Choose your location

Denmark

English

Belgium

Denmark

Estonia

Finland

France

Iceland

Ireland

Latvia

Lithuania

Luxembourg

Netherlands

Norway

Portugal

Sweden

United Kingdom

From complexity to clarity

The outlook for emerging markets (EM) continues to divide investor opinion. Over the past decade, several headwinds have posed significant challenges to the EM investment case and, more recently, China’s slowdown has further dampened sentiment. In the short-term, volatility is likely to persist. On the other hand, EMs continue to offer an attractive growth premium versus their developed counterparts, and with many EM central banks appearing positioned to begin a rate-cutting cycle, the early stages of recovery may be forming.

Against this backdrop, there underlies a rich tapestry of opportunities for the informed investor in emerging markets across a diverse group of countries, industries and individual securities.

Whatever the future holds, we're here to help bring you clarity in emerging markets.

Our Latest Insights on Emerging Markets

Our Investment Capabilities

Our emerging market equity strategies

Our emerging market debt strategies

Our unique approach to investing in China

With over 6,500 investable companies, China has become the second largest stock market globally, and arguably the most dynamic equity market in the world. The vast majority of this universe remains highly inefficient and overlooked. While the news flow can be overwhelming at times, we remain constructive on both the cyclical and structural theses for China and that short-term bouts of adversity can bring with them exciting new opportunities.

Our Emerging Markets Story

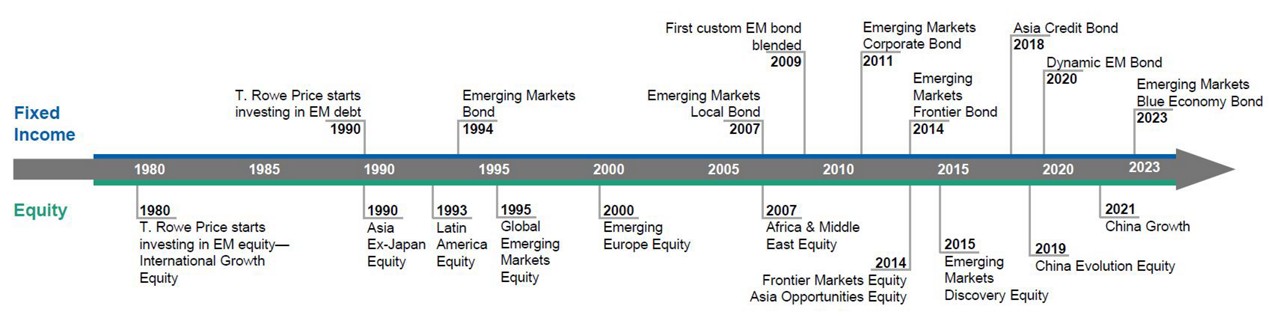

At T. Rowe Price, we’ve seen an extraordinary amount of change since we started investing in EM more than 40 years ago. That experience is invaluable as our teams work across the region fostering long-term partnerships with companies and governments, to find the most compelling and durable investments for our clients’ portfolios across the capital structure. And when combined with our size and scale in EM, it gives us a much deeper and clearer understanding of the opportunities to grasp and the risks to assess.

Our capabilities have expanded over time

Want to know more? Get in touch.

If you have questions or would like more information about T. Rowe Price please contact us.

1Firmwide Emerging Markets Equity and Fixed Income AUM include assets managed by T. Rowe Price Associates, Inc. and its investment advisory affiliates as of 30 June 2023.

2As of 30 September 2023. Figures include the EM Equity and EM Debt Team

202401-3096632