April 2024 / INVESTMENT INSIGHTS

Vietnam: Asia’s next frontier tiger

Tailwinds are gathering to support another major leap

Key Insights

- Vietnamese stocks appear cheap despite a cyclical recovery, an expanding consumer economy, and a looming upgrade to emerging market status.

- A raft of technical and regulatory measures are set to make the stock market more accessible to overseas investors.

- The banking and information technology sectors in particular are well placed to possibly outperform when stock prices respond to improving fundamentals.

Economic reforms have propelled Vietnam from one of the world’s poorest nations to a middle‑income economy in a matter of decades. Now, with a cyclical recovery underway, favorable demographics, and an upgrade to emerging market status (EM) within sight, the country appears poised for another major step in its transformation. Yet investors remain cautious and valuations are cheap. Neither of these is likely to last.

Vietnam’s journey over recent decades has been remarkable. After the Vietnam War ended in 1975, the country remained under a U.S. trade embargo until 1994. Market‑friendly reforms introduced in the mid‑1980s attracted successive waves of foreign investment and boosted exports. In 1995, the country joined the Association of Southeast Asian Nations (ASEAN), and accession to the World Trade Organization followed in 2007. Then in September 2023 it signed a “comprehensive strategic partnership” with the U.S., putting its relations with America on the same level as Russia and China.

Position vacant for China alternative

With confidence in China diminishing amid rising labor costs, a poor economic outlook, and the prospect of a prolonged trade war with the U.S., Vietnam is in pole position to attract manufacturers looking to reduce exposure to Beijing. From an economic standpoint, Vietnam looks attractive. Its overall 2023 gross domestic product (GDP) growth of 5% was down from the previous year’s 8%, weighed down by falling exports amid weak global demand and an intensification of the government’s crackdown on corruption in the property sector. However, property transactions and prices are increasing, while exports and foreign direct investment (FDI) data are also improving.

FDI into Vietnam was USD 2.8 billion in the first two months of this year, up 9.8% from the same period in 2023, according to the Ministry of Planning and Investment. FDI pledges, which serve as an indicator of future FDI disbursements, surged by about 40% year on year. The top sources of investment were Singapore, Hong Kong, and Japan, while Samsung, which employs more than 110,000 people in Vietnam, remains the largest foreign investor in the country. In December, Jensen Huang, CEO and chair of U.S. tech giant NVIDIA, visited Hanoi to announce plans to establish a manufacturing base in Vietnam.

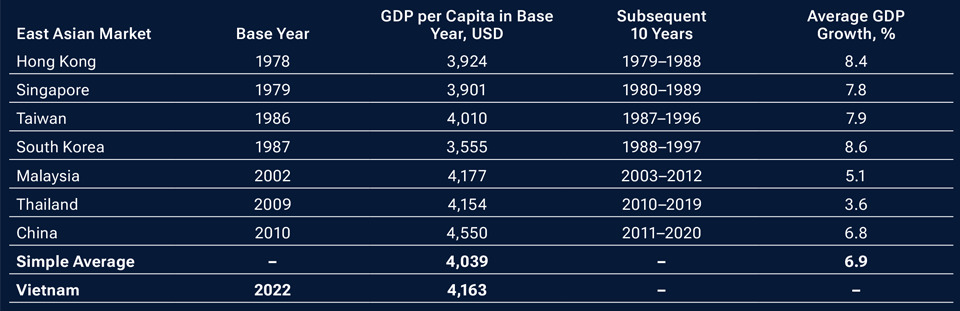

GDP growth is expected to recover to 6% this year and reach 6.5% in 2025. According to the World Bank, Vietnam’s current GDP per capita in 2022 was USD 4,163—similar to levels that several other Asian tigers have recorded ahead of decade‑long growth surges (Figure 1).

A period of rapid expansion looms

(Fig. 1) GDP per capita mirrors Asian tigers before growth spurts

As of February 2024.

Sources: GSO, World Bank, Vietcap. Analysis by T. Rowe Price.

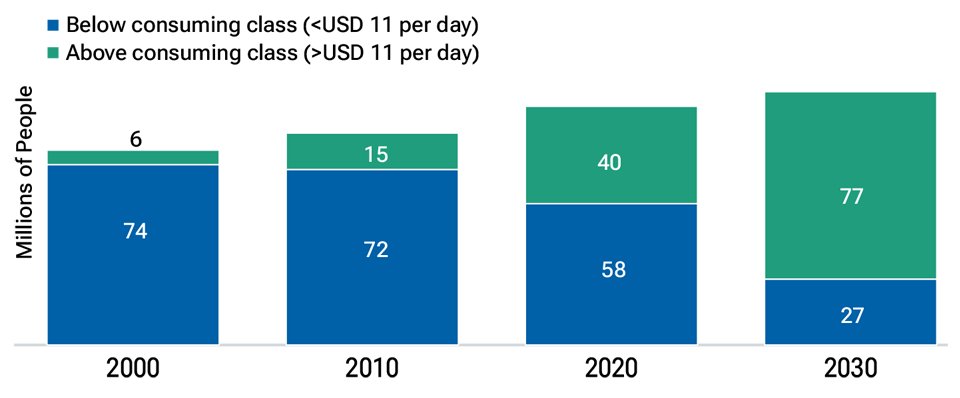

Structural factors are also favorable. Vietnam has a well‑balanced economy and currently runs both a current account surplus and a trade surplus. Its 2023 debt‑to‑GDP ratio of 37% was moderate compared with many of its competitors. Demographics continue to power growth: At the turn of the millennium, Vietnam’s middle class comprised around 6 million people; by 2030, it is expected to be more than 75 million. With a large and youthful population and workforce, Vietnam is turning into a classic consumer economy (Figure 2).

Vietnam is becoming a consumer economy

(Fig. 2) Its middle class is expanding rapidly

Actual outcomes may differ materially from estimates. Estimates are subject to change.

As of December 2021.

Source: “The new faces of the Vietnamese consumer.” McKinsey & Company, December 2021.

Note: Members of the consuming class are defined as having sufficient income to pay for necessities such as food, shelter, and clothing, as well as discretionary goods and services. Income group defined by daily spending (based on 2011 purchasing power parity). Most recent data available.

Vietnam’s main bourse, the Ho Chi Minh City Stock Exchange (HoSE), is currently classified by FTSE and MSCI indices as a frontier market, a status that effectively prevents many overseas investors from investing in it. Vietnam is seeking an upgrade to emerging market status, which, according to the World Bank, could generate foreign net inflows of USD 30 billion by 2030. The HoSE looks likely to achieve this with FTSE after revealing plans to relax its “pre‑funding” settlement procedures for foreign investors—which has been a key obstacle in Vietnam’s bid for emerging market status.

Despite reports that an announcement on Vietnam’s inclusion in the FTSE Emerging Index could come as early as this September, bureaucratic delays mean that the pre-funding hurdle will probably not be resolved until August—leaving FTSE with too little time to consult investors ahead of its annual index inclusion announcement in September. As such, the announcement of Vietnam’s inclusion in the FTSE Emerging Index will more likely take place in 2025.

An upgrade to the MSCI Emerging Markets Index will take longer as MSCI’s requirements for access by foreign investors are stricter. If these requirements are satisfied, Vietnam could join China, Indonesia, Qatar, and the Philippines in moving up from the MSCI Frontier Markets Index, which it currently shares with smaller markets such as Morocco, Sri Lanka, and Kenya. Vietnam is comfortably the largest component of the MSCI Frontier Markets Index, composing 28% of the index at the end of February this year. Confirmation of Vietnam’s upgrade to the MSCI EM Index is likely to come between 2026 and 2028.

However, MSCI EM Index inclusion will only be the cherry on the cake—investor interest in Vietnam is likely to increase long before then. In early March, the HoSE trialed its new Korea Exchange (KRX) technology system, which is intended to significantly upgrade the infrastructure of the Vietnamese stock market and improve stock market liquidity. Further flexibility will come when the pre‑funding solution mentioned above arrives later in the summer, which should drive greater foreign interest.

Stocks have yet to recover from 2022 slump

Combined, these three factors—the reversal of cyclical headwinds, favorable structural conditions, and the regulatory and technological measures to enable an upgrade to EM status—make a compelling case for investing in Vietnam. Yet the VN‑Index, which represents the Ho Chi Minh City Stock Exchange, is trading at low levels. The index slumped by a third in 2022 as valuations of real estate companies (which constitute a fifth of the index) collapsed amid a liquidity crunch and the government anti‑corruption crackdown mentioned above. Although the market recovered somewhat last year, at the end of March the VN‑Index was still trading well below its 2022 peak and at a one‑standard‑deviation discount to its historical average forward price‑to‑earnings ratio of 13x.

This is mainly because local investors (which account for 90% of stock market turnover) are still bruised from the recent slump in exports and fall in property prices, which badly damaged sentiment. However, there is a lot of money sitting on the sidelines that is ready to be deployed as the economy gets stronger and consumer sentiment, which tends to be a lagging indicator, improves.

Another reason for the relative cheapness of Vietnamese stocks is continuing hesitancy among foreign investors when it comes to frontier markets. Investors tend to prefer putting their money into markets where others have gone before; frontier markets are regarded with caution because they are less explored than developed markets and are seen as less liquid and more bureaucratic.

While it is true that the Vietnamese stock market is less liquid than those of developed markets, it is more liquid than several large emerging market countries. The Vietnamese stock market typically trades more than USD 1 billion of securities per day, which is the second highest among the 10 ASEAN countries and nearly five times higher than some established EM countries such as Mexico. The liquidity of the Vietnamese stock market is likely to deepen as the regulatory and technological changes mentioned above take hold.

Bureaucracy is a hurdle. It can take a long time to get things done in Vietnam. In this respect, Vietnam is behind China, where the authorities can plan and execute major infrastructure projects in a very short amount of time. However, the government seems intent on tackling this. In a speech to parliament in November, Prime Minister Pham Minh Chinh admitted that bureaucracy is a burden on enterprise and pledged to streamline outdated administrative procedures to support business and boost growth. It is also worth noting that Vietnamese infrastructure investment as a percentage of GDP remains nearly twice that of regional rivals such as Thailand and Malaysia.

A final factor in the undervaluation of Vietnamese stocks is the inefficiency of the market. The relative lack of overseas investment in—and analyst coverage of—frontier markets means that pricing does not always accurately reflect fundamentals. Positive developments such as those described above may take a while to be reflected in stock prices.

Reforms key to unlocking growth

Further moves to reduce bureaucracy would be welcome. Earlier this year, the National Assembly approved a new Land Law, aimed at removing bottlenecks in securing overseas investment in the property sector. It will come into effect in January next year. Then in late March, the State Securities Commission, Vietnam’s stock market regulator, released a draft regulation amendment addressing obstacles to foreign investment. There is much work to be done on this, but it is a step in the right direction. The removal of further inefficiencies would, in our view, unlock structural growth that could significantly boost GDP.

If Vietnam continues to push key reforms and make itself more accessible (as we believe it will), it will only be a matter of time before more overseas investors are persuaded by its powerful growth story to look more closely at Vietnamese stocks. For those who do, the banking sector, which is currently in the early stage of a cyclical recovery, looks particularly interesting. Valuations remain attractive as the cyclical recovery has yet to be priced in. The key question is the scale and duration of the recovery in the banking sector. In our view, current prices do not reflect its potential by some measure.

Another interesting sector is information technology (IT). Vietnam has many highly skilled coders who cost around 90% less than those in the U.S. and 15% less than those in India. The availability of high‑quality coders at relatively low cost is helping Vietnam to establish itself as a major regional technology center. Management consultancy firm Kearney’s latest Global Services Location Index, published last year, ranked Vietnam as the seventh most attractive location in the world for IT outsourcing. “The presence of major technology companies demonstrates that the country is a global digital hub, motivating it to continue upskilling its workforce,” the report said.

We expect these trends to continue over the coming years. And while the investment case for Vietnam will be strengthened considerably when upgrades to the EM indices of FTSE and MSCI are achieved, it is not dependent upon them. Many positive developments are already occurring that, in our view, make Vietnam one of the most compelling investment opportunities in the world.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

April 2024 / INVESTMENT INSIGHTS

April 2024 / INVESTMENT INSIGHTS

Johannes Loefstrand is the portfolio manager of the Frontier Markets Equity Fund.

Eric Veiel is head of Global Investments and chief investment officer, chair of the Investment Management Steering Committee, and member of the Management Committee, the Equity Steering Committee, the Fixed Income Steering Committee, the International Steering Committee, the Multi-Asset Steering Committee, the Product Steering Committee, and the Management Compensation and Development Committee. Eric also is a member of the Board of the T. Rowe Price Mutual Funds.