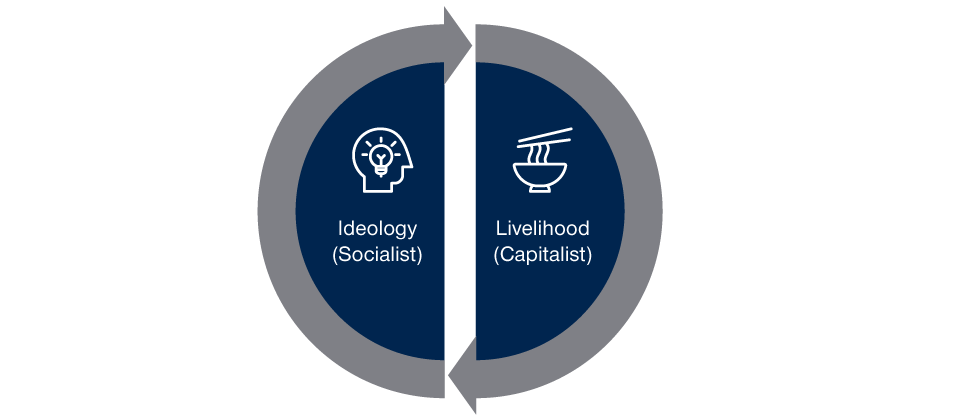

China’s Constant Balancing Act

(Fig. 1) Investing becomes more complex if the equilibrium is broken

Source: T. Rowe Price.

Ernest Yeung, portfolio manager for the Emerging Markets Discovery Equity Strategy, said that China’s recent apparent lurch toward authoritarianism should be understood in the context of Chinese Communist Party’s (CCP) constant need to balance a socialist ideology with a pragmatic approach to wealth creation (Figure 1). “Before President Xi, China was very focused on job creation and was effectively pursuing capitalist policies,” Yeung said. “Since Xi arrived, he’s been trying to pivot the country back toward socialism to correct some of the imbalances that have arisen because of those policies. That’s what ‘common prosperity’ is about.”

“The highest risks are when businesses are not aligned with policy objectives and are earning supranormal profits,” said Anh Lu, lead portfolio manager for the Asia ex‑Japan Equity Strategy. “When businesses are well aligned to policy objectives, they will probably be allowed to earn very high profits for a period. But when businesses are not well aligned with policy objectives, their ability to earn higher‑than‑normal profits may be less tolerated.”

However, Yeung argued that it is important to remember that the CCP’s main objective is to stay in power—and that to achieve that, it must keep people happy. “If Beijing focuses too much on ideology at the expense of wealth creation, people will start to lose their jobs, inflation may become out of control, and social problems will arise,” Yeung said. “Before that happens, the authorities are likely to leave ideology aside and pivot back toward more pragmatic policies.”

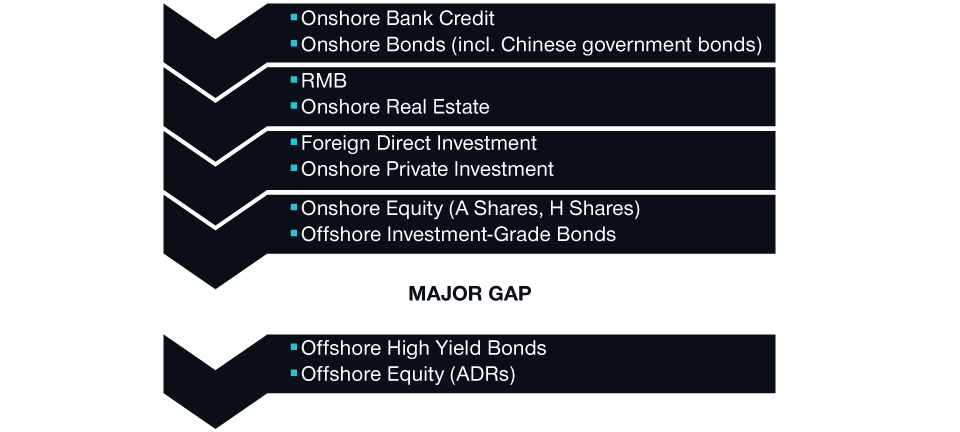

Understanding China’s “Hierarchy of Capital Flow”

When it comes to gauging the impact of Beijing’s policy actions on Chinese assets, Samy Muaddi, portfolio manager of the Emerging Markets Bond Strategy, suggested it may be useful to consider China’s “hierarchy of capital flow” (i.e., the order in which the authorities prioritize their obligations to capital markets (Figure 2). “The biggest constraint China faces is the stability of its onshore banking system—and that’s because it’s one of the few countries that still runs a monetary aggregate framework,” Muaddi said.

Below the onshore banking system, in order of importance, are onshore bonds, the renminbi (RMB), onshore real estate, foreign direct investment, onshore private investment, onshore equity, and offshore investment‑grade bonds. “Then there is a big gap to the bottom rung of the hierarchy, where offshore high yield bonds and offshore equity sit,” Muaddi said. “When China’s policy objectives intersect with an investment low in its hierarchy of capital, there is a much higher probability of tail risk outcomes. The bottom of the hierarchy can go through an existential crisis while the top of the hierarchy is just going through a normal cycle.”

How Policy Impacts Investments

(Fig. 2) Beijing’s hierarchy of capital flow

Source: T. Rowe Price.

Internet and property firms have been hit particularly hard by regulation. Of the former, Jacqueline Liu, a regional portfolio manager in the Equity Division of T. Rowe Price International, said: “The internet sector has been in the grip of major regulatory change since the Ant [initial public offering] was cancelled in October 2020,” she said. “These days, the sector makes up around 30% of the MSCI China Index, which is well down from its peak of around 50%.”

Liu said that the growth outlook for the internet sector is fundamentally less attractive than it was five years ago and predicted that it will become more cyclical over time. “When investing in the internet in the future, it will probably make sense to focus on two sectors,” she said. “First, areas where penetration is still low, such as food delivery, online recruitment, and cloud computing, and second, areas with overseas expansion opportunities, such as international game development and the monetization of TikTok.2”

Muaddi offered a frank description of how regulation has affected the property sector. “In recent years, picking the best property bond in China has been like paying for the parlor suite on the Titanic—it doesn’t matter what you’ve bought when the whole ship has sunk,” he said.

However, Jai Kapadia, manager in T. Rowe Price’s International Equity Division, pointed out that Beijing has already begun to ease policy. Measures introduced have included the lowering of mortgage rates on first and second homes, the relaxation of purchase and sale restrictions, and the lowering of minimum deposits. “Looking ahead, I think it’s clear that state‑owned enterprises [SOEs] will continue to gain market share—they bought around 60% of the land sold last year,” Kapadia said. “It’s also apparent that commercial property will compose an increasing percentage of profits as developers prioritize recurring income over the more volatile residential market.”

Kapadia said that he expects the biggest opportunities for investors will be in the largest SOEs, property management companies, and commercial property real estate investment trusts.

Identifying the Leading Local Firms of Tomorrow

When considering the potential opportunities of the future, it is worth remembering how rapidly the Chinese investment landscape can change. The MSCI China Index, the most closely watched Chinese index, has altered dramatically over the past 20 years (Figure 3). “Two decades ago, telecoms were dominant, composing around 60% of the index,” said Wenli Zheng, portfolio manager of the China Evolution Equity Strategy. “Ten years ago, financials was the biggest sector. Now, it is technology, and in particular internet platforms that were the major winners over the past decade.”

China’s Evolving Investment Landscape

(Fig. 3) The composition of the MSCI China Index, 2011 versus 2021

Analysis as of April 30, 2022. Chart shows index composition as of year‑end 2011 and 2021.

Technology = information technology, media and entertainment, and internet and direct marketing retail. Financials = financials and real estate. Telecom = communication services ex media and entertainment. Other = industrials, utilities, and materials.

T. Rowe Price uses the MSCI/S&P Global Industry Classification Standard (GICS) for sector and industry reporting. T. Rowe Price will adhere to all future updates to GICS for prospective reporting. See Additional Disclosure page for information about this MSCI and GICS information.

Sources: Bloomberg Finance L.P. and FactSet. Financial data and analytics provider FactSet. Copyright 2022 FactSet. All Rights Reserved.

For the next five to 10 years, electric vehicles could be the next major area of opportunity, Zheng believes. “China is one‑third of the global auto industry, but domestic manufacturers have lagged—foreign brands have 70% market share of domestic Chinese ICE [internal combustion engine] car sales,” he said. “However, this is changing with the rise of electric vehicles, where local firms have around 65% of the market. China has arguably one of the most comprehensive supply chains in the world for electric vehicles, so it has the potential to be a major exporter in this area. This will have broad implications not just for auto sales, but it has potential for industrial upgrades across the manufacturing space.”

Zheng also highlighted renewable energy as an area of potential growth. “China is a major importer of fossil fuels but is a major exporter of renewable energy—it is dominant in solar, and has a high market share in wind turbines,” he said. “The energy transition creates opportunities along the whole value chain, from generation to transmission to storage. It can turn one of China’s vulnerabilities into relative strength”.

In traditional industries, the opportunity for leading players is scope for consolidation,” Zheng said. He cited the home improvement sector, where the leading Chinese firm by market capitalization, Oppein Home,3 has just a 1.2% market share—a tiny portion compared with the 17% share of the U.S. market enjoyed by Home Depot. “We believe industry consolidation will be a major driver for future compounders in China,” said Zheng. He also highlighted the Chinese hotel industry, where China Lodging has strong growth potential over the next five to 10 years.

Eric Moffett, portfolio manager of the Emerging Markets Equity Strategy, suggested it is worth paying attention to sectors where import substitution means that local firms are catching up with, and in some cases overtaking, their traditionally dominant foreign competitors. “In the detergent industry, Blue Moon has superseded Procter & Gamble3 as the dominant player, while hotels group Huazhu has been rapidly taking market share from Marriott, and sportswear firm Li Ning is seriously challenging Nike,3” Moffett said.

He suggested that the Chinese software industry is often overlooked by foreign investors—perhaps unfairly. “There are some really good companies that don’t get the attention that the Chinese internet companies have, but probably deserve a bit more attention,” he said.

“Overall, the current environment is probably as good as it will ever get for us as stock pickers as visibility is low and short‑term investors are selling at any price,” Moffett added. “There’s a lot of mispricing out there, which is providing some very good buying opportunities. We also believe that many firms are obscuring their profitability and holding back on pulling profitability levers given the political implications of earning too much when the economy is struggling. When the government’s focus shifts from politics to the economy, these firms will be ready to rev up their engines.”

Low Inflation Gives Authorities a Key Advantage

It was clear from our panelists’ comments that they refute the suggestion that China is uninvestible. Although China may be going through an extended regulatory cycle, it is just that—a cycle. Indeed, all eight speakers agreed that in five years’ time, China will be more investor‑friendly than it is today.

In the nearer term, a key factor in China’s favor is that it remains an outlier in a world of surging inflation. Consumer prices continue to rise modestly, giving the authorities the scope to ease monetary conditions—a privilege enjoyed by very few countries in the world at present. This latitude to adopt a softer stance could prove crucial: Further COVID‑19 outbreaks notwithstanding, China will likely need to stimulate the economy if it is to come close to hitting its targeted gross domestic product number for the year.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.