December 2022 / MARKET OUTLOOK

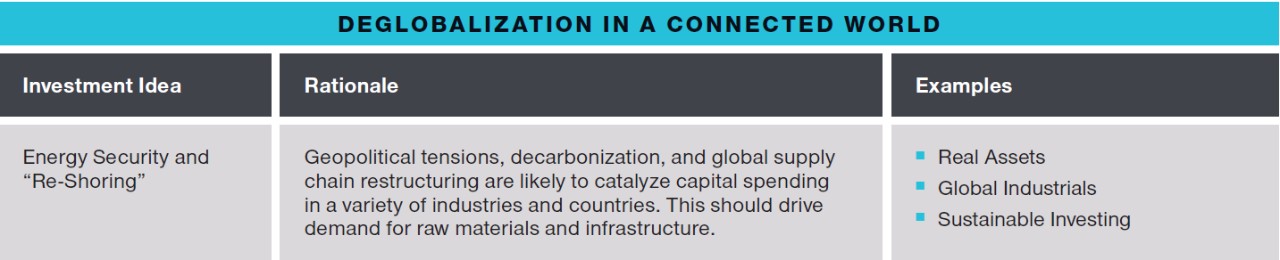

Deglobalisation in a Connected World

We are seeing a shift in the global economy that could shape the investment landscape for years to come.

Geopolitical tensions and supply disruptions have led some analysts to question whether an era of economic integration has ended, dimming prospects for productivity and growth. But that risk appears to have been exaggerated, the CIOs say.

“Globalisation isn’t dead. It may not even be dying,” Thomson argues. Economically, he notes, globalisation has been defined by the fivefold rise in international trade as a percentage of world gross domestic product since the early 1950s. While that ratio has stopped rising, it also isn’t falling, he notes.

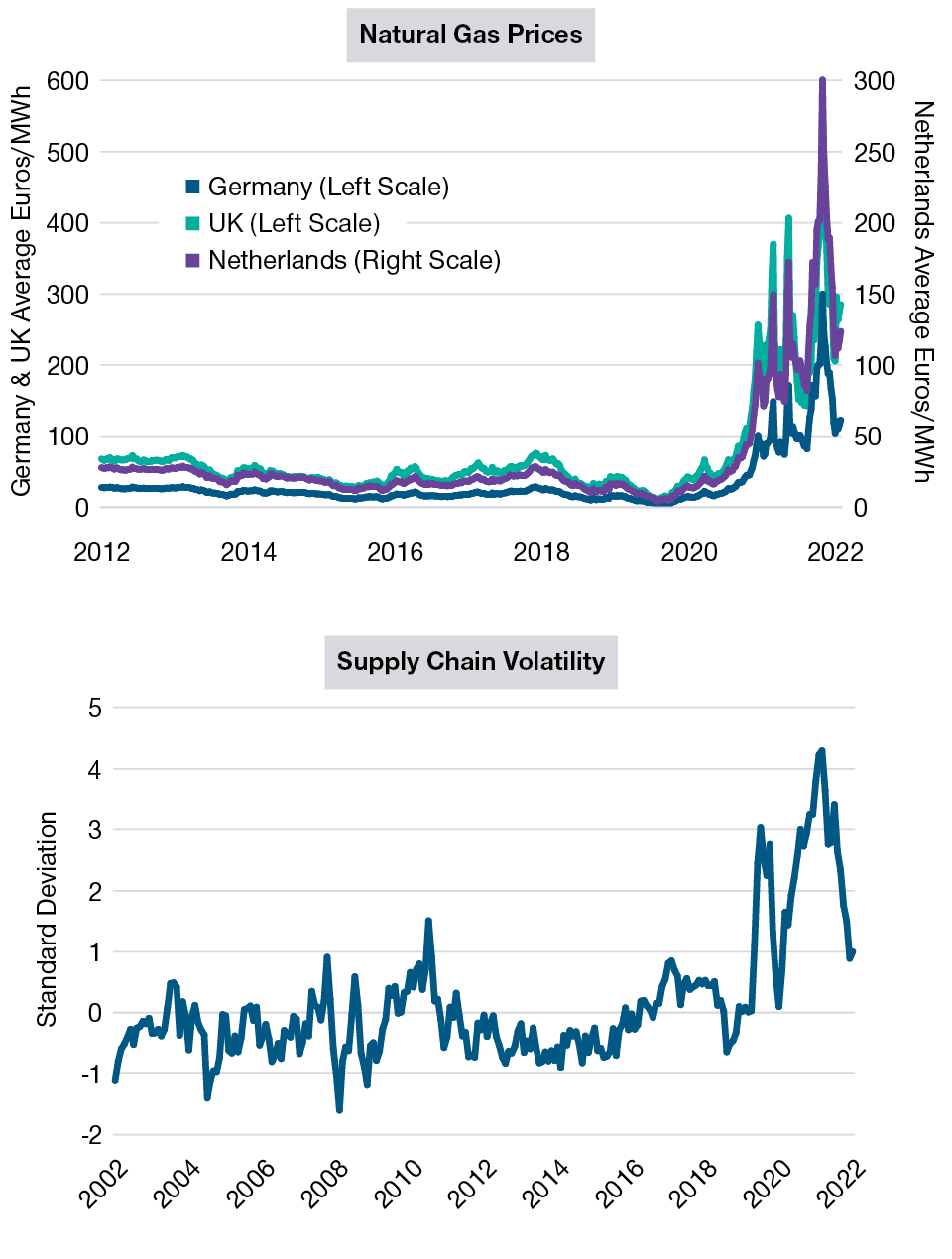

But recent events have shown that globalisation is changing, Thomson adds. A number of economies have become dependent on critical imports from one specific part of the world, he says. Europe’s heavy reliance on Russia for natural gas, for example, put its energy security at risk when the war in Ukraine sent gas prices soaring.

Market forces can correct such imbalances if given time, Thomson says. This was demonstrated by the large declines seen in European gas prices in the second half of 2022 (Figure 5, left) as demand forecasts were slashed and new supply was rerouted to those markets.

Over the longer run, Thomson argues, energy development could drive a massive global surge in capital spending on the transition from fossil fuels to renewable energy sources. “The numbers that will be required are mind‑boggling,” he says. “I’ve seen estimates as high as USD 100 trillion.”

Capital expenditures on that scale, Thomson predicts, should generate investment opportunities on an equally grand scale in the technology, materials, and capital goods sectors, as well as in alternative energy producers and efficiency innovators.

Global Supply Chains Are Healing

Widespread fears that COVID‑related supply shortages could linger for years, strangling global growth, also appear to have been overly pessimistic, Thomson notes. Instead, supply chain reliability improved steadily over the course of 2022 (Figure 5, right).

Moving into 2023 and beyond, supply chains in some industries are likely to be reconfigured to limit future disruptions, McCormick argues. This will impose frictional costs. “I think it supports Justin’s argument that inflation will be stickier and volatility higher going forward,” he says.

Although Supply Disruptions Have Eased, Geopolitical Risks Remain Elevated

(Fig. 5) Natural Gas Prices by Country and Volatility in the New York Federal Reserve’s Global Supply Chain Pressure Index

Past performance is not a reliable indicator of future performance.

Natural gas prices as of November 25, 2022. Supply chain index volatility as of October 31, 2022.

Sources: Intercontinental Exchange/Haver Analytics, Federal Reserve Bank of New York, Liberty Street Economics/Haver Analytics.

But adaption also will create potential opportunities for investors, McCormick and Thomson say. “The companies that can carve out important roles in the newer supply chains will be among the big winners,” McCormick predicts. “We think it could be the investing story of the next five years, if not the next decade.”

Skilled active management will be critical to take advantage of potential opportunities, McCormick adds. “Individual name selection will be important. The quality of management teams will become really important.”

A Contrarian Case for China

Investor anxiety about the economic and political future of China, the world’s second‑largest economy, weighed heavily on Chinese markets in 2022.

Trade and technology conflicts added to investor malaise, as the Biden administration unveiled new export controls designed to restrict China’s access to advanced semiconductor technologies.

“Sentiment about China has never been worse than it is now,” Thomson says. But Thomson thinks the pessimism has been overdone. His arguments:

- Easing COVID restrictions in China should help clear the way for an acceleration in economic and earnings growth.

- Despite a turn toward stricter market regulation, China’s political leaders, including President Xi Jinping, remain committed to a pro‑growth agenda.

- Much of China’s growth over the last three decades has come from property development. That era is coming to an end. But different sectors should continue to drive a more moderate pace of economic growth.

- Washington and Beijing both have an interest in avoiding a major break. “A large‑scale economic decoupling between the U.S. and China would be a mutually assured depression,” Thomson says. “It’s a frightening thought, but highly unlikely.”

“I understand that these issues will continue to weigh on asset valuations and raise capital costs,” Thomson concludes. “But I think we need to stay objective here, keep an open mind, and watch the data points as they evolve.”

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Download the full 2023 Global Market Outlook insights here

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.