May 2021 / INVESTMENT INSIGHTS

Complacency creates inefficiency in EM corporates

Amid broad-based buying, markets have been paying less attention to issuer-specific risks recently. But this may be changing.

Inefficient markets can be good hunting ground for active security selection, and emerging market (EM) corporate bonds are a case in point. Structural features—few specialised EM credit investors in the market; a tendency towards wide price dispersion; and high research intensity—can create information gaps and mispricings for active managers to exploit. Since late 2020, we’ve seen an additional source of inefficiency in the form of market complacency, which in some cases led to incorrect pricing of risk. But that is now changing.

The beta rally (a rising tide floats all boats)

Over roughly the past six months, the search for yield, together with ample liquidity created by accommodative monetary policy, has seen more investors put money to work in EM corporates. This created a market-wide rally in which negative headlines (for example Covid-related developments in Brazil) did little to interrupt the spread tightening trend. One explanation for the resilience was that still-attractive valuations offered more compensation for risk than they do today. Another is that, given the relative illiquidity of the markets, investors might have been reluctant to sell for fear of not being able to buy back in later.

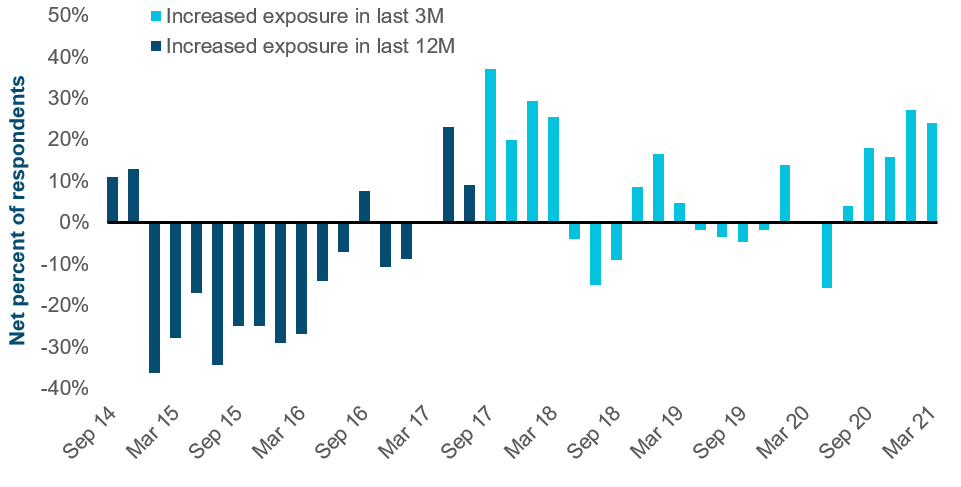

Anecdotally, in the past six months our traders have been reporting higher than usual participation by crossover investors in the new issue market, and that this seems to have been anchoring demand. Recent research by BofA Global Research showed that a net 24% of US investment grade investors reported higher exposure to EM corporates, moderating from a net 27% in January (see chart).

Also anecdotally, we have been seeing increased interest in EM corporates from, for example, US investors who might previously have ventured into domestic high yield but would not have looked at emerging markets. We are telling clients that the rest of 2021 is more likely to be about the alpha opportunity than the beta opportunity. In other words, rather than riding the wave of a broad market rally, the value will come from identifying idiosyncratic, company-specific opportunities.

US investment grade investors report increased EM corporate bond exposure

As of 31 March 2021

Source: BofA Credit Investor Survey, Bank of America

Fundamentals back in focus

Historically, during beta rallies, buying becomes more indiscriminate, there’s less scrutiny of issuerspecific fundamentals, and underlying risks get mispriced. This of course creates a window for active managers to identify those anomalies before the market starts to focus on fundamentals again.

The first quarter of 2021 brought increased interest rate volatility, led by US Treasuries, and the steady tightening in credit spreads started to flatten off. In the last month or so, the market has been noticeably less complacent about negative headlines, and we’ve started to see increased spread volatility..

For example, Peruvian bonds sold off in April as far-left candidate Pedro Castillo, running on a platform of resource nationalisation, unexpectedly won the first round of the presidential elections.

And when Colombia, which is on the cusp a downgrade to high yield, suffered setbacks to implementing a planned reform package, the market was quick to price in a more immediate risk of a downgrade.

Perhaps the most arresting example of a wake-up call to investors is Huarong. With more than US$20 billion in outstanding debt, the Chinese asset manager is widely held, despite a chequered governance record (a former chairman was executed this year for crimes including abuse of power to allocate credit). In our view, given the entity’s opaque business model and inadequate levels of disclosure, any investment thesis rests almost entirely on Huarong’s status as a central government state owned enterprise (SOE).

Until recently, it was taken as read that, unlike some local-government SOEs, no central government SOE would be allowed to fail, but that assumption is currently being challenged. Coming at a time when the Chinese government is trying to deleverage the economy, there are fears that it might be more minded to make an example of Huarong tosend a message to the markets. Given the potential systemic impact of such a move, we are unconvinced that Huarong would be allowed to fail, but bond values are currently in limbo as investors grapple with how to price the risks.

The current opportunity

We wouldn’t be surprised to see further isolated flare-ups of volatility in the coming months, particularly as liquidity is likely to decline as we enter the quieter summer months. That said, the overall market remains in a healthy state (for example, the VIX volatility index remains below 20 and commodity prices remain supportive). Corporate fundamentals should improve further after the trials of 2020, though arguably much of this is already priced in.

In terms of our risk stance, we’re currently running a fairly defensive portfolio, with minimal carry versus the benchmark. Generally we are finding the most opportunities in higher-quality markets such as China, Mexico and India. Other opportunities include corporates in Oman, which benefits from positive reform momentum and a supportive commodity price backdrop.

Our focus is on credit improvement stories or those with idiosyncratic drivers, which admittedly are harder to find as spread dispersion has declined. We have a more favorable medium-term view as the current recovery in developed markets should eventually make its way into our markets, despite slower vaccine roll-outs, and macro headwinds such as withdrawal of fiscal stimulus, election risks, geopolitical tensions and a credit slowdown in China.

Risks - The following risks are materially relevant to the portfolio:

- China Interbank Bond Market risk - market volatility and potential lack of liquidity due to low trading volume of certain debt securities in the China Interbank Bond Market may result in prices of certain debt securities traded on such market fluctuating significantly.

- Contingent convertible bond risk - contingent convertible bonds have similar characteristics to convertible bonds with the main exception that their conversion is subject to predetermined conditions referred to as trigger events usually set to capital ratio and which vary from one issue to the other.

- Country risk (China) - all investments in China are subject to risks similar to those for other emerging markets investments. In addition, investments that are purchased or held in connection with a QFII licence or the Stock Connect program may be subject to additional risks.

- Credit risk - a bond or money market security could lose value if the issuer’s financial health deteriorates.

- Default risk - the issuers of certain bonds could become unable to make payments on their bonds.

- Derivatives risk - derivatives may result in losses that are significantly greater than the cost of the derivative.

- Emerging markets risk - emerging markets are less established than developed markets and therefore involve higher risks.

- Frontier markets risk - small market nations that are at an earlier stage of economic and political development relative to more mature emerging markets typically have limited investability and liquidity.

- High yield bond risk - a bond or debt security rated below BBB- by Standard & Poor’s or an equivalent rating, also termed ‘below investment grade’, is generally subject to higher yields but to greater risks too.

- Interest rate risk - when interest rates rise, bond values generally fall. This risk is generally greater the longer the maturity of a bond investment and the higher its credit quality.

- Liquidity risk - any security could become hard to value or to sell at a desired time and price.

- Sector concentration risk - the performance of a portfolio that invests a large portion of its assets in a particular economic sector (or, for bond portfolios, a particular market segment), will be more strongly affected by events affecting that sector or segment of the fixed income market.

General Portfolio Risks

- Capital risk - the value of your investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the portfolio and the currency in which you subscribed, if different.

- Counterparty risk - an entity with which the portfolio transacts may not meet its obligations to the portfolio.

- ESG and sustainability risk - ESG and sustainability risk may result in a material negative impact on the value of an investment and the performance of the portfolio.

- Geographic concentration risk - to the extent that a portfolio invests a large portion of its assets in a particular geographic area, its performance will be more strongly affected by events within that area.

- Hedging risk - a portfolio's attempts to reduce or eliminate certain risks through hedging may not work as intended.

- Investment portfolio risk - investing in portfolios involves certain risks an investor would not face if investing in markets directly.

- Management risk - the investment manager or its designees may at times find their obligations to a portfolio to be in conflict with their obligations to other investment portfolios they manage (although in such cases, all portfolios will be dealt with equitably).

- Operational risk - operational failures could lead to disruptions of portfolio operations or financial losses.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.