June 2021 / MARKET OUTLOOK

Positioning for a New Economic Landscape

Recovery is on track, but inflation pressures create risks

Key Insights

- Global growth accelerated in early 2021, led by China and the U.S. The economic recovery from the pandemic appears set to broaden in the second half.

- Despite strong growth, earnings expectations could be difficult to meet. But there may be potential for earnings outperformance in some non‑U.S. markets.

- Strong institutional demand for U.S. Treasuries is holding yields down. Fixed income investors may want to consider credit sectors for opportunities.

- China’s tighter corporate governance standards, better capital allocation, and technical innovation are expanding the opportunity set for investors.

The strengthening economic recovery from the coronavirus pandemic appears poised to broaden across regions and countries in the second half of 2021, bolstered by vaccine progress, continued fiscal and monetary stimulus, and pent‑up consumer demand.

But this new economic landscape poses a number of critical questions for investors. A key one is whether growth will be strong enough to meet optimistic earnings expectations without fueling sustained inflationary pressures—the kind that could force the U.S. Federal Reserve and other central banks to speed up a turn toward tighter monetary policy.

“To make the case that broad equity valuations are attractive, you have to rely on an argument that there’s no practical alternative,” says Robert Sharps, president, head of Investments, and group chief investment officer (CIO). “That would rest on a continuation of low interest rates and low inflation.”

Justin Thomson, head of International Equity and CIO Equity, suggests that equities can do well with a modest uptick in inflation but not a significant acceleration. “Historically, periods of rising inflation have been relatively good for equities in aggregate—but only up to a point. Once inflation gets beyond 3% or 4%, it has tended to choke off returns.”

For bond investors, rising yields pose obvious risks but could create potential opportunities, notes Mark Vaselkiv, CIO Fixed Income. Higher yields could make some credit sectors potentially attractive relative to equities, he says, prompting an asset allocation shift.

“I think at some point many equity investors will want to try to lock in the gains they’ve enjoyed from the bull market,” Vaselkiv suggests. “If so, there could be a rotation back to fixed income.”

Building a Sustainable Recovery

Accelerated vaccine campaigns in the developed countries, additional stimulus, and a surge in business activity as industries reopen all appear to have set the stage for robust global economic growth in the second half of 2021 (Figure 1).

Pent‑up demand and fiscal and monetary stimulus should help sustain above‑average growth well into 2022, Sharps says. Recent forecasts from the Organisation for Economic Cooperation and Development (OECD), he notes, suggest that global gross domestic product (GDP) could grow almost 6% in 2021, and 4%–5% in 2022.1

If consumer demand continues to accelerate in the second half of 2021, Sharps adds, “we could experience an economic boom unlike anything we’ve seen in some time.”

Although China and the U.S. have led the recovery so far, Sharps predicts that faster growth will extend to other economies as 2021 progresses. “This might be better characterized as a sequenced global recovery, rather than a synchronized global recovery,” he says. However, the timing of that sequence is likely to remain uneven, as some countries and regions, including India and Latin America, continue to struggle with the pandemic.

A quickening recovery is reshaping the demand in ways that could create both short‑term and long‑term potential opportunities for investors, Sharps says. Areas that could potentially benefit include the travel and hospitality industries, airlines, restaurants, and medical services.

By speeding up the adoption of more efficient technologies and business models, the pandemic also could set the stage for future productivity gains, Sharps argues. That could raise the long‑term global potential for economic and earnings growth.

The Inflation Debate

Although signs of inflationary pressures—such as surging commodity prices and a global semiconductor shortage—periodically rattled markets in the first half, central bankers and other financial officials have taken a relatively dovish view, Thomson notes. “The received wisdom is that the monetary authorities understand inflation and have the tools to deal with it,” he adds.

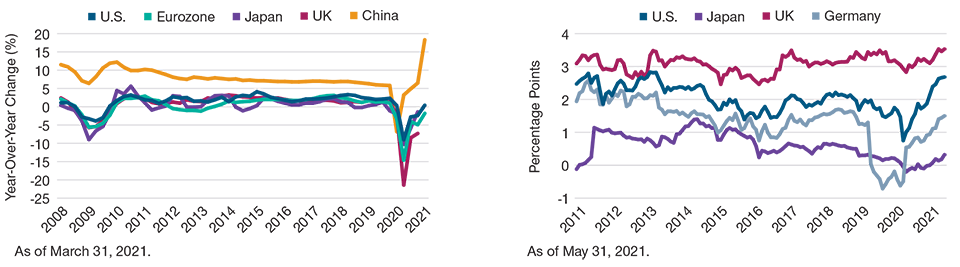

Growth Surge Brings Rising Inflation Expectations

(Fig. 1) Real GDP year‑over‑year growth rates and 10‑year yields minus inflation‑linked 7- to 10-year yields*

Past performance is not a reliable indicator of future performance.

*Break‑even calculation uses the 10‑year benchmark government yield minus the Bloomberg Barclays Government Inflation‑Linked (7–10 Year) Index yield for each country.

Sources: Bloomberg Finance L.P., data analysis by T. Rowe Price, and Haver Analytics (see Additional Disclosures). T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.

The optimistic case, Thomson says, is that the acceleration is a transitory effect that will fade as supply bottlenecks are overcome and the surge in post‑pandemic demand runs its course. But Thomson cites several longer‑term trends that he thinks could produce a structural shift to higher inflation rates:

- Large U.S. fiscal deficits, which have been dramatically enlarged by pandemic stimulus efforts.

- Demographics, as retired baby boomers spend their savings and labor shortages push wages up.

- “Deglobalization”—a turn toward higher tariffs, immigration barriers, and supply onshoring.

Vaselkiv says wage hikes by leading U.S. companies also suggest that the balance of economic power has tilted toward workers in ways that won’t be reversed quickly. This is not entirely bad news, since rising consumer income could help sustain the recovery as fiscal and monetary stimulus efforts wind down.

But Sharps cites another potential inflation threat that decidedly lacks any upside: cyberterrorism. Recent extortionary attacks on a primary U.S. pipeline and a major meat supplier show how fragile global supply chains could be in a wired age. “You could argue that these were one‑off events,” he says, “but at this point they seem to be turning into serial one‑offs.”

Read the full 2021 Midyear Market Outlook: Positioning for a New Economic Landscape (PDF).

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

June 2021 / INVESTMENT INSIGHTS