INVESTMENT INSIGHTS

What Jitters Over Trade Indicate About Markets

August 2019

Key insights

- The recent spike in volatility amid rising concerns over U.S.‑China trade relations indicated that the medium‑term fate of markets will be heavily influenced by how the dispute is resolved.

- A deterioration in relations between the two countries is likely to lead to further bouts of volatility—and possibly a more serious downturn.

- “Timing” the market in this environment will be very difficult. Selectivity is more likely to deliver durable returns during difficult periods.

The recent bout of market agitation over fears of an escalating trade war provided a stark reminder of just how influential US‑China relations are on the global economy. While support remains in place from continued positive corporate earnings growth and accommodative central banks, any worsening of the trade dispute could bring further bouts of turbulence, possibly leading to a more sustained correction. Attempting to time the markets in this environment will be very risky, meaning that investors will likely need to be highly selective if they are to successfully navigate the difficult period ahead.

...twists and turns in this saga, including the imposition of new tariffs and a possible currency war, have the potential to disrupt markets with an immediate and direct impact.

U.S.‑China Trade Tensions Blow Up Again

What a difference a few days can make. For much of the first half of this year, investors seemed assured that slowing global growth would be mitigated by accommodative monetary policies from the U.S., Europe, and emerging markets. While trade tensions ebbed and flowed, the markets chose to believe that common sense would prevail and that a “muddle through” scenario would play out. Rising asset prices reflected this view.

That all changed at the beginning of August when U.S. President Donald Trump announced new tariffs and China swiftly responded by allowing the renminbi to depreciate, prompting accusations of currency manipulation from the U.S. The sudden deterioration in relations between the two countries caused markets to sell off dramatically before stabilizing partially after Beijing stepped in to steady the currency. Any complacency over the U.S.‑China trade dispute was wiped out in a matter of days.

Subsequent twists and turns in this saga, including the imposition of new tariffs and a possible currency war, have the potential to disrupt markets with an immediate and direct impact. “Given the pace at which things change in trade negotiations, it is likely markets will continue to react to headlines and tweets for a while,” says Andrew McCormick, head of Fixed Income. “We are no longer pricing in a rosy scenario.”

...selectivity is key to tuning out short‑term noise...

The depth and complexity of the U.S.‑China trade dispute means that it is very difficult to predict how negotiations will progress from here. “There have always been two issues,” says Fixed Income Sovereign Analyst Chris Kushlis. “First, the narrow trade issue, and second, the longer‑term, geo‑strategic rivalry—and it has been very hard to keep those on separate tracks. For a while, it seemed as if it might be possible to craft a narrow trade deal with limited substance, but even that now seems unlikely.”

What President Trump does from here will likely depend on what he believes will best enable him to get reelected as president next year, Kushlis believes. “What serves President Trump better: striking a trade deal or positioning himself as a ‘trade warrior’ and hoping that Fed interest rate cuts bail him out?” he says. “The Chinese are likely to dig in—they will not want to reward any pressure tactics from Trump. Overall, this is not good for anybody. There are no winners—just relative losers.”

Lack of Consensus on Strength of Global Economy

The potential impact of a worsening U.S.‑China trade dispute on markets depends largely on the underlying strength of the global economy. Here, views differ, reflecting the strength of T. Rowe Price’s diversity of thought among its investment professionals.

Head of Global Multi‑Asset Sebastien Page acknowledges that there are concerns that the current extended cycle is fragile, but he says he does not believe the conditions are in place for a severe downturn. “We recognize the fragility of an aging cycle,” he says, “but we don’t see major speculative imbalances that could trigger a crisis.”

Charles Shriver, co‑head of the T. Rowe Price Asset Allocation Committee, agrees. He argues that while continued volatility can be expected, conditions remain supportive. “The monetary policy environment is supportive, with the recent Fed rate cut and the likelihood of further action to offset weak growth, trade uncertainty, and tighter financial conditions,” Shriver says.

Other portfolio managers, particularly those in fixed income, are more cautious. Quentin Fitzsimmons, senior portfolio manager in the Fixed Income Division, believes that a breakdown in talks could push a fragile global economy over the edge. “I believe that the current situation has the ingredients of a full‑blown international crisis,” he says. “There is a confluence of factors—U.S. politics, Chinese politics, the global economic cycle, the rise of populism, and the impact of technological change on key industries. All of these have been around for a while, but they seem to be coming to a head at the same time.”

“I see parallels with 2007, just before the global financial crisis struck.”

Maintaining a Long‑Term Strategic Approach

When uncertainty is elevated, timing the markets—always a risky endeavor—becomes virtually impossible. At T. Rowe Price, we believe that selectivity is key to tuning out short‑term noise in favor of durable, consistent returns. Our portfolio managers average 22 years in the industry and 17 years with T. Rowe Price, so they’ve weathered all kinds of markets. We’ve learned that volatile periods are often the time to buy good businesses at attractive valuations.

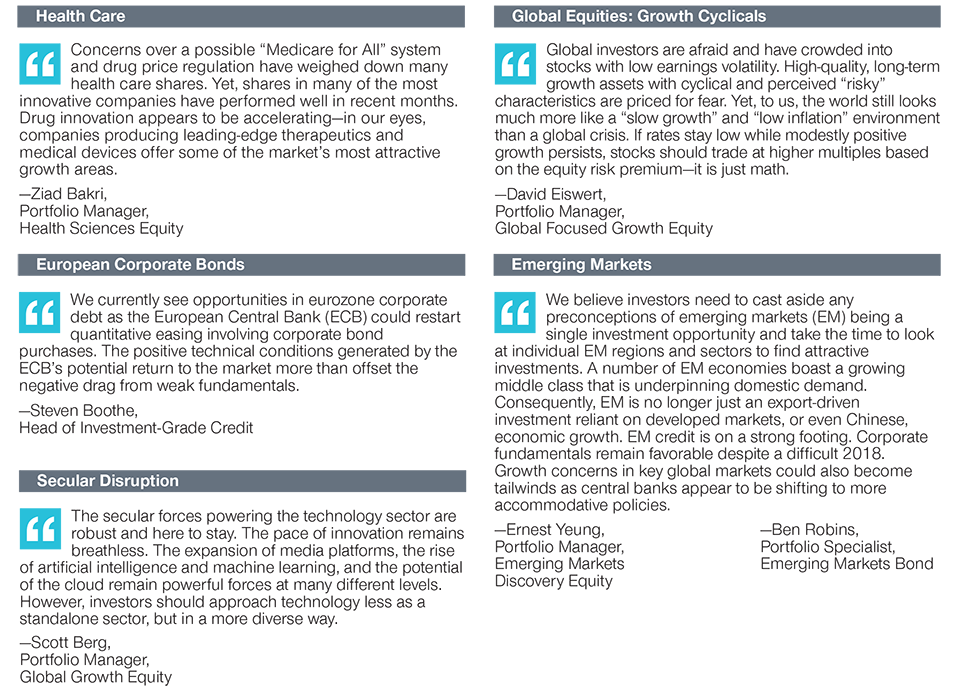

Against that backdrop, here are some notable trends we’re observing:

What we’re watching next

The unpredictable nature of the U.S.-China trade dispute means that it is difficult to predict when the next developments will occur, but we will be monitoring this situation very closely for the foreseeable future. U.S. President Donald Trump’s next move should tell us something about his long-term objective: Will he tone down the rhetoric and focus on trying to strike a deal with the Chinese (in which case, the economic cycle may be extended further)? Or will he dial up the pressure in a bid to position himself as defender of the U.S. economy ahead of next year’s presidential election (in which case, brace yourself for further volatility)?

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

201908‑921569