October 2020 / MULTI-ASSET SOLUTIONS

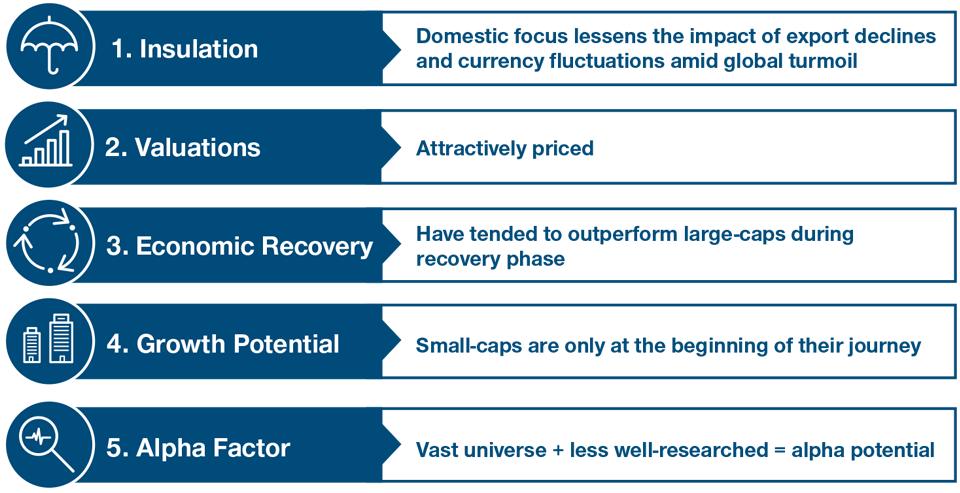

Five Reasons Why Investors Should Now Consider Small-Caps

Attractive valuations and prospects for economic recovery support small-caps

Key Insights

- Small‑caps are typically more immune to currency fluctuations, global economic turbulence, and rising geopolitical tensions compared with large‑caps.

- Supportive valuations and a potential economic recovery support the case for investment.

- Greater potential to add value through proprietary research as small‑cap markets tend to be less efficient than their large‑cap counterparts.

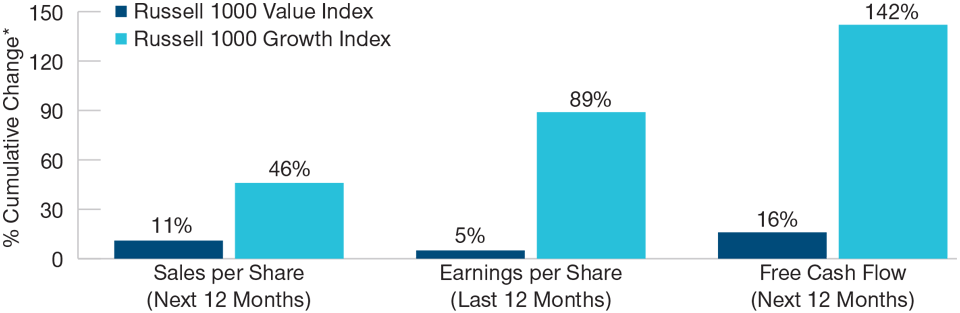

Global stock markets have staged a remarkable recovery from their lows in late March, despite recent volatility. This rebound, however, has not been even. In the U.S., large‑cap stocks have led the way. In particular, some of the marquee growth stocks have enjoyed the best of the returns as the market has recognized that certain companies would see their economic futures pulled forward by the disruption created by the coronavirus crisis. Unusually, growth stocks have showed market leadership before, during, and after a market crisis, albeit supported by greatly superior sales, earnings, and cash flow characteristics (see chart).

Why Small-Caps Can Punch Above Their Weight

By contrast, U.S. small‑cap stocks, as measured by the Russell 2000 Index, have performed poorly. It seems that in some cases the stock market recovery has eluded smaller companies. Empirical evidence, however, reflects that small‑caps historically outperform large‑caps over longer time periods. We have identified five potential drivers that could contribute to a reversal of small‑caps’ recent underperformance.

1. Better Immunization to Global Turmoil

Undeniably, the world faces major challenges right now. The coronavirus pandemic has decimated economic growth, with many economies remaining in deep recession as lockdown measures and disruption to global supply chains have impacted trade and services. Rising geopolitical tensions are also factors. China and the U.S. remain entrenched in a divisive trade war, and the rhetoric is heating up as we approach November’s U.S. presidential election. Meanwhile, with the U.S. economy faltering, the Federal Reserve has had to slash interest rates to near zero to support growth, putting pressure on the U.S. dollar.

But turmoil in the global economy and currency markets has more of an impact on companies that rely more heavily on exports. Small‑caps, on the other hand, typically focus on local markets to sell their produce and services, making them more immune to currency fluctuations and global economic turbulence relative to large‑caps.

2. When It Comes to Valuations, Size Does Matter

While the performance of stocks over the short term is largely driven by sentiment, over the long‑term, valuations matter. Using an equally weighted basket of valuation ratios (price to earnings, price to book, and price‑to‑cash flows) and comparing current levels with the past 15 years, small‑caps currently rank as one of the most attractively priced segments of the equity market.

Buying cheap just because it is cheap is not a good reason to buy, however. What comes down does not always go up again. But there are good reasons why small‑caps have underperformed. They are more sensitive to economic downturns within their own countries. They also have less chance of receiving fiscal aid from governments because they employ fewer employees compared with larger corporations. Additionally, they tend to feature higher concentration in the consumer, financial, and energy sectors—sectors that have not performed well in this current environment.

However, we believe the worst of the pandemic may be behind us and that both individual economies and the global economy as a whole could change direction. While valuations on their own may not be enough to push small‑caps forward, valuations plus an economic recovery may provide that catalyst.

Growth Stocks Leading on Key Metrics

Accelerating disruption has concentrated gains in large‑cap growth companies

*Cumulative changes represent differences between forward measures as of June 1, 2007, and June 30, 2020.

Source: T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.

3. Economic Recovery on the Horizon

It can be a challenge to be contrarian and go against the adage “make the trend your friend.” A catalyst is needed to convince investors to buy assets whose price is dropping. This catalyst may be the increasing prospect of economic recovery.

The good news, however, is that central banks are supportive, many governments are reopening economies, and, importantly, consumers seem to be gradually overcoming their fears and are beginning to consume again. The base case scenario is that an economic recovery is more likely over the next few quarters. There are risks—not least of which are the second wave of infections and the return of lockdown measures. But from here—a very low point—the global economy is expected to start a process of mending.

Small‑caps tend to perform best and indeed have outperformed large‑caps, when the economic cycle entered a recovery phase. When a positive inflection point in economic growth has been reached, strong returns have historically been generated in small‑caps. Importantly, this trend has often engendered a multiyear cycle. With small‑caps having lagged, and the potential for economies to start to accelerate again, now could be an opportune time to add to small‑cap allocations.

4. Thinking Long Term—Every Giant Started Small

The most successful large‑ and mega‑cap corporations of today started life as small companies. Some started in the founder’s parents’ home—or garage. Some took their first steps as an obscure website, while others were nothing more than a single outfit selling food or manufacturing lamps. Fast‑forward a few decades, and these tiny businesses are now some of the world’s largest international corporations.

Investing in small‑caps today may give investors with a long‑term investment horizon the opportunity to join the journey of some of tomorrow’s most successful businesses at an early stage. While some giants struggle to grow because they are big, small‑caps often have the best to come. Not all small companies will succeed—some will fail, especially during the hardship of an economic recession. However, skill, experience, and diligent research can potentially help to uncover future winners.

5. Size Factor Is Dead, Long Live Liquidity and Alpha Factors

When Eugene Fama and Kenneth French unveiled their three‑factor model in the 1990s, they claimed that small companies should outperform big companies because of a risk premium. A risk premium for the size factor makes sense because, compared with large organizations, smaller companies typically have less diversified businesses with weaker balance sheets. Therefore, they are riskier investments. To compensate investors for this risk, returns must be higher; otherwise, why would any rational investor take excess risk without potential excess return?

Over the years, the size factor has diminished to the point that some academics and practitioners claim that it has all but disappeared. The fading importance of the size factor doesn’t mean small‑caps do not have a role in portfolios. First, because small‑caps are less liquid than large‑caps, they may come with a liquidity factor. Illiquidity is a risk, and a liquidity premium is needed to compensate investors.

Secondly, and more interestingly, the small‑cap universe is vast, offering a breadth of choice and companies that are less well researched and known compared with large ones. This means there are likely hidden gems waiting to be discovered by skilled active managers—the alpha factor. Indeed, some active strategies specializing in smaller companies have outperformed their benchmarks by some way so far in 2020. While not systematic and dependent on talent, the alpha factor in small‑caps is another reason to consider investing in the asset class using actively managed strategies.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

July 2020 / Investment Insights