February 2022 / INVESTMENT INSIGHTS

Restored Supply Chains Should Propel a Eurozone Recovery

Higher yields and a stronger euro are likely

Key Insights

- COVID‑related supply chain disruption was a major impediment to eurozone manufacturing in 2021.

- The restoration of supply chains could fuel a strong recovery in the currency bloc this year.

- A sell‑off in bunds is likely to push yields firmly into positive territory, while the euro is likely to strengthen against the US dollar.

The eurozone economy was buffeted by a series of major headwinds in 2021, including the global supply shortage, surging gas prices, rising inflation, weaker demand and falling retail sales. As a result, the currency bloc’s economy slowed significantly over the last months of the year. There are signs, though, that some of these headwinds may turn into tailwinds in 2022, pushing up bond yields and strengthening the euro.

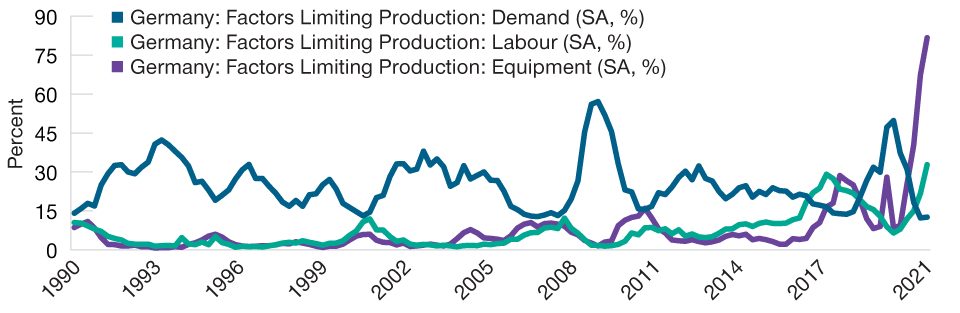

Industrial production was weak through the second half of last year, which was notable given that we were in the early stages of an economic recovery at the time. Financial markets took note, and the bund yield curve almost inverted in August 2021 amid concerns over weak demand threatening the recovery. Interestingly, surveys show that 12.6% of German firms cited demand as an impediment to production in the fourth quarter of last year—a figure that would normally be associated with a strong recovery (Figure 1).

Supply Chain Issues Have Hit German Manufacturing

(Fig. 1) Firms say weak demand has had much less impact

As of 31 December 2021.

Source: European Commission/Haver Analytics.

However, just over 80% of German firms cited a lack of equipment as an impediment to production, which suggested that supply chain disruptions played a much bigger role in industrial production weakness than fragile demand. Indeed, the German statistical office indicated that the German economy contracted between 0.5% and 1% in the fourth quarter of 2021, citing supply chain disruptions as an important determinant of the disruption.

Last year’s supply chain issues had several causes. One was the fact that container ships were stranded in the wrong parts of the world after the 2020 COVID outbreak, resulting in a 250% rise in the price of shipping goods between Asia and Western countries. Another was a lack of truck drivers to transport containers to their destination. Rising energy costs also contributed to supply problems because they drove up the price of locally produced steel and aluminium, fuelling demand for substitutes from elsewhere and leading to high container prices. Finally, the zero‑COVID policy implemented across Asia often led to localised shutdown of key factories, exacerbating the global shortage of computer chips, which are essential for the manufacture of many goods.

These supply chain issues have raised the prices of manufactured goods and their relevant inputs significantly. In November, for example, UK manufacturing total order books reached their highest level since 1977, when UK inflation was running at 17.5%.1 However, rising prices incentivise producers to increase production of both manufacturing goods and their inputs—and it is this desire to maximise profits that we believe is likely to eventually resolve ongoing supply chain issues. Indeed, Purchasing Managers’ Index surveys show that supply chain constraints have reached the peak and are beginning to ease. If the degree of easing seen in the last three months continues in the next six months, supply chain indicators will begin to enter the normal range seen in the pre‑pandemic period.

Strong demand for eurozone‑manufactured goods will likely result in a broad‑based rise in production once supply constraints ease. Orders for industrial goods in the bloc have continued to rise rapidly and are now above the level they reached in 2019—indeed, surveys show that German order book levels are at the highest level since the historical peak in 1969. As industrial production has remained weak, some of these orders have been filled from producers’ inventories—however, inventories are at historically low levels, and there is a seven‑months‑long production backlog (a record high in the automotive sector).

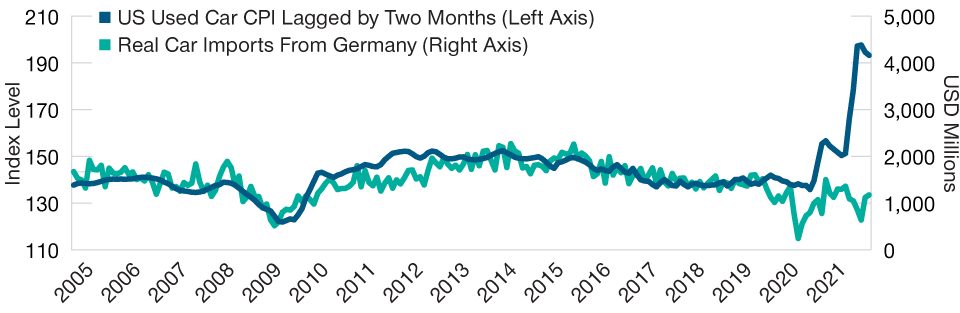

Because these orders have already been taken, the data suggest that, at face value, industrial production would grow by 10% if the current supply constraints eased. Furthermore, demand for motor vehicles and other industrial products remains very strong. Since the prices of new cars are typically fixed, used car prices are a reliable indicator of vehicle demand in the US. The historical relationship with imports suggests a 50% rise in demand for German car imports. Overall, the data show that industrial production will recover very strongly once supply constraints ease.

The omicron variant is a short‑term risk to the recovery of supply chains. While the omicron wave may have peaked already in the UK, there remains a risk of a large number of Continental European workers isolating at the same time, potentially leading to factory closures. Survey data from the UK experience indicate that manufacturers have lost roughly 10% of working days due to omicron‑related staff absences. However, just like in the UK, any such workforce shortage in Europe is likely to be short‑lived, meaning that the resumption of normal production levels would only likely be delayed by a month or so. The German economy likely contracted in the fourth quarter of 2021, and if labour shortages contributed to a second negative quarter, the German economy would have entered a technical recession. However, this weakness will likely be followed by a strong recovery due to the short‑lived effect of omicron‑related absences on labour supply.

Used Car Sales a Good Sign for German Automakers

(Fig. 2) Exports to US set to rise when supply problems ease

As of 30 November 2021.

Source: Bureau of Labor Statistics/Haver Analytics.

Of greater risk is the omicron variant exacerbating supply chain disruption in several key Asian countries, including China. China will host the winter Olympics this year and continues to lock down individual cities at even the smallest sign of COVID‑19 outbreaks as part of its zero‑COVID policy. Although China has so far successfully managed to contain many mini outbreaks, imposing more broad‑based and longer‑lasting lockdowns is the biggest risk to the recovery of eurozone supply chains. Indeed, containment measures in the Chinese city of Tianjin led to the closure of a VW-owned factory from 10 January. The negative supply chain effects could intensify as China’s authorities confront the more contagious omicron variant. However, even in that worst‑case scenario, the easing of supply chain constraints would be delayed by three to six months but probably not derailed, as the demand for manufactured goods will remain strong and the imbalance between orders and production continues to growth over time.

Rising Yields and a Stronger Euro Loom

Following the strong growth rates after the post‑lockdown reopening of economies, growth had to moderate back to historical levels. However, in the face of a slowdown in key export markets such as China and the prospective reduction in US fiscal stimulus, financial markets became concerned about the weak industrial production outturns in the eurozone. Recently, the focus has shifted to inflation and the European central bank’s (ECB’s) reaction to it, with less attention paid to activity developments. The latest data imply that output in Germany contracted by between 0.5% and 1%, but this was mainly due to supply chain disruptions. While staff absences due to the rapid spread of the omicron variant could push Germany into a technical recession, the current supply chain constraints will likely continue to ease in the next six months.

The prospect of a large rise in eurozone industrial production due to easing supply chains from the second quarter of 2022 onward is not currently fully priced into financial markets. However, we believe it is something that investors should be mindful of. The German bund sold off sharply in December and early January, and a strong recovery in industrial production would likely prompt a further sell‑off, pushing the 10‑year bund yield firmly into positive territory. The euro would also likely rise against the US dollar from its current low level because financial markets would price a more hawkish ECB, but also because the eurozone would start recording larger trade surpluses, thereby lifting the euro. Importantly, even in a worst‑case scenario of intensifying COVID containment measures in China, the supply chain‑driven recovery would be delayed by three to six months, but not derailed. And even if this were to happen, we believe that the euro and bund yields would end the year higher than they started it.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

February 2022 / INVESTMENT INSIGHTS