January 2023 / INVESTMENT INSIGHTS

Five Key Insights From 2022

Uncertainty persists, but yield is back and fundamentals matter

Key Insights

- The Fed is committed to do whatever it takes to curb inflation. Meanwhile, a focus on socially oriented goals could impact economic policies in China.

- The rout in bonds helped to restore healthy yields but reminded investors that stocks and bonds can sometimes sell off at the same time.

As we reflect on a momentous year, I would like to share these five insights from 2022 that I believe will continue to influence financial markets in the new year.

1. Valuation matters.

After starting the year at elevated levels, equity valuations quickly adjusted downward once investors realized that steep interest rate hikes were imminent. While equity markets sold off meaningfully during 2022, earnings expectations fell only modestly. This, unfortunately, means that a decline in earnings expectations in 2023 due to a global recession could worsen the sell‑off in stocks.

2. The Fed remains committed to fighting inflation.

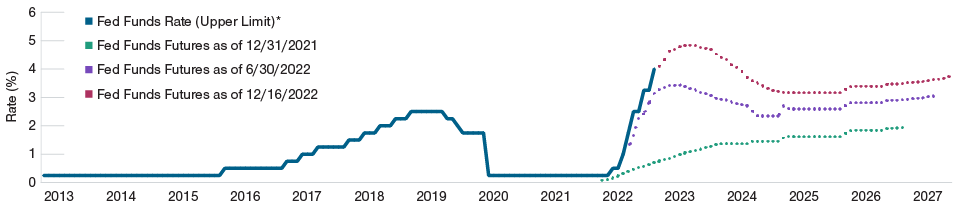

The Evolution of Fed Market Expectations

(Fig. 1) The Fed will choose fighting inflation over supporting the economy

*January 2013 to November 2022, futures estimates through August 2027.

Actual outcomes may differ materially from estimates. Estimates are subject to change.

Source: Bloomberg Finance L.P.

Market expectations for the federal funds rate were consistently too low in 2022 (Figure 1). In fact, how high the Federal Reserve will raise rates and how long they will hold them at elevated levels remains unknown. What is clear is that they are determined to avoid a replay of the 1970s and will do whatever it takes to get inflation back to healthy levels, even if their actions push the U.S. economy into recession. In 2023, the Fed’s primary focus will be on lowering wage inflation, and we should not expect a shift in policy unless the labor market also weakens considerably.

3. China has changed.

The year 2022 proved to be one of considerable change in China, which saw the leadership of President Xi Jinping extended. Notably, while the Chinese government has indicated that economic growth remains important, it intends to reinvigorate socially oriented goals. This could lead to less predictable economic policy changes in the future. We were surprised by the easing of COVID restrictions in December, and investors should be prepared for more uncertainty going forward.

4. Stocks and bonds can sell off simultaneously.

Bonds have historically offered ballast to investors’ portfolios when equities faltered. However, this has not always been the case, particularly in periods when the Fed embarks on a new hiking cycle, as happened in 2022. Further, 2022 was somewhat of an outlier because the Fed usually tightens when growth is accelerating—which was not the case in 2022—and interest rate hikes are typically more gradual. Fortunately, stock/bond correlations should likely fall in 2023, as the Fed appears close to the end of its hiking cycle.

5. Yield is back.

The silver lining to the rout in bonds during 2022 is that bonds have healthy yields once again. This means that investors no longer have to take significant credit risk to get a healthy yield from their bond portfolio. In addition, investors can also enjoy a potentially larger income buffer to help offset any further increases in interest rates and/or credit spreads1.

As we welcome 2023, we will continue to monitor these market themes and provide updates accordingly.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Tim Murray is a capital market strategist in the Multi-Asset Division. Tim is a vice president of T. Rowe Price Associates, Inc.