June 2022 / MARKET OUTLOOK

Navigating Challenging Currents

How can investors respond to the risks of recession in Europe and the US and a further growth slowdown in China?

Inflation expectations are likely to dominate financial market performance in the second half of the year, just as they did in the first, the T. Rowe Price CIOs predict.

Although investors must contend with other economic headwinds—the war in Ukraine, COVID‑19 lockdowns in China, and central bank tightening—inflation is the risk that channels those pressures into financial asset prices, Page argues.

- Higher energy and food prices in effect are a tax on the consumer, the main engine of global economic growth.

- With interest rates rising, continued earnings gains will be needed to support positive equity returns. But higher wage and input costs could cut into profit margins.

- Inflation raises the risk that the Fed will hike rates too aggressively, increasing the cost of capital and causing a recession.

“Those are three ways in which inflation can trigger a growth shock,” Page says. The key questions investors face now are whether inflation has already peaked, and, if so, whether it will decelerate quickly enough to limit the need for a prolonged monetary tightening campaign by the Fed.

While there have been some anecdotal signs in some markets that price pressures are easing—such as a slowdown in home price appreciation and cooling demand for labor—clearer evidence is needed, Husain argues. “Until we see a meaningful decline in inflation toward the targets that central banks have set, the burden of proof hasn’t been met,” he says.

How Will Central Banks Respond?

Even if inflation has peaked, fixed income investors appear unconvinced it will quickly return to the Fed’s long‑run target.

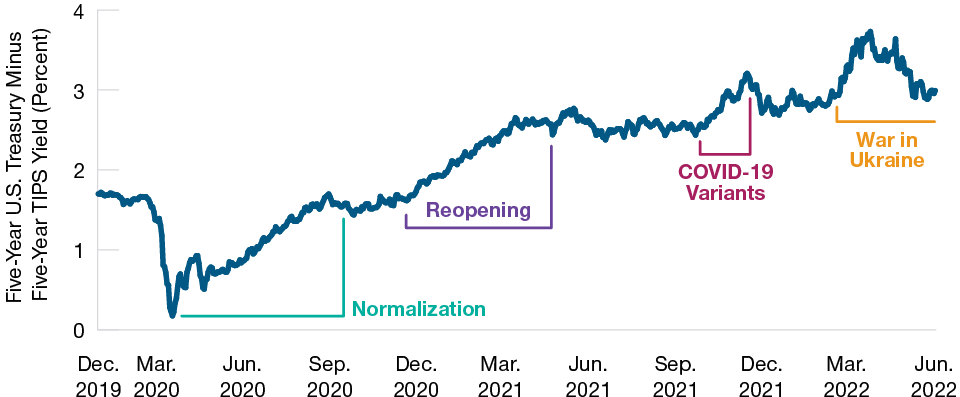

Figure 2 shows the spread, or breakeven, between yields on the nominal five‑year U.S. Treasury note and on the five‑year Treasury inflation protected security (TIPS). The breakeven is widely viewed as an estimate of investors’ inflation expectations.

Inflation Is Still the Key Issue for Global Investors

(Fig. 2) Five‑year U.S. inflation expectations based on TIPS breakeven yields

December 31, 2019, through June 1, 2022.

Source: Bloomberg Finance L.P. Data analysis by T. Rowe Price.

Although inflation expectations eased somewhat after surging in the wake of Russia’s invasion of Ukraine, the breakeven remained close to 3% as of the end of May—almost a percentage point higher than the Fed’s long‑term target for the U.S. consumer price index (CPI).

“The market has already priced in a number of future Fed rate hikes, yet it still expects inflation to overshoot the Fed’s target by a full percentage point per year over the next five years,” Page comments.

With the CPI up more than 8.5% year over year through May, the market consensus also could prove too optimistic, Page says. “What if the CPI gets stuck on the way down at 4% or 5%?” he asks. “How committed is the Fed to its 2% target?”

The answers could be critical, and not just for the bond markets, Thomson says. “For global equity markets, the inflation outcome is absolutely key.”

“If inflation settles around 3%, that could be a reasonable backdrop for equities,” Thomson argues. “If it’s between 3% and 4%, things could get a bit more difficult. But, if it’s over 4% it could be [Paul] Volcker time”—a reference to the Fed chairman of the early 1980s who hiked rates to double‑digit levels to break an inflationary spiral, pushing U.S. equities into a deep bear market.

The Supply Chain Factor

Inflation pressures are coming from both supply and demand and are being driven by both cyclical and structural factors, which makes the forecast exceptionally cloudy, Husain notes.

“I think what that means is that the Fed is going to keep raising rates,” Husain says. “There will come a point where they’ll want to pause and see what effect they are having. But my view is that we should be prepared for much higher rates going forward over the next few months.” Page suggests a possible silver lining to those clouds. There is plenty of potential “pent up” supply in the global economy, he argues, which could help bring inflation down if supply chain bottlenecks can be unclogged.

“The question is whether fixing supply chains could do part of the Fed’s job for it,” Page says. “If it happens soon enough, maybe they won’t have to push demand off the cliff.”

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Download the full 2022 Midyear Market Outlook insights

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.