May 2021 / BLOG

Navigating a Landscape of Interlinked Crises

Opportunities presented by public policy in the Biden era

Key Insights

- Investors remain concerned about the U.S. legislative and regulatory landscape, given the backdrop of interlinked crises inherited by the Biden administration.

- The coronavirus has brought a new level of uncertainty to markets, raising questions about what tools governments will use to get to a postcrisis environment.

- U.S. President Joe Biden has already adapted his policy rhetoric from “transformation” to “crisis management,” informing his legislative/regulatory agenda for the next four years.

Within T. Rowe Price, our Public Policy Research team supports our analysts and portfolio managers through all stages of the investment process. We work closely with our environmental, social, and governance (ESG) team to integrate policy catalysts and risk factors into the Responsible Investing Indicator Model (RIIM), while helping our investors assess the likely outcomes and implications of legislative, regulatory, and legal decisions for their company holdings and sectors.

Concerns Around U.S. Policy Remain, but of a Different Nature

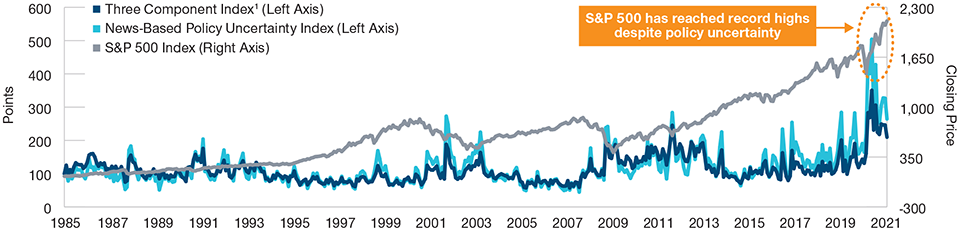

Between 2016 and 2020, we experienced a marked increase in concern from investors regarding the political volatility driving the legislative and regulatory environment. Despite this spike in economic policy uncertainty, the U.S. equity market still marched higher—with the S&P 500 Index gaining more than 1,000 points (Fig. 1).

As 2021 has progressed, investors have expressed concern regarding the legislative and regulatory backdrop, but for an entirely different reason: crisis management. With the coronavirus pandemic came a level of market and economic uncertainty that continues to transform investors’ expectations about the future—what a “new normal” might look like for the global economy and what tools different governments will use to get to a postcrisis environment.

Economic Policy Uncertainty Index Versus the S&P 500 Index

(Fig. 1) Amid a backdrop of interlinked crises, policy uncertainty has spiked

As of January 31, 2021.

Past performance is not a reliable indicator of future performance.

1 The Three Component Index is constructed from three underlying datasets. One component quantifies newspaper coverage of policy-related economic uncertainty. A second component reflects the number of federal tax code provisions set to expire in future years. The third component uses disagreement among economic forecasters as a proxy for uncertainty.

Source: “Measuring Economic Policy Uncertainty,” by Scott Baker, Nicholas Bloom, and Steven J. Davis at http://www.PolicyUncertainty.com. S&P indices (see Additional Disclosure). Data rebased to 100.

To this end, we have seen recently elected U.S. President Joe Biden adapt his policy rhetoric from “transformation” to “crisis management,” framing the federal government as a source of stability for American families and businesses—not only for the dual public health and economic crises, but also for the risks posed by climate change and racial inequality.

The Challenge of Triaging Interwoven Crises

Coronavirus: Public Health and Economic Crises

The Biden administration’s foremost priority is helping the nation heal from the public health and economic fallout caused by the coronavirus pandemic. As such, we expect landmark stimulus proposals to dominate the Biden administration’s capacity in the coming year: the American Rescue Plan Act, comprising around USD 1.9 trillion in relief spending, and signed into law on March 11, 2021; and Biden’s “Build Back Better Plan,” which has been proposed in two phases: the American Jobs Plan, containing clean energy and infrastructure investment; and the American Families Plan, containing “human infrastructure” investments in health care, childcare, and the broader social safety net. Estimates for those proposals combined range between USD 2 trillion and USD 4 trillion in new spending and USD 1 trillion to USD 2 trillion in revenue raisers.

Combined, these plans inject an unprecedented level of federal stimulus into the U.S. economy—providing a striking amount of direct transfer payments to consumers and incentives for renewable and green technologies. The Build Back Better platform also invests in legacy infrastructure, creating opportunities in utilities and sectors related to grid modernization, broadband internet, transportation, and water systems. The Biden administration may also attempt to incorporate significant labor reforms to expand the workforce and increase the minimum wage—though they would likely not pass under the reconciliation process in Congress. These changes would have dramatic implications for different sectors’ recoveries during and after the pandemic and will shift investors’ overall expectations regarding tax policy, gross domestic product growth, and inflation.

Climate Change: Legislative Incentives and Regulatory Deterrents

Though a comprehensive, progressive environmental reform package like the Green New Deal is unlikely in this presidential term, we should expect a significant reversal from the regulatory status quo as President Biden builds one of the most progressive environmental policy portfolios in U.S. history. Specifically, the Biden administration seeks to heavily incentivize consumer and industrial adoption of green technologies—like electric vehicles and renewable power—through legislation; while disincentivizing the continued use and expansion of fossil fuels through regulation, which can be executed on a unilateral basis through federal agencies. The U.S. has also rejoined the Paris Climate Accord and the president will look to establish cross‑departmental research initiatives to expand policy recommendations for climate innovations like decarbonization. We also anticipate that the Biden administration will pursue stronger disclosure requirements and assessment of climate risk from firms, affecting our analysis of these firms’ environmental risk. These changes present an opportunity to actively engage with the companies we are invested in, share our experience and expertise; and advise on disclosure best practices, where required.

Societal Division: Civil Rights, Wealth Inequality, and Populism

President Biden has explicitly identified racial injustice as a pivotal crisis facing the United States—intersecting with underlying issues like wealth inequality. We should expect the administration to pursue regulations and policy developments that improve racial equity while addressing workers’ rights. This includes mandated improvement of worker protections, rhetorical support for unionization efforts, and advocacy for a higher federal minimum wage, as well as instigating federal investigations to identify and penalize discriminatory practices. It also includes implementing more progressive corporate and personal tax proposals to address the inequitable distribution of wealth in the United States. Though gridlock may prevent the Democratic majority from achieving several of these goals, we should expect the Biden administration to pursue these goals through all executive and regulatory tools available.

After the January 6 attack on the U.S. Capitol, concerns over falsified and propaganda‑driven information—amplified by algorithms perpetuating the isolation of specific demographic and geographic groups in the U.S.—prompted a renewed push for tech regulation. We will be monitoring how platform companies respond to data privacy, content liability, and market concentration concerns as Congress, the Department of Justice, the Federal Trade Commission, and the Federal Communications Commission begin to propose tools to regulate company behavior. From an investment perspective, the ramifications of such regulatory actions on the operations, and the bottom lines, of those companies most impacted could ultimately prove substantial.

Public Policy in Our Investment Analysis

As the U.S. federal government continues to respond to the changes caused by the coronavirus—and begins to address the crises posed by climate change and societal division—we should expect further policy changes with significant implications for financial markets. We will continue to monitor government action and incorporate it into our fundamental analysis as we pursue the highest‑quality investment performance for our clients.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.