June 2021 / MARKET OUTLOOK

As the Global Economy Recovers, Japan Stands in the Spotlight

Upbeat outlook as Japanese market is highly geared to global recovery

Key Insights

- The outlook for Japanese equities appears favorable at the current stage of the business cycle.

- The cyclical nature of the Japan equity market means it is highly leveraged to a prospective recovery in global demand.

- Ongoing structural market reform and the acceleration of secular growth trends add to the optimistic outlook for Japan through 2021 and beyond.

While Japanese equities made solid progress during the first half of 2021, the TOPIX gaining 8.52%, year-to date (as of May 28, 2021), performance has ultimately disappointed, with Japan trailing other major equity market returns. This is partly due to Japan’s strong outperformance in 2020, but also reflects idiosyncratic issues, such as the slow roll-out of the coronavirus vaccine and, more recently, the imposition of localized lock downs in certain prefectures, including Tokyo.

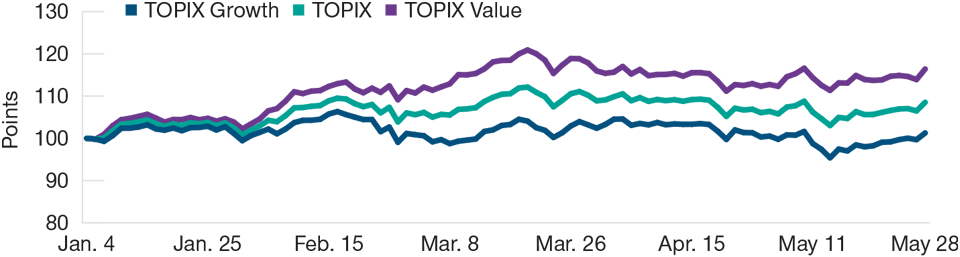

The dominant market theme during the first half of the year has been the ongoing market rotation, out of growth stocks and into value, that began toward the end of 2020. This trend accelerated in earnest from February, with the arrival of the Pfizer coronavirus vaccine. Having been delayed in Japan, the rollout of the vaccination boosted hopes of an economic reopening, encouraging investors to rotate into cyclical value companies at depressed prices.

Meanwhile, expectations that the vast amounts of fiscal and monetary stimulus provided by governments around the world would inevitably prove inflationary also saw investors rush to take profits on growth stocks in favor of value and lower‑quality cyclical stocks.

Early cycle value areas like banking and autos and, most notably, commodity‑related sectors, have significantly outperformed in 2021 (Fig. 1), as investors have poured money into these areas to try to take advantage of depressed stock prices. However, while the market rotation has been severe, we also believe that it is largely played out, as prices have risen to more “normalized” levels.

Market Rotation Has Accelerated in 2021

(Fig. 1) Value stocks have strongly outperformed growth in 2021

Past performance is not a reliable indicator of future performance.

As of May 28, 2021.

Data re-based to 100.

Sources: Refinitiv, © 2021 Refinitiv, all rights reserved, and T. Rowe Price.

We remain positive about a number of secular growth areas that offer potentially open‑ended, long‑term growth opportunities. Many companies in these areas are currently at the lowest valuations seen in years. These are innovative, resilient businesses that have been able to sustain high returns on equity and are well positioned to grow market share over a long‑term horizon. Indeed, the global pandemic has accelerated secular growth trends that were already in place in Japan, such as factory automation, e‑commerce, digitization, e‑health, fintech, and environmental technologies. At the same time, competitive dynamics have also improved—meaning well‑positioned, resilient businesses are likely to emerge even stronger.

Budgetary and Monetary Support Remain Accommodative

In August 2020, Japan’s longest‑serving prime minister, Shinzo Abe, announced his resignation due to declining health. The sudden announcement raised fears that Mr. Abe’s transformational “Abenomics” program of economic and regulatory reform would also come to an end. However, Mr. Abe’s long‑serving Chief Cabinet Secretary and right‑hand man, Yoshihide Suga subsequently won a landslide victory in the ruling Liberal Democratic Party’s leadership election, assuming the prime ministership in the process. This not only provided political continuity and stability in Japan, but also ensured the continuation of the Abenomics structural reform program.

Since taking the helm, Mr Suga has stepped-up government spending and structural reform efforts, and maintained the focus on economic growth as Japan’s number one priority. Mr Suga has also pledged to cut greenhouse gas emissions to net zero by 2050, vowing to transform Japan’s policy on coal-fired power generation and boost innovation in renewable energy. Elsewhere, the Governor of the Bank of Japan, Haruhiko Kuroda, has reiterated the Bank’s commitment to maintaining ultra-easy monetary policy.

Domestically, Japan’s Diet approved a record JPY 106.61 trillion (USD 976 billion) budget for the 2021 fiscal year to help mitigate the fallout from the coronavirus pandemic as well as rising social security and defense costs. The Bank of Japan published a review of its policy tools, signaling that it will keep easing measures in place for a prolonged period, and continue with its “yield curve control” strategy, but with added flexibility.

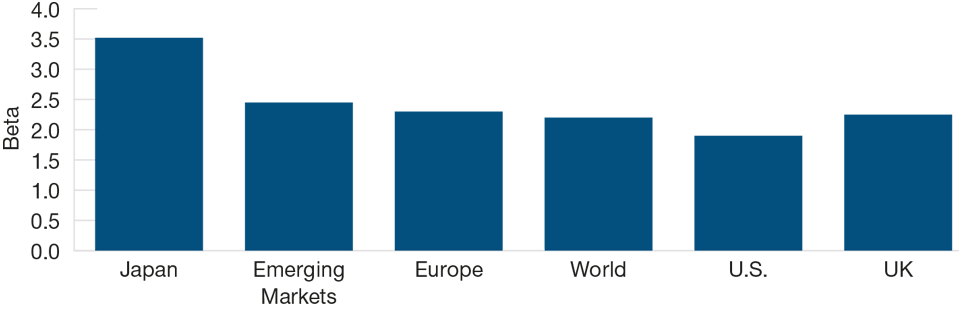

On the economic data front, a better‑than‑anticipated gross domestic product report showed the Japanese economy growing at a 12.7% annualized pace in the fourth quarter of 2020, supported by strong exports (particularly to China), consumption, and capital expenditure. This augurs well for Japan’s cyclical market, with corporate earnings highly levered to the health of the global economy and export demand (Fig 2).

Japanese Corporate Earnings Are Highly Levered to a Prospective Global Recovery

(Fig. 2) Beta of regional corporate earnings per share to global industrial

production

As of March 31, 2021. Subject to change.

Source: Nomura.

Key Factors to Watch in H2 2021—Vaccines, Lockdowns, and the Olympics

Despite its densely populated cities and an aging population, Japan has managed to broadly contain the spread of the coronavirus and keep the mortality rate relatively low. That said, Japan has recently seen an acceleration in the numbers of coronavirus infections, with a state of emergency having to be declared in certain districts. While this is a worrying setback, it is worth noting that the current situation is less restrictive than lockdowns in Europe and the U.S., or even Japan’s own spring 2020 lockdown. Currently, just four prefectures (of 42) are facing curbs and curfews in the evening. Japan has dealt effectively with previous waves of the coronavirus much better than most of the world, but it would do well to arrest this latest outbreak ahead of the Tokyo Olympics, which the government and authorities are keen to proceed with. Given the success with which Japan has dealt with previous waves of the pandemic, and the fact that the vaccination program is accelerating rapidly, we expect the current flare‑up to be dealt with effectively.

Moving Forward

The path to economic recovery is beset with uncertainty, depending on progress of the vaccine rollout, the potential for “new waves,” and the effectiveness of the public health responses to these outbreaks, both domestically and worldwide.

That said, we believe the anticipated global economic recovery will continue to build and broaden through 2021 and beyond and that we will slowly return to some semblance of “normalization.” Given Japan is one of the most cyclical and open markets—highly levered to the health of the global economy—we believe it will be a major beneficiary of the prospective global recovery. Certainly, the rapid economic recovery evident in China, Japan’s major trading partner, represents a significant tailwind.

As we enter the next stage of the equity cycle, amid a broadening domestic and global economic recovery, we continue to believe that Japan is a compelling active management case, particularly as the market is under‑owned, continues to undergo governance reform and improvement, and displays positive change dynamics.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

June 2021 / INVESTMENT INSIGHTS