July 2022 / BLOG

Russia’s Invasion of Ukraine Prompts U.S. Energy Policy Shift

The U.S. natural gas industry may enjoy some emerging policy tailwinds

Russia’s invasion of Ukraine highlighted the vulnerability of European countries that depend heavily on energy imported from Russia. It has also spurred a rethinking of U.S. energy policy, with the Biden administration moving toward a more favorable view of domestic natural gas.

We also see the potential for the White House to take some actions in the near term to respond to higher oil prices. However, the policy backdrop for U.S. oil producers is likely to remain challenging in the medium term.

These pragmatic adjustments to U.S. energy policy, in our view, do not reflect any wavering in the White House’s commitment to the transition away from fossil fuels. Rather, the administration’s legislative and regulatory initiatives suggest that President Biden is still taking a whole-of-government approach to pursuing his long-term goals for decarbonizing the U.S. economy.

Natural Gas and European Energy Security

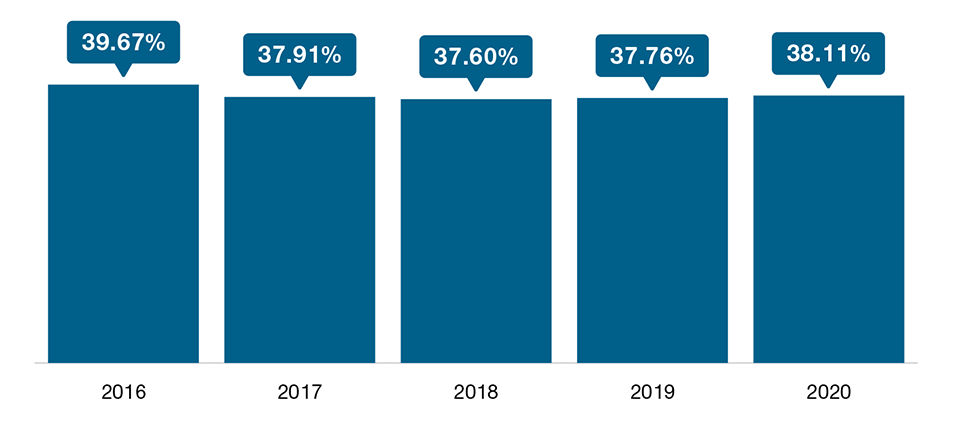

Historically, more than 35% of the natural gas that the European Union (EU) imports each year has come from Russia (Figure 1).

The European Union (EU) Has Relied Heavily on Energy from Russia

(Fig. 1) Percent of annual EU natural gas imports sourced from Russia

As of December 31, 2020.

Source: Eurostat. Data analysis by T. Rowe Price.

Whereas coal and crude oil are readily shipped around the world, logistical constraints mean that replacing natural gas shipments from Russia with alternative supplies would not be easy or quick. Europe would need to expand its access to liquefied natural gas, or LNG. Here is how the LNG value chain works:

- Liquefaction plants chill the natural gas to about -260°F, at which point the thermal fuel condenses into liquid form.

- The LNG is shipped overseas in specialized vessels.

- Regasification facilities convert the LNG to its gaseous state, after which it can enter the pipeline network for distribution.

Adopting this course would mean significant infrastructure spending on the supply side and the demand side to increase capacity. LNG projects usually take several years to complete, and long-term sales agreements are needed to secure financing. Europe’s pipeline system would also likely need to be fundamentally replumbed to distribute these volumes to areas of need.

Potential Policy Tailwinds for U.S. Natural Gas

Policy support on both sides of the Atlantic could help to move key LNG projects forward. The European Commission said it would work to ensure stable demand for a significant uptick in U.S. LNG through 2030. The U.S., which boasts abundant shale gas reserves, agreed to adopt regulatory policies that would support projects to expand LNG export capacity.

How might the regulatory environment for natural gas improve?

The White House has various levers at its disposal to encourage regulatory agencies to speed up the approval of export licenses and construction permits for LNG terminals. Such steps could help exporters obtain financing and secure long-term contracts with customers. Over the past four months, the prospect of a supportive regulatory framework and the wide price spread between Gulf Coast natural gas prices and those in Europe and Asia have contributed to a flurry of long-term offtake agreements for to-be-built LNG export capacity.

The development of new LNG export capacity agreements would likely give U.S. energy producers the certainty they need to ramp up output over time. This improved visibility would also benefit some companies that own gas pipelines and processing infrastructure.

But Biden remains focused on reducing carbon emissions, in our view. We expect the administration to prioritize curtailing natural gas emissions from wells and pipelines. Although natural gas produces less carbon dioxide than coal when burned, it is a potent greenhouse gas when released directly into the atmosphere. Methane leak rates from natural gas production will likely be a key focus for regulators.

Crude Realities

With high oil prices causing pain at the pump as the summer driving season approaches, the Biden administration is likely to take some actions in the near term to respond to these pressures.

Possible options could include faster well permitting in an effort to boost oil production in the short term and/or policy adjustments that would aim to provide some near-term relief on gasoline prices.

That said, we believe that the medium-term policy backdrop for the U.S. oil production complex is likely to remain challenging.

Committed to the Energy Transition

Even with the Biden White House appearing to take a more constructive view on U.S. LNG exports, the administration remains committed to pursuing initiatives that advance its long-term goals of significantly reducing carbon emissions.

The Securities and Exchange Commission, for example, is likely to push ahead with implementing rigorous climate disclosure requirements for public companies, while the Environmental Protection Agency recently issued stricter emissions standards for 2024 and 2025 automobile models.

Promoting adoption of renewable energy also remains an area of focus.

The USD 1.2 trillion bipartisan infrastructure bill passed last fall included USD 73 billion for upgrades to the nation’s power grid. This funding is likely to be critical to the U.S. energy transition because these projects can help the system to accommodate a higher proportion of intermittent wind and solar power.

And the White House continues to push for the passage of the Build Back Better Act, which includes line items that would extend and expand tax credits for clean energy projects and electric vehicles and create new ones for emerging technologies that could advance the transition from fossil fuels.

Even if this legislation were to fail, we could see extensions of tax credits for wind and solar power later in the year, as these measures historically have enjoyed bipartisan support.

We view the clean energy transition as a durable secular trend that could enjoy tailwinds due to the Biden administration’s support.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

July 2022 / INVESTMENT INSIGHTS